Title: Expert System for Bitcoin Forecasting: Integrating Global Liquidity via TimeXer Transformers

ArXiv ID: 2512.22326

Date: 2025-12-26

Authors: Sravan Karthick T

📝 Abstract

Bitcoin price forecasting is characterized by extreme volatility and non-stationarity, often defying traditional univariate time-series models over long horizons. This paper addresses a critical gap by integrating Global M2 Liquidity, aggregated from 18 major economies, as a leading exogenous variable with a 12-week lag structure. Using the TimeXer architecture, we compare a liquidity-conditioned forecasting model (TimeXer-Exog) against state-of-the-art benchmarks including LSTM, N-BEATS, PatchTST, and a standard univariate TimeXer. Experiments conducted on daily Bitcoin price data from January 2020 to August 2025 demonstrate that explicit macroeconomic conditioning significantly stabilizes long-horizon forecasts. At a 70-day forecast horizon, the proposed TimeXer-Exog model achieves a mean squared error (MSE) 1.08e8, outperforming the univariate TimeXer baseline by over 89 percent. These results highlight that conditioning deep learning models on global liquidity provides substantial improvements in long-horizon Bitcoin price forecasting.

💡 Deep Analysis

📄 Full Content

Expert System for Bitcoin Forecasting: Integrating

Global Liquidity via TimeXer Transformers

Sravan Karthick T∗

RV College of Engineering (RVCE), Bengaluru, India

Rakshita A

RV College of Engineering (RVCE), Bengaluru, India

Dr. Minal Moharir

RV College of Engineering (RVCE), Bengaluru, India

Abstract

Bitcoin price forecasting is characterized by extreme volatility and non-stationarity, making

it hard for univariate time-series prediction models over long-horizons. By integrating Global

M2 Liquidity as an exogenous variable, aggregated from 18 major economies, we improve the

predictions over long-horizons.

Using TimeXer, we compare a liquidity-conditioned univariate forecasting model (TimeXer-

Exog) against state-of-the-art univariate models, Long Short-Term Memory(LSTM), Neural

Basis Expansion Analysis for interpretable Time-Series (N-BEATS), Patch Time-Series Trans-

former(PatchTST), and standard TimeXer. Experiments conducted on daily Bitcoin price data

from January 2020 to August 2025 demonstrate that explicit macroeconomic conditioning sig-

nificantly stabilizes long-horizon forecasts.

