Posterior model probabilities computed from model-specific Gibbs output

Reversible jump Markov chain Monte Carlo (RJMCMC) extends ordinary MCMC methods for use in Bayesian multimodel inference. We show that RJMCMC can be implemented as Gibbs sampling with alternating updates of a model indicator and a vector-valued "pale…

Authors: Richard J. Barker, William A. Link

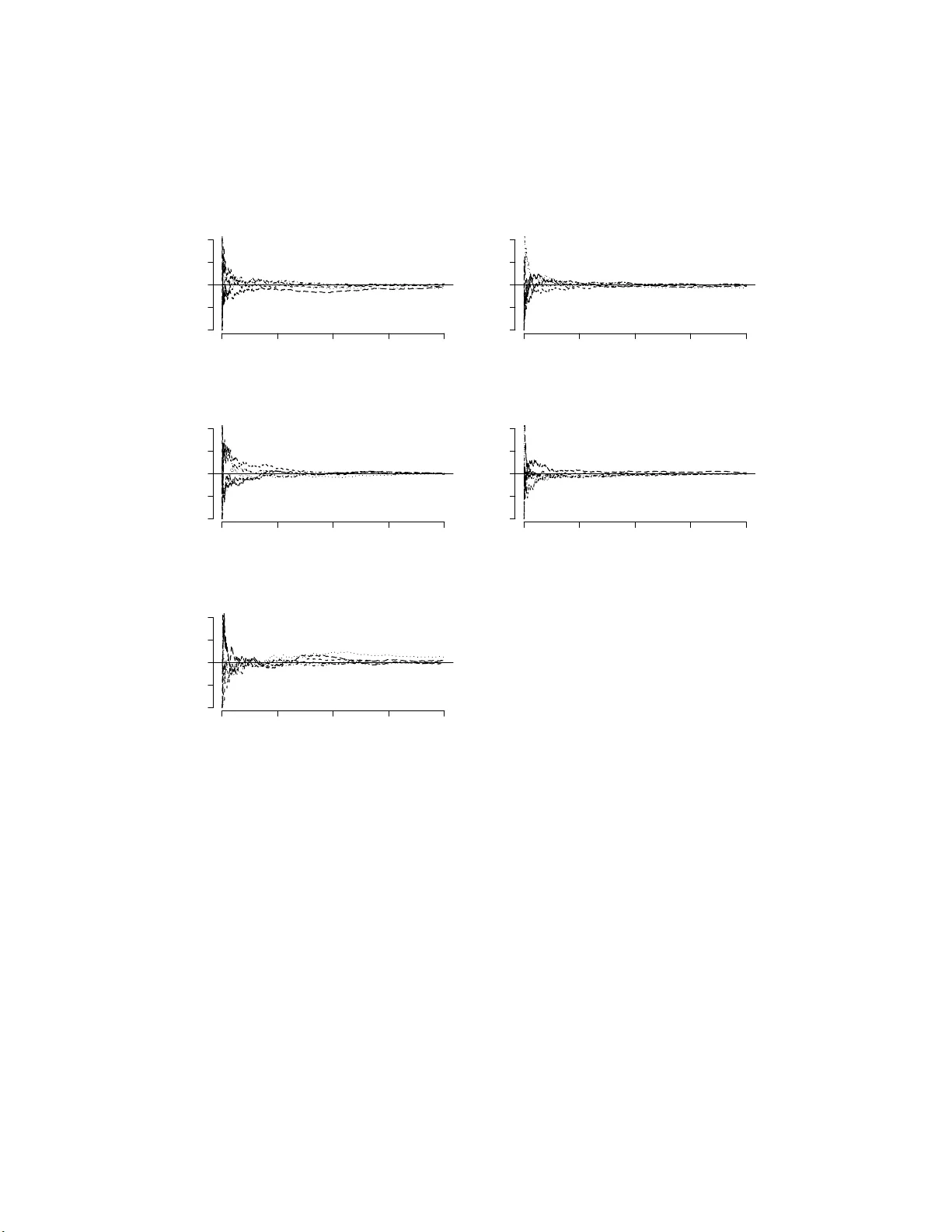

P osterior Mo del Probabilities Computed F rom Mo del-Sp ecific Gibbs Output Ric hard J. Bar k er ∗ and Willi am A. Link † Octob er 2 3, 201 8 Rev ersible jump Mark ov c hain Monte Carlo (RJMCMC) extends ordinary MCMC metho ds for use in Bay esian m ultimo del inference. W e show that RJMCMC can b e implemen ted as Gibbs sampling with alternating up dates of a mo del indicator and a v ector-v alued “palette” of parameters denoted ψ . Lik e an artist uses the palette to mix dabs of color fo r sp ecific needs, w e create mo del-sp ecific parameters f r o m the set av aila ble in ψ . This descrip- tion not only remov es some o f the my stery of R JMCMC, but also pro vides a basis f o r fitting mo dels one at a time using ordinary MCMC and computing mo del we igh ts or Bay es factors by p ost-pro cessing the Mon te Carlo output. ∗ Department of Mathematics and Statistics, Universit y of O tago, P .O. B ox 56 Dunedin, New Zea land † Patuxen t Wildlife Research Center, Laurel, MD 2 0708, USA 1 W e illustrate our pro cedure using sev eral examples . KEY W O R DS: Rev ersible jump Mark ov c ha in Mon te Carlo, Bay esian m ul- timo del inference, Bay es factors, Poste rior mo del pro babilities. 1 In tro duct i on A natural Bay esian approach to pro blems of m ultimo del inference is to com- pute p osterior mo del probabilities, or equiv alently Ba y es factors, given priors and data. Ba y es factors in v olve marginal lik eliho o ds and can b e difficult to calculate. Here w e address the problem of estimating p osterior mo del proba- bilities, and pro vide a represen ta tion of rev ersible jump Mark o v c hain Mon te Carlo (RJMCM C) that allo ws us to use MCMC o ut put obtained fitting mo d- els one at a time. T ec hniques ha v e been prop osed for computing Bay es factors using MCMC output from indep enden t c hains generated for differen t mo dels (f o r example, Chib 1995) or b y using a searc h ov er the join t space of mo del indicators M ∈ M and mo del parameters θ j ∈ Θ j giv en by M × Q j ∈M Θ j . Either approac h is difficult in practice and it is common for mo del selection to b e based instead on a deviance information criterion (D IC) (Spiegelhalter et al. 2002). How ev er, there is no theoretical justification for using DIC to pro duce mo del w eigh ts or Ba yes factors. 2 Rev ersible jump Mark o v c ha in Mon te Carlo is an extension of o rdinary MCMC, for m ultimo del inference. In this broader context, the p osterior dis- tribution under in v estigation describ es par ameters for a collection of mo dels, rather than a single mo del; furthermore the p o sterior distribution describ es mo del uncertain t y through we igh ts on a categorical v ar ia ble w e call Mo d el . A k ey step in implemen ting RJMCMC is the specification of bijections de- scribing relationships b etw een the parameters of v arious mo dels (e.g., G reen 1995; Gelman et al. 20 04). RJMCMC is usually describ ed in terms of K 2 suc h bijections where K is the n um b er of mo dels in the mo del set M . Link and Bark er (2010) outlined an alternative form ula t ion of RJMCMC as simple Gibbs sampling, alternating b et w een up dating a palette of parameters ψ , whic h is of the same dimension for all models, a nd the categorical v ariable Mo