Conditioning on a Volatility Proxy Compresses the Apparent Timescale of Collective Market Correlation

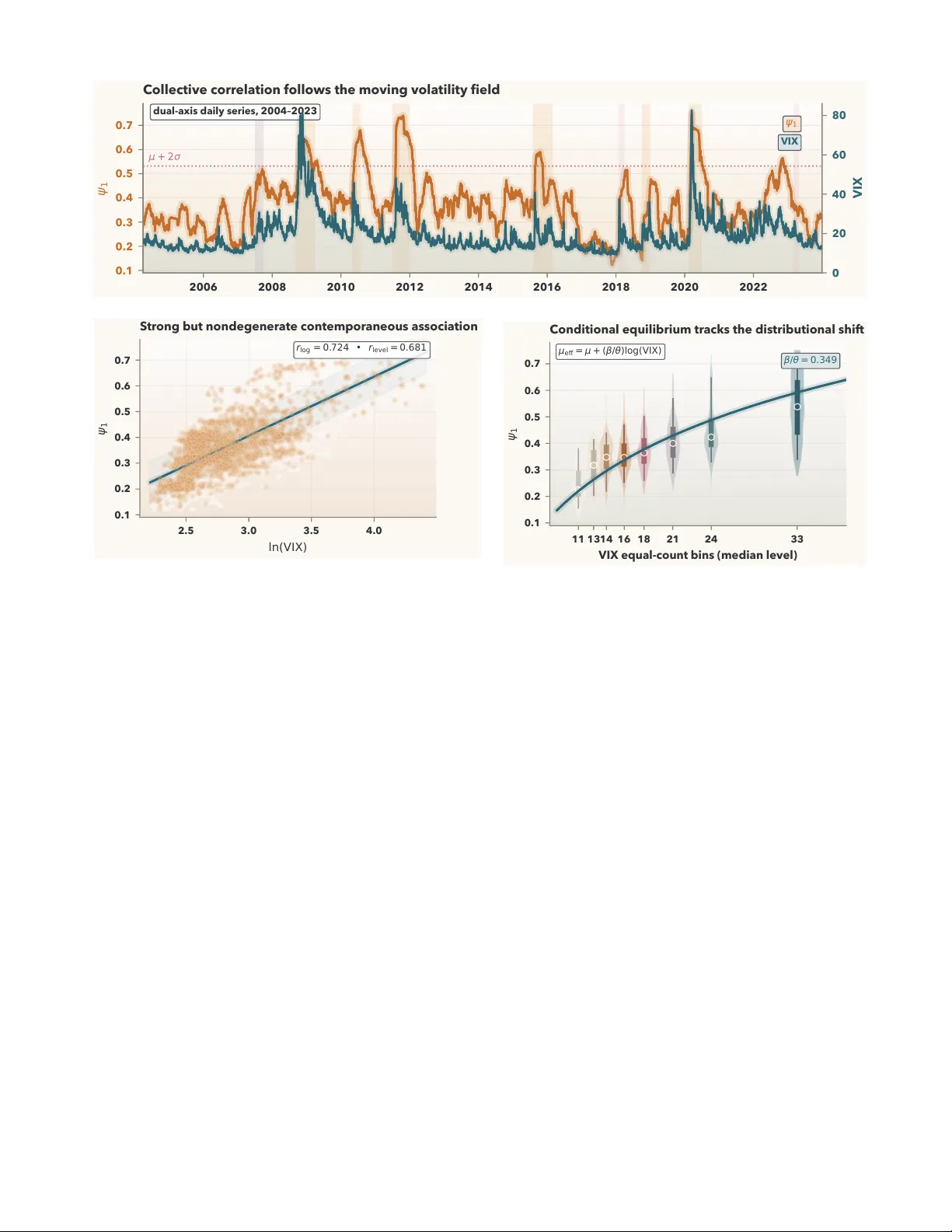

We address the attribution problem for apparent slow collective dynamics: is the observed persistence intrinsic, or inherited from a persistent driver? For the leading eigenvalue fraction $ψ_1=λ_{\max}/N$ of S\&P 500 60-day rolling correlation matric…

Authors: Yuda Bi, Vince D Calhoun