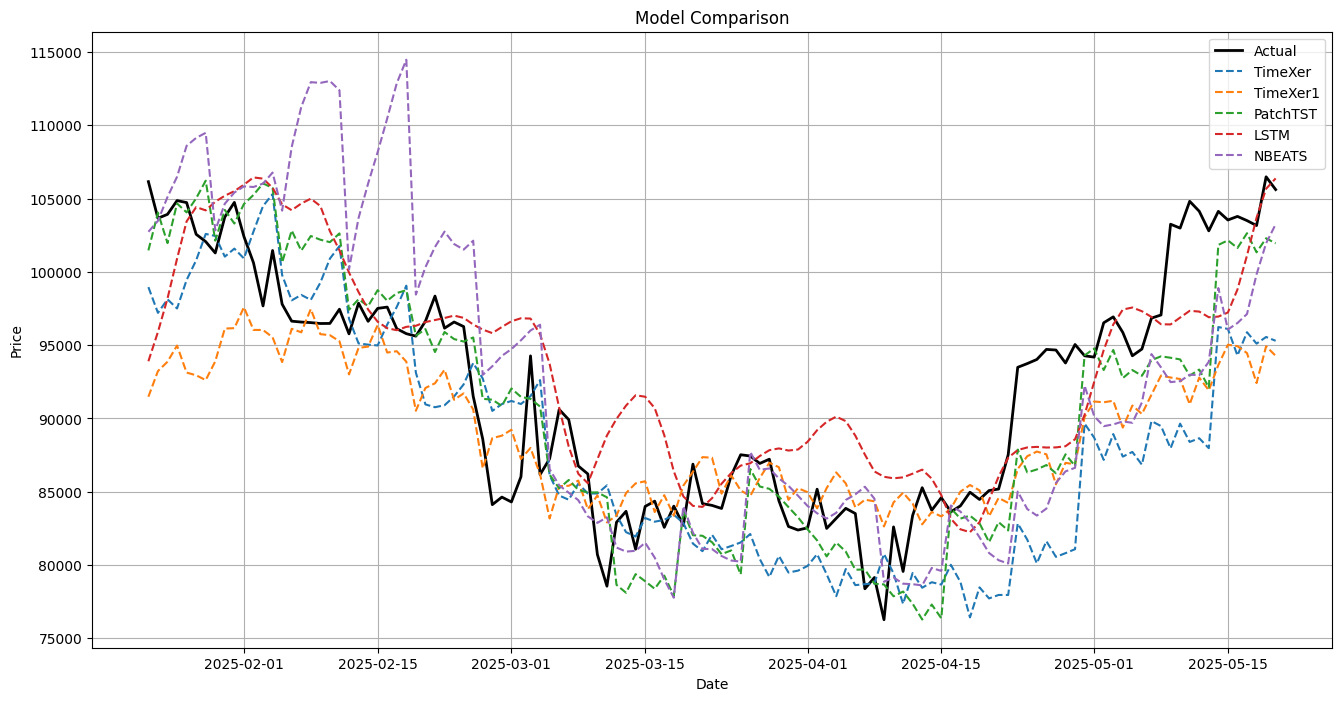

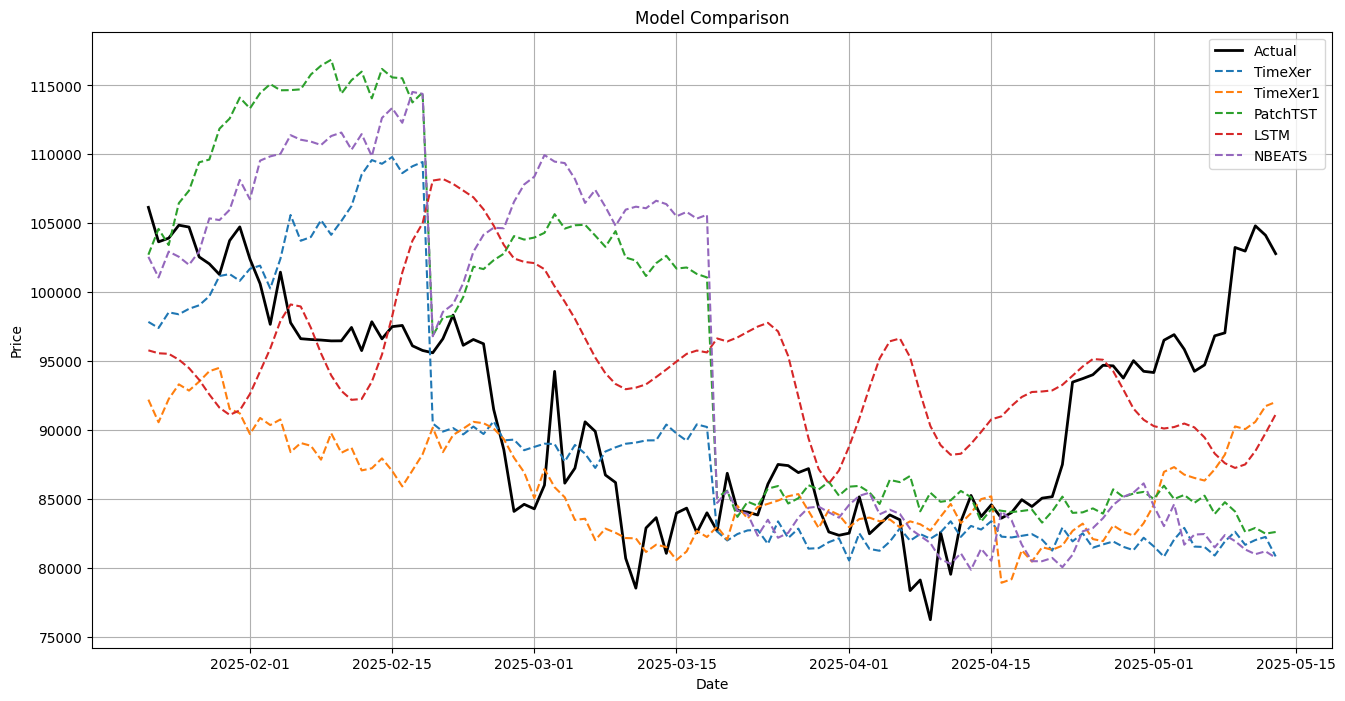

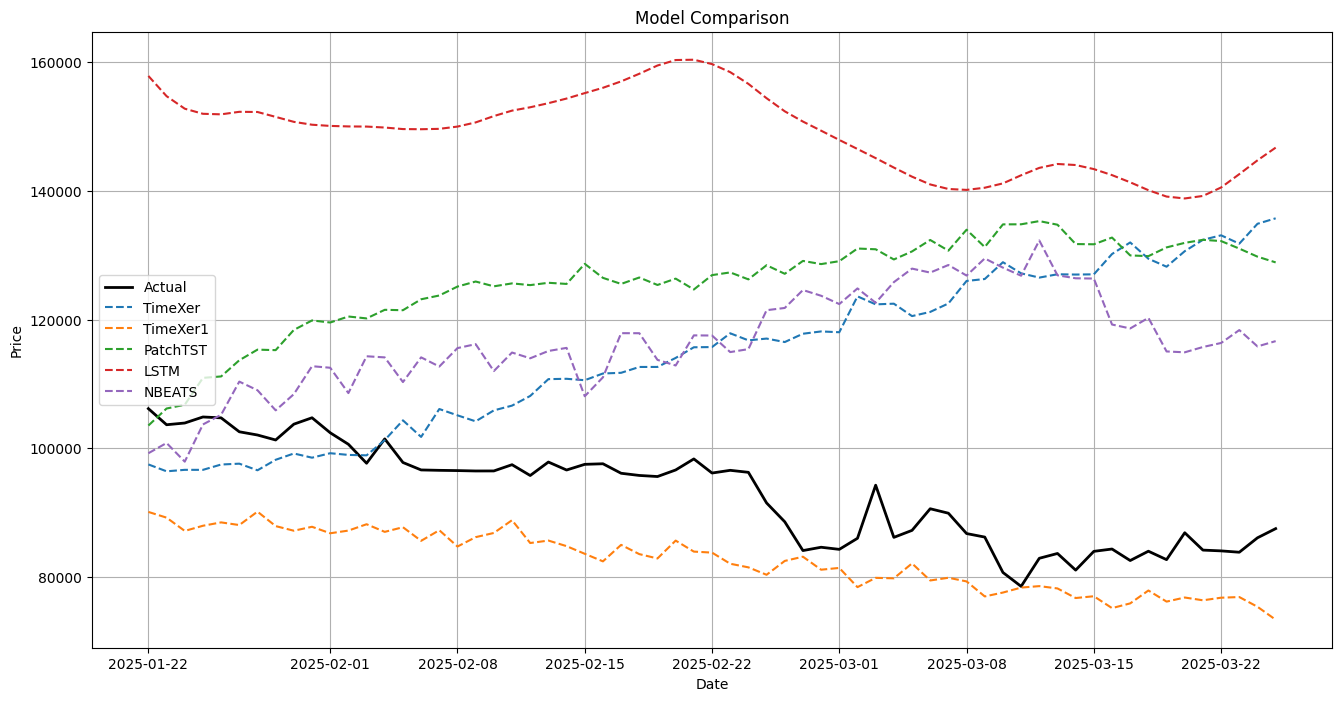

At a 70-day forecast horizon, the proposed TimeXer-Exog model achieves a Mean Squared

Error (MSE) of 10.814, scaled by 107, which outperformed the univariate TimeXer baseline

by over 89%. The results show that explicitly conditioning deep learning models on Global

Liquidity as an exogenous variable gives substantial improvements in long-horizon Bitcoin price

forecasting.

Keywords: Bitcoin forecasting, Global liquidity, TimeXer, Transformers, Deep learning, Macroe-

conomic conditioning, Long-horizon forecasting

1

Introduction

Early attempts to forecast Bitcoin prices were made using statistical tools, especially the ARIMA

models (Sagheer et al., 2025; Xu, 2025). ARIMA is good at picking up short-term linear patterns,

like the ones in a relatively calm equity index over a few weeks. However, bitcoin does not behave

like that. Its price is noisy and very volatile, which statistical models and tools do not capture.

ARIMA requires stationarity and linear structure, which is exactly what bitcoin lacks. Large rallies,

sudden crashes, or regime shifts often get smoothed away (Pratas et al., 2023; Mizdrakovic, 2024).