del . There are K bijections, one relating eac h mo del’s parameters to the palette ψ ; the K 2 bijections typic ally describ ed are obtained fro m these. Careful construction of the palette and K bijections allo ws RJMCMC to be carried out using samples from mo del-sp ecific p osteriors, obtained one mo del at a time. Here we illustrate this approac h and extend Link and Barker (2010) b y showing that mov es b et w een mo dels can b e written so that they in v olve a direct draw from a kno wn categorical distribution with all mo dels in the sample space . This formulation ob viates the need for use o f a Metrop olis- Hastings step that only allow s pair-wise comparison of mo dels and can b e easier to implemen t than RJMCMC in its usual incarnations. 3 2 A d escripti on of RJMCMC Supp ose that w e wish to ev aluate the relative suppo rt provided b y data y to mo dels M k , k = 1 , 2 , . . . , K , these mo dels b eing fully know n except for parameter v ectors θ ( k ) for whic h w e ha ve specified priors. RJMCMC can b e expressed as simple Gibbs sampling, with dra ws alter- nating betw een the categorical v ariable Mo del a nd a univ ersal vec tor-v alued parameter ψ . W e compare ψ to an ar tist’s palette: as the artist com bines colors on her palette to pro duce colors needed for sp ecific a pplications, so comp onen ts of ψ are combined to pro duce mo del-specific parameters θ ( k ) . The impo rtan t feature of RJMCMC is that the en tire palette ψ is updat ed at each step of the Gibbs sampler (rather than simply those comp onen ts relating to the presen t mo del). F ollow ing Link and Bark er (2010) the palette of parameters ψ is a v ector of dimension d greater than or equal to t he dimension of the most com- plex mo del in the mo del set. P ara meter v ector θ ( k ) can b e reco v ered fro m the palette ψ b y means of a known (in v ertible) mapping g k ( ψ ) = Θ ( k ) = ( θ ( k ) , u ( k ) ) ′ . V ector u ( k ) is irr elev ant to mo del M k , serving only to matc h the dimension of Θ ( k ) and ψ , so that g k ( · ) can b e defined as a bijection. Th us if mo del M 2 has parameter space of dimension 7 , and d = 10, v ector u (2) will ha v e dimension 3. Note that the K 2 bijections typically required for RJMCMC are induced b y our K bijections b et w een the palette and mo del-sp ecific parameter spaces: 4 for mo dels M j and M k w e hav e g j k ( Θ ( j ) ) ≡ g k ◦ g − 1 j ( Θ ( j ) ) = g k ( ψ ) = Θ ( k ) . W e m ust sp ecify a prior for ψ and in doing so accommo da te mo del sp ecific priors [ θ ( k ) | M odel = M k ], whic h for simplicit y we write a s [ θ ( k ) | M k ]. W e hav e [ Θ ( k ) | M k ] = [ θ ( k ) , u ( k ) | M k ] = [ θ ( k ) | M k ] [ u ( k ) | θ ( k ) , M k ] . All that is needed is a sp ecification of [ u ( k ) | θ ( k ) , M k ]; given that u ( k ) has no role in inference, it will b e con v enien t to assume it is conditiona lly indep en- den t of θ ( k ) , so that [ u ( k ) | θ ( k ) , M k ] = [ u ( k ) | M k ]. The sp ecific c hoice do es not mat ter, except fo r tuning the RJMCMC alg orithm. F rom [ Θ ( k ) | M k ] w e obta in [ ψ | M k ] using the c ha ng e of v ariables theorem in terms o f a prio r f k ( Θ ( k ) ) = [ θ ( k ) , u ( k ) | M k ]. The prior on ψ is then [ ψ ] = X k [ ψ | M k ][ M k ] where [ ψ | M k ] = f k ( g k ( ψ )) ∂ g k ( ψ ) ∂ ψ . (1) Under this formu lation, Gibbs sampling consists of cyclical sampling of full conditional distributions, alternating b et w een draws from [ ψ | M k , y ] to up date ψ , and f rom [ { M 1 , . . . , M K }| ψ , y ] to up date Mo del . 