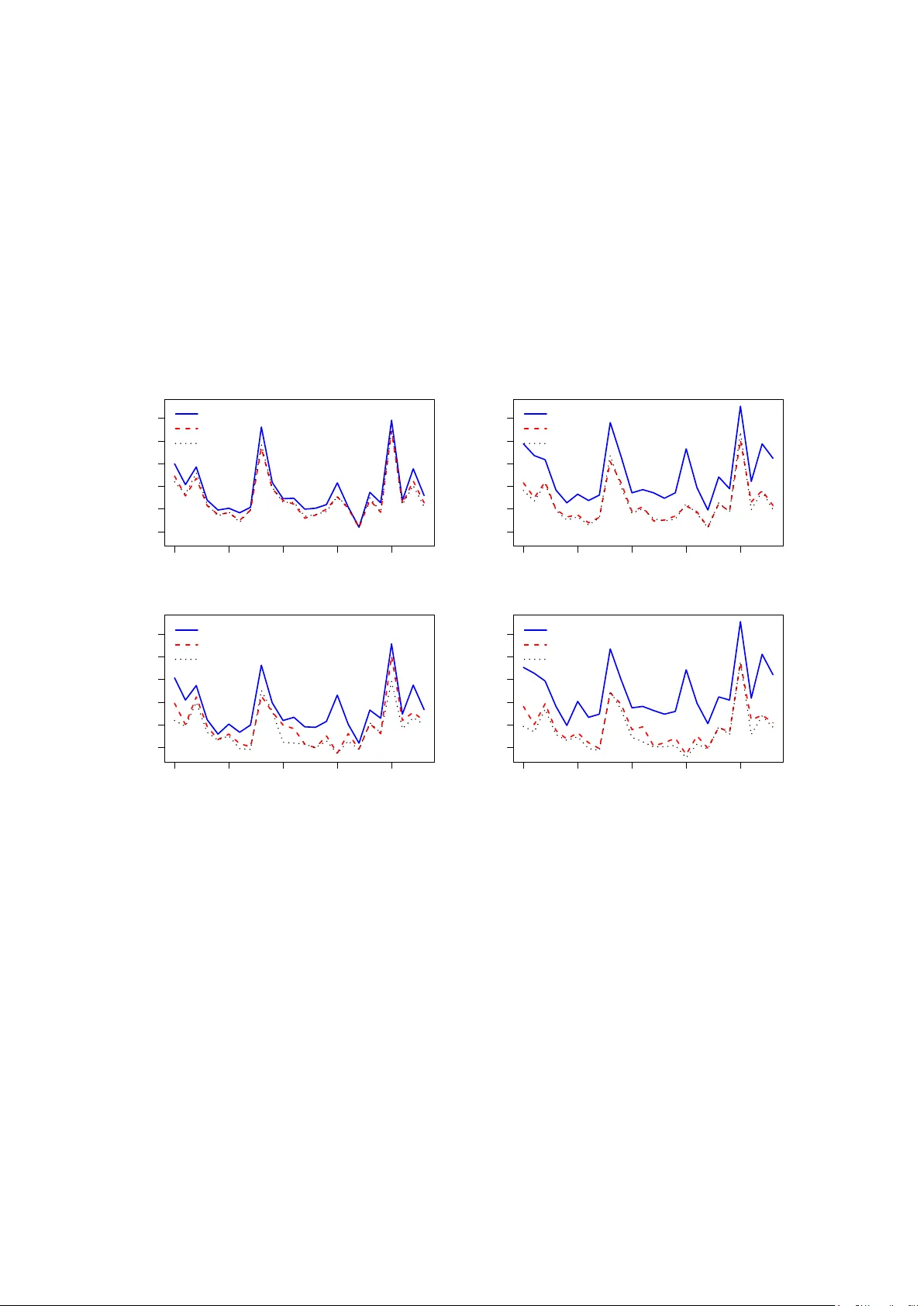

Zero Variance Portfolio

When the number of assets is larger than the sample size, the minimum variance portfolio interpolates the training data, delivering pathological zero in-sample variance. We show that if the weights of the zero variance portfolio are learned by a nove…

Authors: Jinyuan Chang, Yi Ding, Zhentao Shi