∗Corresponding author. Email: sravankt.cs20@rvce.edu.in

1

arXiv:2512.22326v2 [cs.LG] 11 Jan 2026

As a result, these models can perform well over a short horizon, their accuracy drops once the

forecast horizon is about 60 or 90 days (Mousa, 2025; Kareem and Aue, 2025).

Researchers moved to RNN models, which were designed to handle sequences. Long Short-Term

Memory (LSTM) and Gated Recurrent Unit (GRU) models were successful in learning the non-

linear patterns from the data (Bagheri and Giudici, 2025; Xu, 2025). They can, for example, react

differently to a slow upward trend than to a sudden spike triggered by a regulatory headline. These

models are not perfect. Because they process data step by step, they scale poorly and struggle

when dependencies stretch far back in time. Capturing relationships across hundreds of days still

remains hard, and unreliable (Zhao et al., 2022; Zheng, 2025).

More recently, attention has shifted toward Transformer-based models, time series forecasting

moved to self-attention rather than strict sequence processing (Nie, 2022; Zhao et al., 2022). Instead

of remembering the past one step at a time, these models can look across an entire window at once.

PatchTST takes this idea further by breaking the time series into patches, small segments that

preserve local structure while keeping computation manageable (Nie, 2022). For time series fore-

casting which require long look-back windows, Transformer models have repeatedly outperformed

LSTM-based approaches, especially for long-horizon predictions (Nie, 2022; Zheng, 2025).

Long-term forecasting improves when models are allowed to look beyond price history itself.

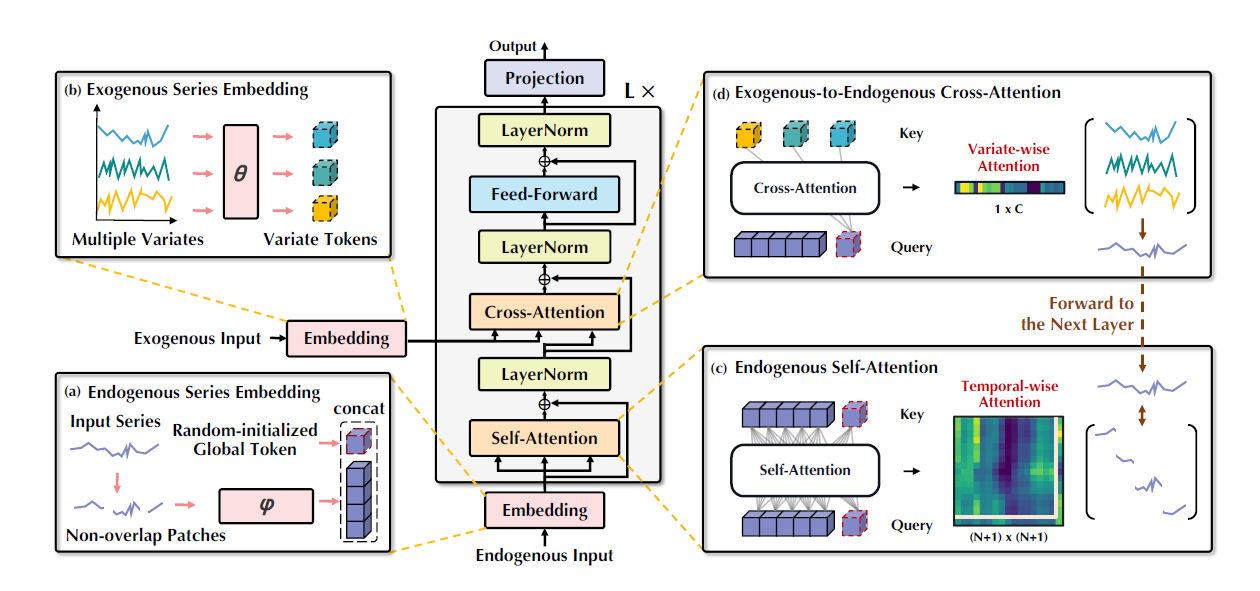

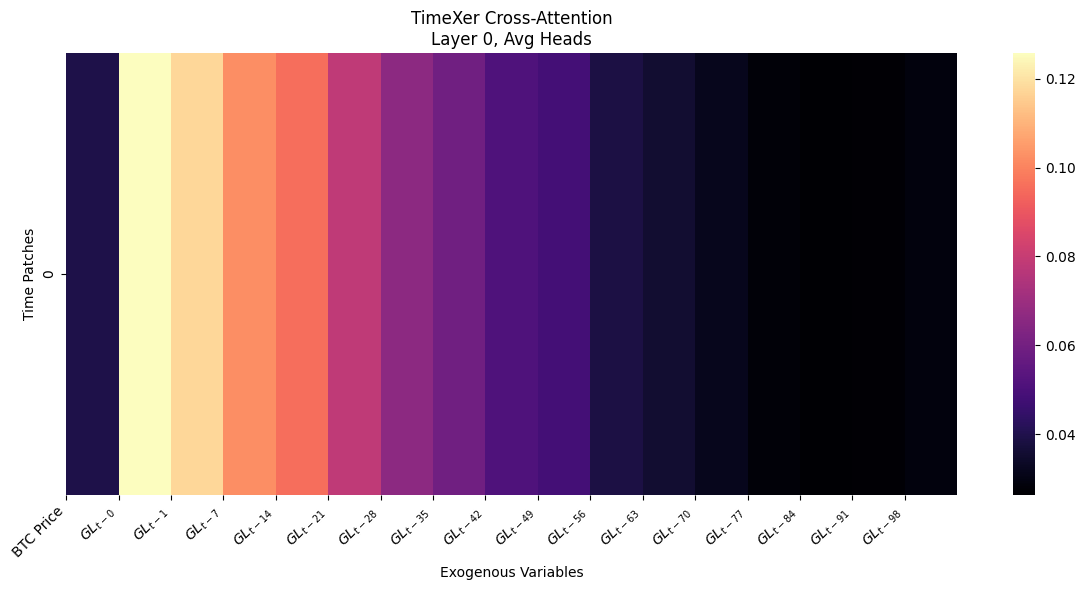

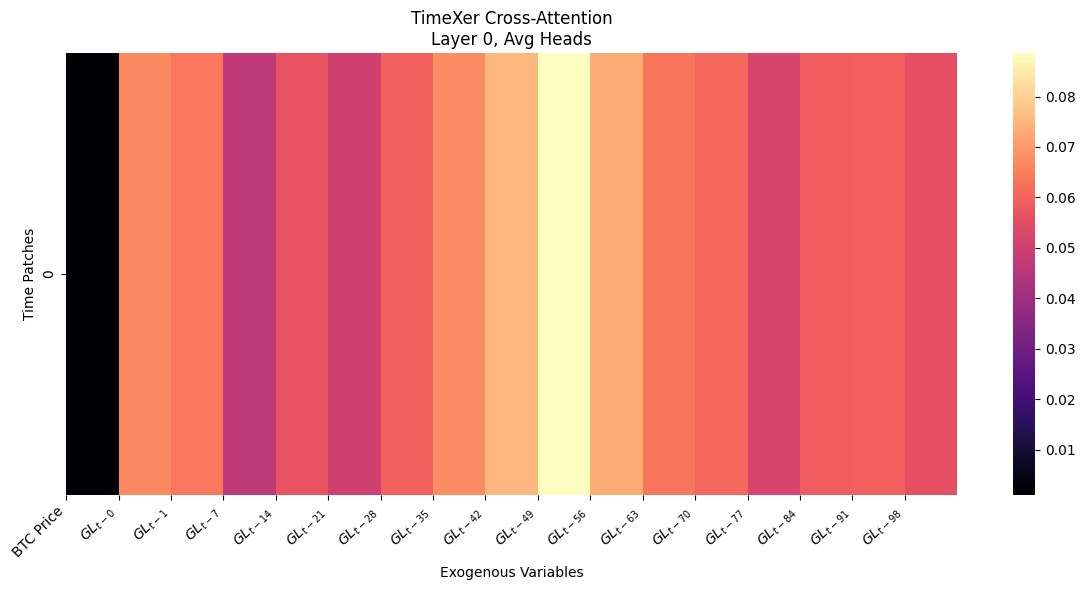

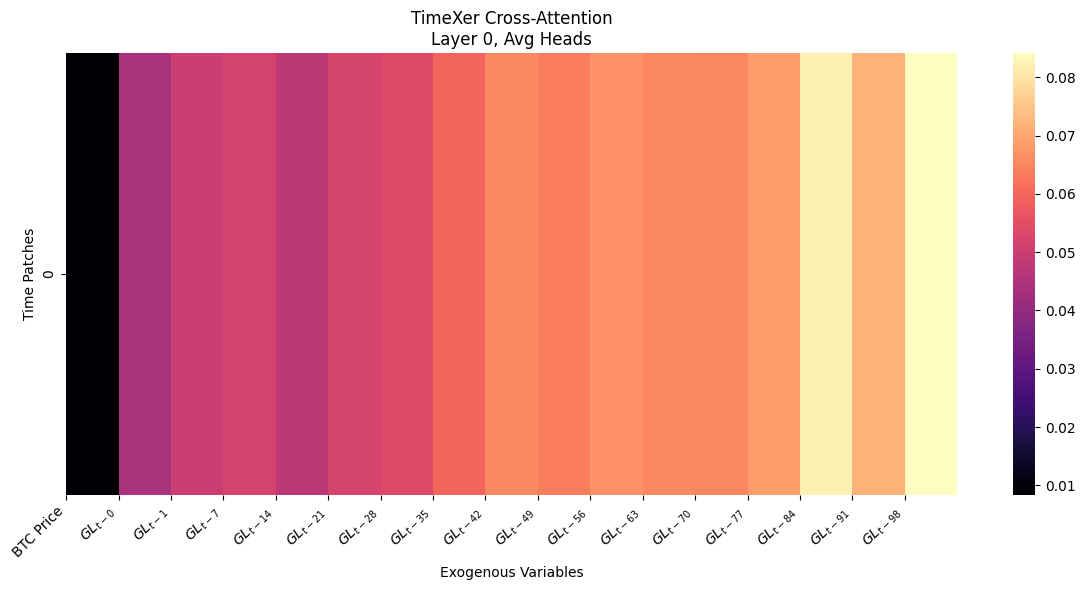

The TimeXer framework reflects this shift. It combines patch-wise attention for the main series with

cross-attention for external variables, making it possible to integrate data that arrive at different

frequencies and are not neatly aligned in time (Wang, 2024). This is closer to how real financial

systems operate. Macroeconomic indicators do not update on a daily basis, yet markets tend to

respond to them gradually and unevenly.

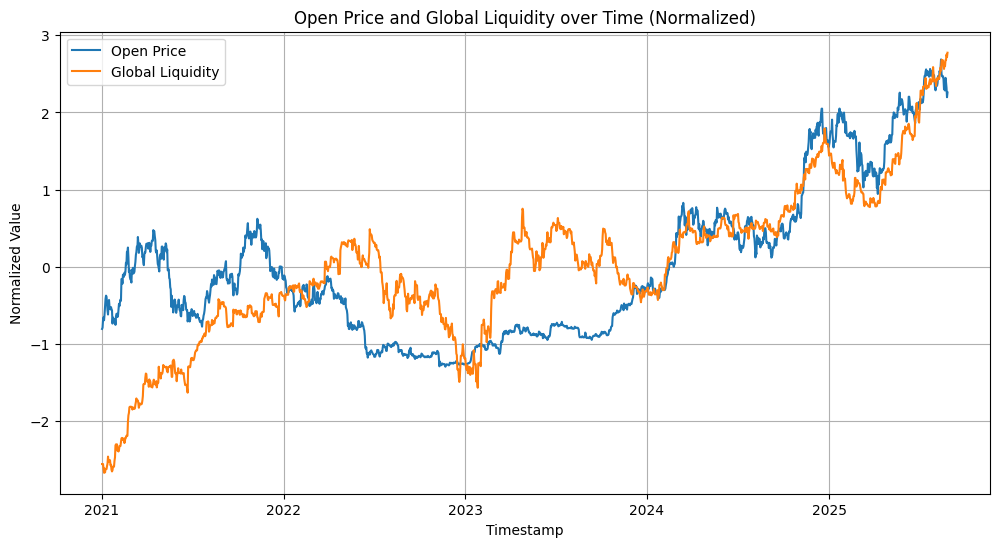

Global liquidity is often measured by M2 money supply, which has particularly attracted atten-

tion (Gu and Chen, 2025). Although the relationship is not perfectly stable, the logic is intuitive.

According to empirical work using time-varying Granger causality, the influence of M2 on Bitcoin

prices is not constant. It strengthens during expansionary regimes and weakens in other regimes

(Gu and Chen, 2025). Co-integration analyses go further by pointing towards a long-run equi-

librium relationship in which Bitcoin prices respond more than proportionally to liquidity growth

(Kokabian, 2025). It is important to note that these effects do not come into the pi