5 Up dating ψ T o dra w from the full conditional [ ψ | M k , y ] it suffices to dra w from [ θ ( k ) | M k , y ] and [ u ( k ) | M k ] and then to apply the in vers e transformation g − 1 k ( Θ ( k ) ) to ob- tain a dra w for ψ . The dra w from [ θ ( k ) | M k , y ] can either b e made directly , if the distribution is of con v enien t for m, or b y simulation. Another po ssibilit y , often an a t trac- tiv e alternative , is to take a random draw from the stored MCMC output of an earlier analysis of mo del M k . Up dating the mo del The full-conditional for Mo del is categor ical with probabilities: Pr( M k | · ) = [ y | ψ , M k ][ ψ | M k ][ M k ] P j [ y | ψ , M j ][ ψ | M j ][ M j ] , for k = 1 , . . . , K . If w e a r e willing to calculate all of these probabilities, w e can up date Mo del by a direct draw from this f ull-conditional distribution. Chain means of mo del indicato rs I ( M odel = M k ) con v erge to the full condi- tional mo del probabilities, but greater efficiency is a v ailable b y using c hain means o f the full conditional mo del probabilities, whic h also conv erge to the p osterior mo del probabilities. As an alternativ e, w e can up dat e mo del indicators b y a Metrop o lis- Hastings step if the mo del candidate generator only allo ws limited transitions, for example, to a near neigh b or in a graphical mo del sense. The adv antage 6 of this approac h is that w e compute a smaller set of categorical pr o babilities, corresp onding to the neighborho o d set. In this case w e m ust compute p o s- terior mo del probabilities by c hain means of indicators I ( M o del = M k ). Expressing RJMCMC as simple G ibbs sampling provides the key innov a- tion of our fo rm ula tion: it allo ws us to fit mo dels one at a time using ordinary MCMC and then compute mo del w eights or Ba y es fa ctors b y p ost-pro cessing the Mon te Carlo output. Th us, w e hav e a simple 2-stage pro cedure that can b e used for computing mo del pr o babilities: Stage 1: P ro duce samples of [ ψ | y , M k ] for eac h k . Begin b y sampling [ θ ( k ) | y , M k ]. This can b e a ccomplished b y running a n MCMC sampler fo r M k , pro cessing it in the usual wa y , discarding a n y ini- tial burn-in iterations, and storing the results. (In cases where the p osterior distribution for θ ( k ) is of a kno wn and easily sampled form, w e do so.) F or eac h sampled v alue θ ( k ) , inde p enden t ly sample an auxiliary v ariable u ( k ) from [ u ( k ) | M k ] and calculate ψ = g − 1 k (( θ ( k ) , u ( k ) ) ′ ). The collection of sampled v al- ues ψ is a sample of [ ψ | y , M k ]. Stage 2: Post-pro cess the mo del sp ecific outputs. P o sterior mo del probabilities can b e computed in one of t wo w a ys. The first metho d is based on generating a Marko v chain of the categorical v ariable 7 Mo del that can b e used a s a p osterior sample from [ M o del | y ]. The second metho d is based on generating a Marko v c hain of b etw een-mo del transition probabilities that can b e used to estimate t he b etw een-mo del transition ma- trix. The steady state marginal distribution of this matrix corresp onds to the p osterior mo del probabilities. Metho d 1 A p osterior sample Mo del (1) , Mo del (2) , . . . , Mo del ( j ) , . . . can b e generated as follows : (a) Initialize Mo d el , sa y with M od el (1) = M 1 . (b) Iterate fr o m j = 1 to some large num b er J , and at eac h step: (i) If Mo del ( j ) = M k , draw a v alue ψ ( j ) from the stored sample of [ ψ | y , M k ] from Stage 1. (ii) Compute π ( j ) k = Pr( M odel = M k | ψ ( j ) , y ), for each k . This calcu- lation requires the Jacobian of the transformation Θ ( k ) = g k ( ψ ) as in eq. (1), ev aluated a t ψ ( j ) . (iii) Sample Mo del ( j +1) from a categorical distribution with sample space { M 1 , M 2 , . . . , M K } and probabilit y v ector π ( j ) = π ( j ) 1 , π ( j ) 2 , . . . , π ( j ) K ′ . The relative frequency with whic h M odel ( j ) = M k appro ximates the p oste- rior mo del proba bility for M k . A b etter estimate (Rao-Blackw ellized) is the c ha in mean of v a lues π ( j ) k . 8 Metho d 2 A further impro v emen t on this appro ximation can b e made b y mar g inalizing at stage 1, ob viating the need for the construction of a Mark ov c hain of mo del indicators in the second stage. F or eac h mo del w e can compute Pr( M k | ψ , M h ) forming a Marko v chain o f transition probabili- ties f rom mo del h to mo del k ( h, k ∈ 1 , . . . , K ). These can then b e a v era g ed to form an a pproximation to the sto chastic matrix gov erning mo del-to - mo del transitions. Giv en an estimate of this tra nsition matrix we can obtain corre- sp onding estimates of the p osterior mo del probabilities as the limiting distri- bution obtainable b y normalizing the left eigen v ector of the transition matrix asso ciated with the eigen v alue 1.0 (Seb er 2 008). 3 Examples 3.1 Radiata pine data Carlin and Chib (1995), Han and Carlin (20 01), a nd man y others a nalyze data take n fro m Williams (1 959). The resp onse v ariable y i is the maxim um compressiv e strength parallel to the grain fo r 42 radiata pine b oards. Two explanatory v ariables are considered: the first is the sp ecimen’s densit y , x i , and the second is the sp ecimen’s densit y ha ving adjusted f or resin conten t, z i . Resin increases the densit y of b oards without increasing their compress iv e 9 strength. Carlin and Chib (199 5) considered t w o mo dels: Mo del 1: y i = α + β ( x i − ¯ x ) + ε i , ε i ∼ N (0 , σ 2 x ) and Mo del 2: y i = γ + δ ( z i − ¯ z ) + ε i , ε i ∼ N (0 , σ 2 z ) . In b oth cases the error s ε are a ssumed iid among observ ations, conditional on the parameters. As priors, Carlin and Chib (1995) used N (( 3 000 , 185) ′ , diag(1 0 6 , 10 4 )) pri- ors on ( α, β ) ′ and ( γ , δ ) ′ , and inv erse gamma priors on σ 2 x and σ 2 z , b oth ha ving mean a nd standard deviation equal to 300 2 . This quirky choice of priors w as made to b e v ague but with exp ectations corresp onding roughly to the pa- rameter estimates obtained by fitting t he mo del b y least squares. W e fitted eac h of these mo dels indep enden tly using BUGS (Lunn et al. 2000) and the ab o v e priors, running three c hains of 60,000 eac h with distinct starting v alues. D iscarding the first 10,000 of eac h c hain as a burn- in left us with a p osterior sample of 1 5 0,000 for θ (1) and θ (2) . W e co ded a rev ersible jump algorithm in whic h g 1 ( ψ ) = ( α, β , σ 2 x ) ′ and g 2 ( ψ ) = ( γ , δ, σ 2 z ) ′ . In this case, [ ψ | M 1 ] = [ ψ | M 2 ], and the mo del up date is based on t he relativ e v alues 10 of the lik eliho o ds w eigh ted b y the mo del prior s Pr( M k ): Pr( M k | y , ψ ) = Pr( M k ) e − 1 2 ψ 3 P 42 i =1 ( y i − µ ik ) 2 Pr( M 1 ) e − 1 2 ψ 3 P 42 i =1 ( y i − µ i 1 ) 2 + Pr( M 2 ) e − 1 2 ψ 3 P 42 i =1 ( y i − µ i 2 ) 2 , where µ ik = ψ 1 + ψ 2 ( x i − ¯ x ) k = 1 ψ 1 + ψ 2 ( z i − ¯ z ) k = 2 . F ollow ing Han and Carlin (2001) we assigned mo del prio r s of Pr( M 1 ) = 0 . 9995 and Pr( M 2 ) = 0 . 0005 to ensure that t he t w o mo dels w ere visited in roughly equal prop o rtion. Starting at mo del 1 or model 2 the chain fo r the p osterior model probabilit y conv erges rapidly (Figur e 1). Aft er running the t w o c hains for 20 0,000 iterations a nd discarding the first 100 ,0 00 as a burn- in, our estimate of the p osterior mo del probabilit y w as 0.709 correspo nding to a Ba y es factor B F 21 of 4870 . These are in close agreemen t with the exact v alues o f Pr( M 2 | y ) = 0 . 70865 and B F 21 = 486 2 rep orted b y Han a nd Carlin (2001). Figure 1 ab out here Using our second metho d, w e sampled 200,000 v alues of ψ from each c ha in h , and for the i th sample w e calculated Pr( M k | ψ ( i ) , M h ) ( k = 1 , 2). Av eraging across i w e obtain an estimated transition matrix of : 0 . 6003 0 . 3997 0 . 1651 0 . 8349 11 with steady-state marg ina l distribution of (0 . 2924 , 0 . 7076) ′ , corresp onding to B F 21 = 483 8. 3.2 T rout return rates Link and Bark er (200 6) rep o rt an a nalysis based on fitting logistic regression mo dels to the return rates fo r bro wn trout expressed in terms of sex S i and length L i effects. Mo deling the return indicator y i ∼ B er n ( p i ) they considered fiv e mo dels: 1. η i = β 0 2. η i = β 0 + β 1 S i 3. η i = β 0 + β 2 L i 4. η i = β 0 + β 1 S i + β 2 L i 5. η i = β 0 + β 1 S i + β 2 L i + β 3 S i L i where η i = logit( p i ). Link and Bark er (2006) used the fo llo wing priors on parameters: [ β k | V , M k ] = N (0 , V − 1 ) k = 1 N (0 , (2 V ) − 1 ) k = 2 N (0 , (2 V ) − 1 ) k = 3 N (0 , (3 V ) − 1 ) k = 4 N (0 , (4 V ) − 1 ) k = 5 12 where V has a Ga (3 . 29 , 7 . 8 0) prior distribution. This c hoice w as motiv ated b y the observ ation tha t if lo git( p ) ∼ N (0 , V − 1 ) and V ∼ Γ(3 . 29 , 7 . 80) , then the marginal distribution o f p is v ery nearly uniform on [0,1]. With S i and L i ha ving b een standardized, these choices of priors ensure that the prior on e η i / (1 − e η i ) = p i is appro ximately U (0 , 1 ) for S i = ± 1 and L i ± 1. P alette and bijections Eac h elemen t of ψ is directly asso ciated with either an elemen t o f the beta v ector or with a supplemen ta l v ariable u (T able 1): The parameter V is part Mo del ψ 1 2 3 4 5 ψ 1 β 0 β 0 β 0 β 0 β 0 ψ 2 u 1 β 1 u 1 β 1 β 1 ψ 3 u 2 u 1 β 2 β 2 β 2 ψ 4 u 3 u 2 u 2 u 1 β 12 T a ble 1: Association b et w een elemen ts of ψ and elemen ts o f β k , sp ecific parameters for mo del M k and suppleme n tal v ariables u k used in mo del M k for matc hing the parameter dimension t o ψ . of the prior sp ecification and is common to all mo dels so w e c hose to lea ve it out of the palette sp ecification, althoug h this is not necessary . Up dates for V were stored when eac h mo del was fitted. F or a particular mo del, the priors on the supplemen tal v ariables w ere the same as the prio r s used fo r the β co efficien ts in that mo del, and in eac h case the Jacobian of the t r ansformation from θ ( k ) to ψ is an iden tit y matrix of dimension 5. 13 As a n example, Mo del 1 (constan t only) has parameter v ector θ (1) = β 0 with supplemen tal v ariables u (1) = ( u 1 , u 2 , u 3 ) ′ . Th us g 1 ( ψ ) = g 1 ψ 1 . . . ψ 4 = Θ (1) = β 0 u 1 u 2 u 3 = ψ 1 . . . ψ 4 , leading to: [ ψ | M 1 , V ] = f 1 ( g 1 ( ψ )) ∂ g 1 ( ψ ) ∂ ψ = N ( ψ 1 ; 0 , V − 1 ) × N ( ψ 2 ; 0 , V − 1 ) × N ( ψ 3 ; 0 , V − 1 ) × N ( ψ 4 ; 0 , V − 1 ) × Ga ( V ; 3 . 2 9 , 7 . 80 ) × | I 5 | . Rep eating this pro cess fo r eac h mo del w e obtain the mo del- sp ecific priors: [ ψ | M k , V ] = 4 Y i =1 N ( ψ i ; 0 , ( n k V ) − 1 ) × Ga ( V ; 3 . 29 , 7 . 80) × | I 5 | where n k is the dimension of the v ector β ( k ) . F or generating a c hain of mo del indicators, we used a direct draw from the full conditional: Pr( M k | ψ , V ) = Pr( M k ) Q 4 i =1 q n k V 2 π e − n k V 2 ψ 2 i Q 1961 j = 1 p ( k ) j (1 − p ( k ) j ) P 5 h =1 Pr( M h ) Q 4 i =1 q n h V 2 π e − n h V 2 ψ 2 i Q 1961 j = 1 p ( h ) j (1 − p ( h ) j ) 14 where logit( p ( k ) i ) = x ′ i β ( k ) . T o estimate the Bay es factors w e first fitted the fiv e mo dels, in each case com bining results from three differen t chains o f length 500,0 00 after discarding a burn-in. W e then generated fiv e c hains using our Gibbs sampler for the mo del indic ator, starting eac h c hain with a different model. F ollow ing Link and Bark er (2006) w e first tuned the Gibbs sampler to visit eac h mo del in roughly equal prop ortion. Mixing of the mo del indicators app ears rapid (Figure 2) and agreemen t with the Link and Bark er (2006) estimates is g o o d after com bining the results fr om the second half of 200 ,000 iterations of the fiv e c hains (T able 2 ) . j BF 1 j Pr( M j | y ) 1 1 (1 ) 0.893 (0.894) 2 31.3 (31.7) 0.029 (0.028) 3 12.3 (12.4) 0.073 (0.072) 4 274.6 (281.7) 0.003 (0.003) 5 383.4 ( 390.1) 0.002 (0.002) T a ble 2: Estimates of Bay es f a ctors BF 1 j for comparing mo dels 1 and j and estimates of p osterior mo del probabilities under constan t prior mo del probabilities Pr( M j ) = 0 . 2. Corresp onding estimates from Link and Barker (2006) are giv en in paren theses. Figure 2 ab out here F or metho d t wo w e drew a sample of 10,000 v alues for ψ from each chain 15 1 leading to an estimate of the transition matrix o f: 0 . 8172 0 . 0870 0 . 0847 0 . 0088 0 . 0024 0 . 0858 0 . 8086 0 . 0107 0 . 0755 0 . 0195 0 . 0854 0 . 0102 0 . 8233 0 . 0759 0 . 0052 0 . 0081 0 . 0749 0 . 0781 0 . 7884 0 . 0504 0 . 0026 0 . 0176 0 . 0057 0 . 0498 0 . 9244 with steady-state marginal distribution 0 . 1986 0 . 1975 0 . 2016 0 . 1989 0 . 2034 . 3.3 Simple binomial In b ot h of the ab ov e examples, the bijections from ψ t o θ are simple 1-1 mappings with the Ja cobian of the transformatio n an identit y matrix. Now consider an example where Y i ∼ B ( N i , p i ) and w e ha ve observ ations y 1 = 8, n 1 = 20, y 2 = 16, and n 2 = 30. What is t he evidence for p 1 6 = p 2 against p 1 = p 2 = π ? T o compute an appropriate Bay es factor w e fit t w o mo dels: 1. Mo del 1 : ( p 1 , p 2 ) with indep enden t B e ( α p , β p ) priors 1 Only 10,000 samples were dra wn due to the large RAM requirements on the desktop. This num b er can eas ily b e increa sed b y writing batches of suc h draws to the ha rd-drive. 16 2. Mo del 2 : p 1 = p 2 = π with a B e ( α π , β π ) prior on π . F or mo del 1, w e assign ψ = ( p 1 , p 2 ) ′ . It seems natural in mo ving from mo del 1 to model 2 that the a v erag e ¯ ψ = ( ψ 1 + ψ 2 ) / 2 should pro vide a go o d candidate for π . Th us, our bijections can b e written as: Mo del 1: I 2 × ψ = p 1 p 2 and Mo del 2: 1 / 2 1 / 2 0 1 × ψ 1 ψ 2 = π u , where I 2 is a 2 × 2 iden tity matrix and u an appropriate suppleme n tal v ariable Our Gibbs sampler then pro ceeds as fo llo ws: 1. Within mo dels the full conditional distributions fo r mo del-sp ecific pa- rameters are of known form since w e hav e conditional (on the mo del) conjugacy: - Under Mo del 1 w e sample p 1 ∼ B e (8 + α p , 12 + β p ) and p 2 ∼ B e (16 + α p , 14 + β p ) and then compute ψ = ( p 1 , p 2 ) ′ . - Under Mo del 2 w e sample π ∼ B e (24 + α π , 26 + β π ) and u ∼ B e ( α u , β u ) and then set ψ 1 = 2 π − u and ψ 2 = u . 2. Betw een mo dels we set: 17 - Pr( M 1 |· ) ∝ Pr( M 1 ) × ψ 8+ α p 1 (1 − ψ 1 ) 12+ β p ψ 16+ α p 2 (1 − ψ 2 ) 14+ β p 1 ψ 1 ∈ (0 , 1) 1 ψ 2 ∈ (0 , 1) - Pr( M 2 |· ) ∝ Pr( M 2 ) × ¯ ψ 24+ α π (1 − ¯ ψ ) 26+ β π 1 ¯ ψ ∈ (0 , 1) 1 ψ 2 ∈ (0 , 1) × 1 2 where 1 E denotes the indicator of the eve n t E and the prop ortiona l- it y constant is the same for eac h mo del. W e then sample the mo del indicator b y a direct draw from a cat ego rical distribution with sample space { 1 , 2 } and parameter v ector ( π 1 , π 2 ) ′ where π j = Pr( M j |· ) Pr( M 1 |· ) + Pr( M 2 |· ) . T o fit t he mo dels w e used as prior parameters α p = β p = α π = β π = 1 (i.e., indep enden t U (0 , 1) priors). W e also set α u = β u = 15 so that dra ws for u w ere similar to draws for p 2 . Con v ergence of the c ha in for the p osterior probabilit y o f mo del 2 w a s rapid (Figure 3). Combining results from 100,000 iterations of the t wo chains we obtained ˆ B 21 = 1 . 92 and Pr ( M 2 ) = 0 . 658. F or b oth mo dels the marginal distribution of the dat a is straight-forw ard to compute and the exact solution for the p osterior mo del probabilty is 0.658 0. Figure 3 ab out here Using metho d t w o with a sample of 100,000 v alues of ψ from eac h c hain w e estimate the transition matrix as: 0 . 4318 0 . 5682 0 . 2951 0 . 7049 18 with steady-state marginal distribution (0 . 34230 . 6577 ) ′ . 4 Discuss ion Ba y esian inference offers an app ealing f r a mew ork for m ultimo del inference but the difficulties of computing Bay es factors, or equiv alen tly p osterior mo del probabilities, can b e a barrier to implemen tation. Being a ble to in- dep enden tly fit mo dels and then p ost-pro cess them using RJMCMC as w e ha v e described here o ffers a partial solution to the problem. An issue of ten raised in ob jection to Ba ye sian m ultimo del inference (BMI) based o n Ba y es factors is that one m ust assume that the true mo del is in the mo del set. As w e ha v e argued elsewhe re (Link and Bark er 2006, 201 0), this is a red-herring – conditioning on a mo del set is no less inno cuous than conditioning on a mo del as m ust b e done for any f orm of statistical inference. Conditioning on mo dels a nd mo del sets is done for op erational con venie nce - w e no more b eliev e that truth is in our mo del set than w e b eliev e that the mo del y i iid ∼ N ( µ , σ 2 ) can ev er b e a true and complete represen tation of an y set of data. A more serious issue with BMI is priors on pa r ameters; it is w ell-kno wn that Bay es factors are sensitiv e to c hoice of priors, particularly v ague priors. Our view is that prio r s should b e c hosen so tha t common features o f interest in each mo del ha v e the same prior uncertain ty asso ciat ed with them. An attempt at suc h an approac h is illustrated b y the W est Coast trout example 19 in whic h priors w ere constructed based on the log it of the return probabilit y for trout that had t ypical v alues of the co v aria tes. Such an approac h w e hav e previously referred to as “nonpreferen tial” (Link and Bark er 2008). Choice of efficien t bijections fo r moving b etw een mo dels requires some though t. Althoug h our approa c h simplifies this pro blem to one of choosing K suc h bijections, choice s m ust b e made. F eatures that are of in terest and common across mo dels can b e exploited in c ho osing bijections as we ll a s pro viding a basis for constructing non-preferential priors. Generalized linear mo del formulations suc h as represe n ted in our trout example offers one means for constructing bijections. One area of p ossible fr uitful inv estigation in this con text is that o ur palette represen tatio n of R JMCMC a pp ears to b e connected to the use of imp ortance link functions MacEac hern and P eruggia (2000). There may b e b enefits from considering this connection fro m the p oin t of view of determining transformations g ( ψ ) in our represen ta tion that lead to more effic ien t Mon te Carlo estimation of p osterior mo del probabilities. Our description of RJMC MC as simple Gibbs sampling with a direct dra w from a kno wn distribution for mo del pro babilities is a further useful simpli- fication. Mo v es can b e made to any mo del in the set M using samples from the full-conditional distribution for mo del indicators; we are not restricted to mo v es b et w een pairs o f mo dels. Metho ds that in v o lv e mo v es to neigh b ours ha v e b een use d to automate searc h across v ery high dimens ional mo del space. W e are sk eptical ab out the v alue of suc h a lgorithms as they induce a partic- ular prior on parameters. Suc h default constructions ma y lead to prio rs that 20 are prejudicial in whic h case p osterior mo del probabilities w ould b e more a reflection of these prior prejudices than data -informed p osterior w eigh t ing . References Carlin, B. P . and Chib, S. (1995), “ Ba y esian mo del c hoice via Mark ov chain Mon t e Carlo metho ds.” Journal of the R oyal Statistic al So cie ty, Se ries B. , 57, 473–484. Chib, S. (1 995), “Marginal lik eliho o d from the Gibbs output.” Journal o f the A meric an Statistic al Asso ciation , 90, 1313–1321 . Gelman, A. B., Carlin, J. S., Stern, H. S., and Rubin, D. B. (2004), Bayesian data analysis. Se c ond e dition. , Chapman and Hall/CR C, Bo ca Rato n. Green, P . J. (1 9 95), “Rev ersible jump Mark o v chain Mon te Carlo computa- tion and Bay esian mo del determination.” Biometrika , 82, 711–732. Han, C. and Carlin, B. (20 0 1), “Mark o v chain Monte Carlo metho ds for computing Ba yes factors: a comparative review.” Journal of the Americ an Statistic al Asso ciation , 96, 1122–113 3. Link, W. a nd Bark er, R. (2008), “ Ba y es fa ctors and multimodel inference,” Envir onmental and Ec olo gic al Statistics , 3, 597–618. Link, W. A. and Bark er, R. J. (2006), “Mo del we igh ts and the foundations of m ulti- mo del inference,” Ec olo gy , 87, 2626–2635. 21 — (2010), Bayesian Infer enc e with e c o lo gic al applic ations , Academic Press. Lunn, D ., Thomas, A., Best, N., and Spiegelhalter, D. (200 0 ), “WinBUGS – a Ba y esian mo delling framew ork: concepts, structure, and extensibilit y .” Statistics and Computing , 10, 325–337. MacEac hern, S. N. and P eruggia, M. (200 0 ), “Imp ortance link function esti- mation for Mark ov c hain Monte Carlo methods,” Journal o f C omputational and , 9, 99–12 1 . Seb er, G. A. F . (20 08), A matrix handb o ok for s tatisticians , John Wiley and Sons, Hob oken, New Jersey . Spiegelhalter, D. J., Best, N. G., Carlin, B. P ., and v an der Linde, A. (20 0 2), “Ba y esian measures of mo del complexit y and fit.” Journal of the R oyal Statistic al So ciety series B , 64, 583– 639. Williams, E. (1959 ), R e gr ession A n alysis. , Wiley , New Y ork. 22 Inde x p 2 0 5000 10000 15000 0.5 0.6 0.7 0.8 Model = 1 Model = 2 Exact solution Figure 1: Index plot of the cum ulativ e p osterior probabilit y p = Pr ( M = 2) starting with mo del 1 (red) or mo del (2). The hor izontal blac k line corre- sp onds to the exact result. 23 Model 1 Inde x p 1 0 5000 10000 15000 20000 0.0 0.2 0.4 Model 2 Inde x p 1 0 5000 10000 15000 20000 0.0 0.2 0.4 Model 3 Inde x p 1 0 5000 10000 15000 20000 0.0 0.2 0.4 Model 4 Inde x p 1 0 5000 10000 15000 20000 0.0 0.2 0.4 Model 5 Inde x p 1 0 5000 10000 15000 20000 0.0 0.2 0.4 Figure 2: Index plot o f the cum ula t iv e p osterior mo del probabilities. Eac h plot represen ts a differen t mo del probability and the differen t colored c hains represen t different starting v alues. The blac k line corresp onds t o the v alue targeted during tuning. 24 Inde x p 2 0 2000 4000 6000 8000 10000 0.5 0.6 0.7 0.8 Model = 1 Model = 2 Exact solution Figure 3: Index plot of the cum ulativ e p osterior probabilit y p = Pr ( M = 2) starting with mo del 1 (red) or mo del (2). The hor izontal blac k line corre- sp onds to the exact result. 25

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment