Categorisation of Spreadsheet Use within Organisations, Incorporating Risk: A Progress Report

There has been a significant amount of research into spreadsheets over the last two decades. Errors in spreadsheets are well documented. Once used mainly for simple functions such as logging, tracking and totalling information, spreadsheets with enha…

Authors: Mukul Madahar, Pat Cleary, David Ball

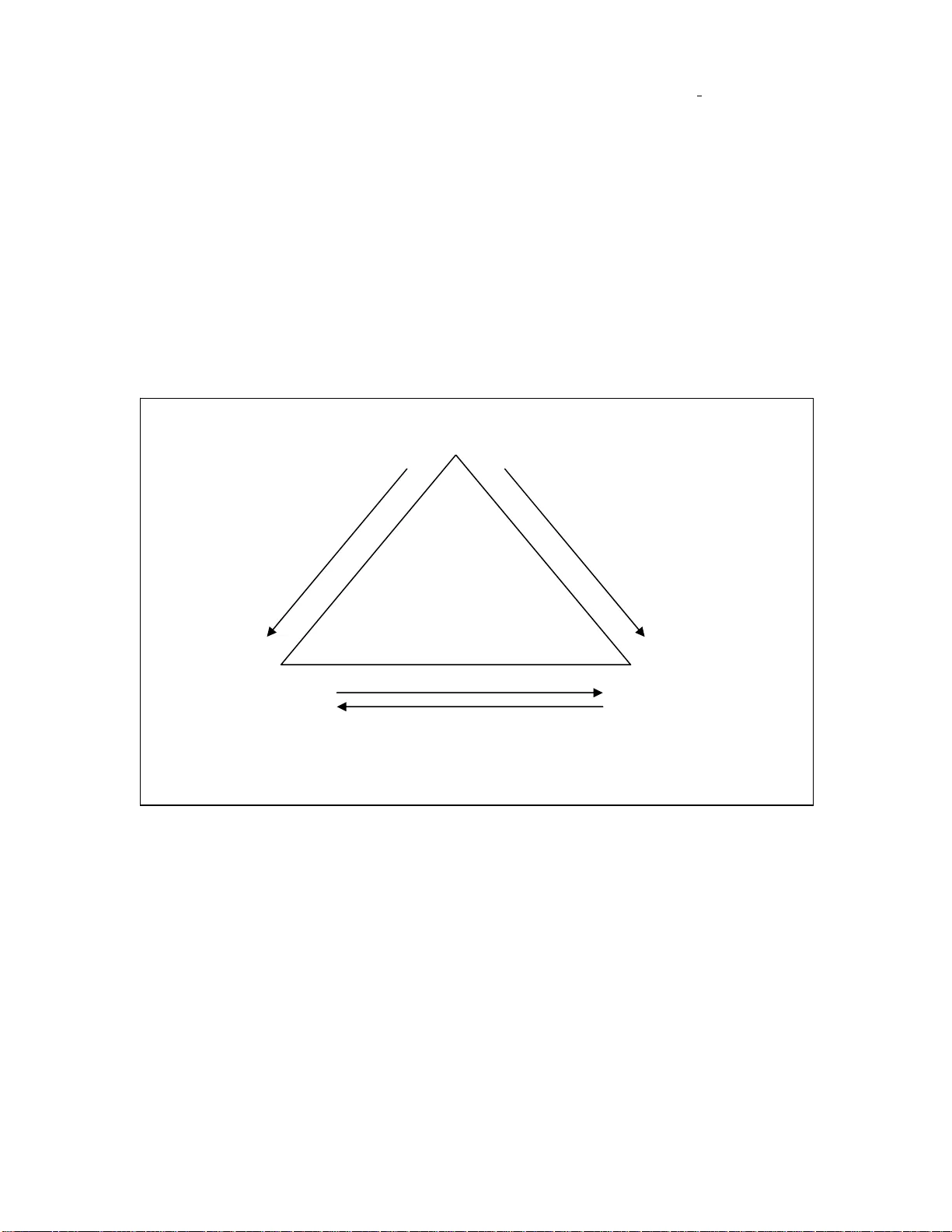

Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 37 Categorisation of Spreadsheet Use within Organisations, Incorporating Risk: A Progress Report Mukul Madahar, Pat Cleary, David Ball Cardiff School of Management University of Wales Institute Cardiff Colchester Avenue Cardiff, CF23 9XR mmadahar@uwic.ac.uk , pmcleary@uwic.ac.uk , dball@uwic.ac.uk ABSTRACT: There has been a significant amount of research into spreadsheets over the last two decades. Errors in spreadsheets are well documented. On ce used mainly for simple functions such as logging, tracking and totalling inform ation, spreadsheets with enhanced formulas are being used for complex calculative models. There are many software packages and tools which assist in detecting errors within spreadsheets. There has been very little evidence of investigation into the spreadsheet risks associated with th e main stream operations within an organisation. This study is a part of the investigation into the means of mitigating risks associated with spreadsheet use within organisations. In this paper the author s present and analyse three proposed models for categorisation of spreadsheet use and the level of risks involved. The models are analysed in the light of current knowledge and the gene ral risks associated with organisations. 1. INTRODUCTION: Many organisations rely on spreadsheets as a key tool in their financial reporting and operational processes (Price Waterhouse Coopers (PWC), 2004) . Spreadsheets are becoming a significant part of the organisational decision-making fra mework and there is ample evidence that spreadsheets are erroneous. Panko and Nicholas (2005) highlighted the main studies undertaken to analyse the extent of spreadsheet error, wh ich included studies by Hicks (1995), Coopers and Lybrand (1997), KPMG (1998), Butler (2000), and o t hers. There are many software packages and tools such as SpACE, ComplyXL, ClusterSeven and Actuate which tend to assist in locating and rectifying errors within complex spreadsheet mode ls. Majority of the investigations concerning spreadsheet problems have been from a technical perspective. This paper is a part of the investigation within University of Wales Ins titute Cardiff (UWIC) that is examining the spreadsheet risks from a management/organisationa l point of view rather than from a technical stance. The purpose is to relate the risks associated with spreadsh eet use to organisational risk management. The aim is to develop a framework for categorising spreadsheet use, incorporating risk as one of the criteria. Once this framework is developed, it could prove very valuable for managing risks associated w ith spreadsheet use. Many researchers have categorised errors in spreadsheets (PWC, 2004; Panko, 1996; Galletta, 1993; Rajalingham, Chadwick and Knight, 20 00; Rajalingham, 2005). PWC (2004) categori sed spreadsheets by use and complexity. This research attempts to incor porate the risk factor into the categorisation of use of spreadsheets. The paper proposes a nu mber of models of categorisation which are based on a pilot study conducted w ithin the accommodation office of the Facilities Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 38 Department at UWIC. Subsequently a comparativ e analysis of the various models proposed is presented. This paper is organised into three further sections. Section 2 sets out the context of the pil ot study. Section 3 highlights the three m odels th at were proposed as a result of the pilot study. Section 4 then presents a comparison of the m ode ls proposed. Then finally the conclusions are presented. 2. THE STUDY: 2.1 Organisation: For conducting the pilot study the Accommodati on Office, was selected within the Facilities Department of UWIC. The Office is responsib le for arranging accommodation for students and therefore includes all the halls of residence as well as assisting in finding private accommodation. During the summer, the same department works with the Conference Service s Department to organise accommodation for conferences. The spreadsh eet use within the department is diverse ranging from basic record keeping (trivial) to complex budgeting and forecasting (strategic). 2.2 Methodology: The research methodology behind the pilot study reflects an interpretive approach due to the nature of this investigation. As Saunders et al. (2006) highlights, business situations are complex and unique. This study was conducted in orde r to u nderstand how this department use spreadsheets and perception of their im portance and the associated risks. As this study was a pilot, it was decided that Un-s tructured interviews were appropriate, in or der to extract maximum information without any bias or influence on the interviewee. As highlighted by Bell (1993), ‘unstructured interviews centred round the topic area may produce a wealth of valuable data.’ The rationale behind the pilot investigation was to identify and analyse which aspects to explore further and areas that need to be discarded. The data gathered was analysed to identify the spectrum of use of spreadsheets within the department. The models proposed are based on cond ucting in-depth one-to-one interviews of all the key personnel involved with development and use of spreadsheets within the department. All the interviews were recorded and then transcribed and analysed. The authors initially presented the models INFORM S, 2006 and the feedback from that has been incorporated into the discussion. 3. FINDINGS: The spreadsheets were an integral part of the case study department. On one extre me they were used for designing basic paper forms or data stor es, whereas on the other extreme they were used for budgeting and forecasting, which formed th e more strategic use of spreadsheets. 3.1 Model 1: Dimensions for Model 1 (Ref. Figure 1): • Use: The categories for this dimension of the model were based on the type of use of the spreadsheet. The use of spread sheets within the department was significant. They were Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 39 mainly used as a data source. Some of the employees used complex models too, for budgeting and forecasting. Therefore the spreadsheets could be classified as being ‘Trivial’ data sources or ‘Strategic’ spreadsheets. Further analysis of the interviews revealed that within the Stra tegic spreadsheets, there were calculative (The spreadsheets used for budgeting and forecasting) and non-cal culative spreadsheets (For exam ple, The UWIC Rider Bible which recorded the details of the student passes for UWIC Bus service). Therefore the first model had three categories within use. 1. Trivial Informative 2. Strategic (Non Calculative/ Informative) 3. Strategic Calculative. • Importance: This dimension was based purel y on reliance on the information contained within the Spreadsheet. Therefor e the three categories produced: 1. Not important/ Little Important 2. Important 3. Critical • Risk: For this dimension the conventiona l categorisation was used. Any definition of risk is likely to carry an element of subjectivity, depending upon the nature of the risk and to what it is applied. (Riabokon, 2004) As such there is no all encompassing definition of risk. Chicken & Posner (1998) acknowledge this, and instead provide their interpretation of what a risk constituents: Risk = Hazard x Exposure They define hazard as “... the way in which a thing or situation can cause harm,” (ibid) and exposure as “…The extent to which the likel y recipient of the harm can be influenced by the hazard” (ibid). Therefore risk in this case can be assessed on probability of information being incorrect or erroneous and the extent of problems that can be caused by it being erroneous. The problems or the loss can be financial, operative or administrative. Risk, therefore, is measured in terms of impact and likelihood. The refore the three categories proposed for this model were: 1. Low 2. Medium 3. High Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 40 Risk Importance High Medium Low Strategic Calculative Strategic Non-Calculative Trivial Informative Little/Not Im p ortant Important Critical Use Figure 1: Model 1 Discussion for Model 1 (Refer: Figure 1): This model highlights 27 di fferent categories (3 X 3 X 3 Matrix) of spreadsheet usage. The research group at UWIC discussed the above mode l and it was highlighted that t here is some overlap within the categories of ‘Use’. Thus it was proposed that it might be worth reducing t he use categories to Calculative and Non-Calculative and the spreadsheets that are used for strategic purposes can be categorised on the level of ‘Importance’. Thus a new framework for categorisation was proposed (Refer: Figure 2), with just two categories of ‘Use’ i.e. Calculative and Non-calculative. Risk Importance High Medium Low Calculative Non-Calculative Little/Not Im p ortant Important Critical Use Figure 2: Model 1 (Modified) Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 41 3.2 Model 2 This model was considered to be acceptable specific to the case stu dy department for the pilot but the classification was considered more complex. As can be seen there seems to be some overlap between ‘Risk’ and ‘Importance’. For example, something that represents a risk can be assu med to be important to the organisation. Con sideri ng the complexity of the above model, another classification has been proposed (Refer: Figure 3). This model emphasise Importance vs. Urgency. Dimensions for Model 2 (Refer: Figure 3): • The Importance means that dealing with that spreadsheet results in a high pay-off. • Urgent means tight deadlines are associated with it. (The urgency dimension was inspired by Pawel J. Kalczynski (2006) paper presented at UKAIS Conference 2006.) One of the reasons why spreadsheets are commonly used is that they are quick and easy to use tools. Most of the organisations can easily differentiate what is urgent and what is not. Importance (High/Low Pay-off) Urgency (Deadlines) Section 4 Section 3 Section 1 Section 2 Discussion: This section now describes the individual sections of the model along with the pr oposed approach that can be followed for these sections. • Section 1: Low Importance and Low Urgency: Do nothing • Section 2: Low Importance and High Urgency: This is the situation in which spreadsheets, being the quick and easy-to-use tool, are commonly used. • Section 3: High Importance and High Urgency: This is the category of spreadsheet is critical and the organisation requires to put management controls in place. Complexity Figure 3: Model 2 High High Low Low Risk Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 42 • Section 4: High Importance and Low Urgency: In this category, as the urgency is low, it might be better to use other methods, like database etc. This model is very simple to implement and a pply on individual basis, but there are further two dimensions, which need to be addressed, i.e. ‘Complexity’ and ‘Risk’, thereby making it complex and hard to implement in big organisations. Risk in this model is weighted by assessing mana gement structures in place for three variables: (Refer: Figure 4) 1. Spreadsheet Error 2. Control 3. Compliance Compliance Control Risk Awareness Spreadsheet Errors Figure 4: Three variables for Ri sk measurement for Model 2 Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 43 3.3 Model 3 The overlap between the ‘Use’ and ‘Importance’ in Model 1, the fuzziness between the ‘Risk’ and ‘Importance’ in Mode l 1 (modified), and pr oblems with implementing Model 2 in bi g and complex organisations, lead the researcher to propose another model (Model 3: Refer Figure 5). This model works on more conventional approaches towards Risk. Dimensions for Model 3 (Refer: Figure 5): • The X-Axis is to classify the ‘Magnitude’ of risk i.e. in other words the classification for this dimension can be based on severity of the consequences of errors within spreadsheets, which can be financial or busi ness risk (which can also include reputation and compliance). • The Y axis highlights the ‘Dependency’, which can be operational, tactical or strategic. • The ‘Urgency’ dimension from Model 2 can also be incorporated into this model. X - Magnitude Y - Dependency Z – Time/Urgency Figure 5: Model 3 Discussion: When defining the ‘Dependency’ dimension, as mentioned earlier, the classification can be strategic, operational or tactical. Another possibility is the PWC (2004) classification as defined below, which is mainly for the financial domain. 1. Operational: Spreadsheets used to facilitate tracking and monitoring of workflow to support operational processes. 2. Analytical/Management Information: Spreadsheets used to support analytical review and management decision making. These may be used to evaluate the reasonableness of financial amounts. 3. Financial: Spreadsheets used to directly determine financial statement transaction amounts or balances that are populated into the general ledger and/or financial statements. Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 44 4. COMPARISON OF THE THRE E MODELS: The categorisation of the first model derived from th e pilot study can be considered to be specific to this case study department. Considering the spectrum of use of spr eadsheets within large organisations Model 1 seems the most appropriate. The authors suggest that it might be complex to segregate into one of the 27 categories, therefore considering the practical application Model 2 was proposed. This m odel is simple to apply practically but it is weaker as there are two furt her possible dimensions (Complexity and Risk). This might need to be considered in organisations larger than the pilot organisation. Further thi s model is mainly for designing/development of ne w spreadsheets, and it does not take into account the thousands of existing spreadsheets which might be in use within big organisations. Even as far as the case study organisation is concerned, most of the spreadsheets tend to be in Section 1 of Model 2 (Figure 3). Within this department the level of urgency is low, because it concerns maintaining regular records and genera ting feedback at the end of year. Model 3 uses a more understandable terminology wi thin the majority of organisations. This aspect makes it easier to understand and implem ent in different types of organisations. Furthermore the authors believe that for the dime nsio ns in this model it is easier to define criteria and define categories. Means of measuring is yet to be investigated. 5. CONCLUSION: The spectrum of spreadsheet use within the pilot study organisation was very diverse. The research suggests that the first model proposed by the authors was simple but the key problem encountered within this model was the difficulty to classify a specific spreadsheet within one of the 27 categories of spreadsheets. But the s upportive argument is that it does cover use of spreadsheets within organisation well. The Model 2 on the other hand is also simple but easier to understand. Findings suggest that this model is also easy to apply gene rally, but one might need to conside r two further dimensions (Risk and Complexity) when considering bigg er organisations. Emphasis is placed on new spreadsheet development, and there is some fuzzine ss in dealing with thousands of spreadsheets already existing within the organisation. According to the analysis the Model 3 seems to be the most acceptable for categorising spreadsheets. The primary reason is that it uses more conventional and un iversally understandable terminology and could be applied to a wide range of organisations. More specifically the dimensions are easier to understand, therefore the model is easier to implement. The authors perceive that it would be easier categorise us ing the Model 3 dimensions, but the means of measurement and categorisation are yet to be inv estigated. The next stage of the research is to develop clear definitions of each of the dimens ions i.e. Magnitude and Dependence and then investigate appropriate criteria to measure and develop specific categories. 6. REFERENCES: Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 45 • Bell, J. (1993), Doing Your Research Project: A Gu ide for First-time Researchers in Education and Social Science, Open University Press, 2 nd Edition. • Galletta, D. F., et al (1993), An Empirical Study of Spreadsheet Error – Finding Performance’, Accounting, Management and Info rmation Technol ogies, 3(2). • Kalczynski, P. J. (2006), Representing Fuzziness in the Onto logy of Time for Semantic Web, UKAIS Conference Proceedings, held at University of Gloucestershire, April 9-11. • Panko, R. (1996), Spreadsheets on Trial, 29 th Annual Hawaii International Conference on System Sciences. • Panko, R. and Ordway, N. (2005), Sarbanes Oxley: What About All the Spreadsheets? EuSpRIG Conference Proceedings, Univ ersity of Greenwich, July 7-8. • Price Waterhouse Coopers (2004), The Use of Spreadsheets: Considerations for Section 404 of the Sarbanes-Oxley Act , Whitepaper published in July 2004. Available from: http://www.pwcglobal.com/extweb/service.nsf/docid/CD287E 403C0AEB7185256F0800 7F8CAA • Rajalingham, K. (2005), A Revised Classification of Spreadshe et Errors, EuSpRIG Conference Proceedings, University of Greenwich, July 7-8. • Rajalingham, K., Chadwick, D. R. and Knight, B. (2000), Classification of Spreadsheet Errors, EuSpRIG Conference Proceedings, Univ ersity of Greenwich, July 7-8. • Saunders, M. Lewis, P. and Thornhill, A. (2006), Research Methods for Business Students, Prentice Hall Financial Times, 4 th Edition. • Chicken, C & Posner, T (1998) The Philosophy of Risk , Londo n, Thomas Telford • Riabokon, V. (1998) Risk, Available from http://www.energy- markets.com/reports/RISKColum n.pdf Accessed on 10 May 2005. Categorisation of Spreadsheet Use withi n Organisations: A Progress Report Madahar, Cleary & Ball 46 Blank Page

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment