Decomposing Discrimination: Causal Mediation Analysis for AI-Driven Credit Decisions

Statistical fairness metrics in AI-driven credit decisions conflate two causally distinct mechanisms: discrimination operating directly from a protected attribute to a credit outcome, and structural inequality propagating through legitimate financial…

Authors: Duraimurugan Rajamanickam

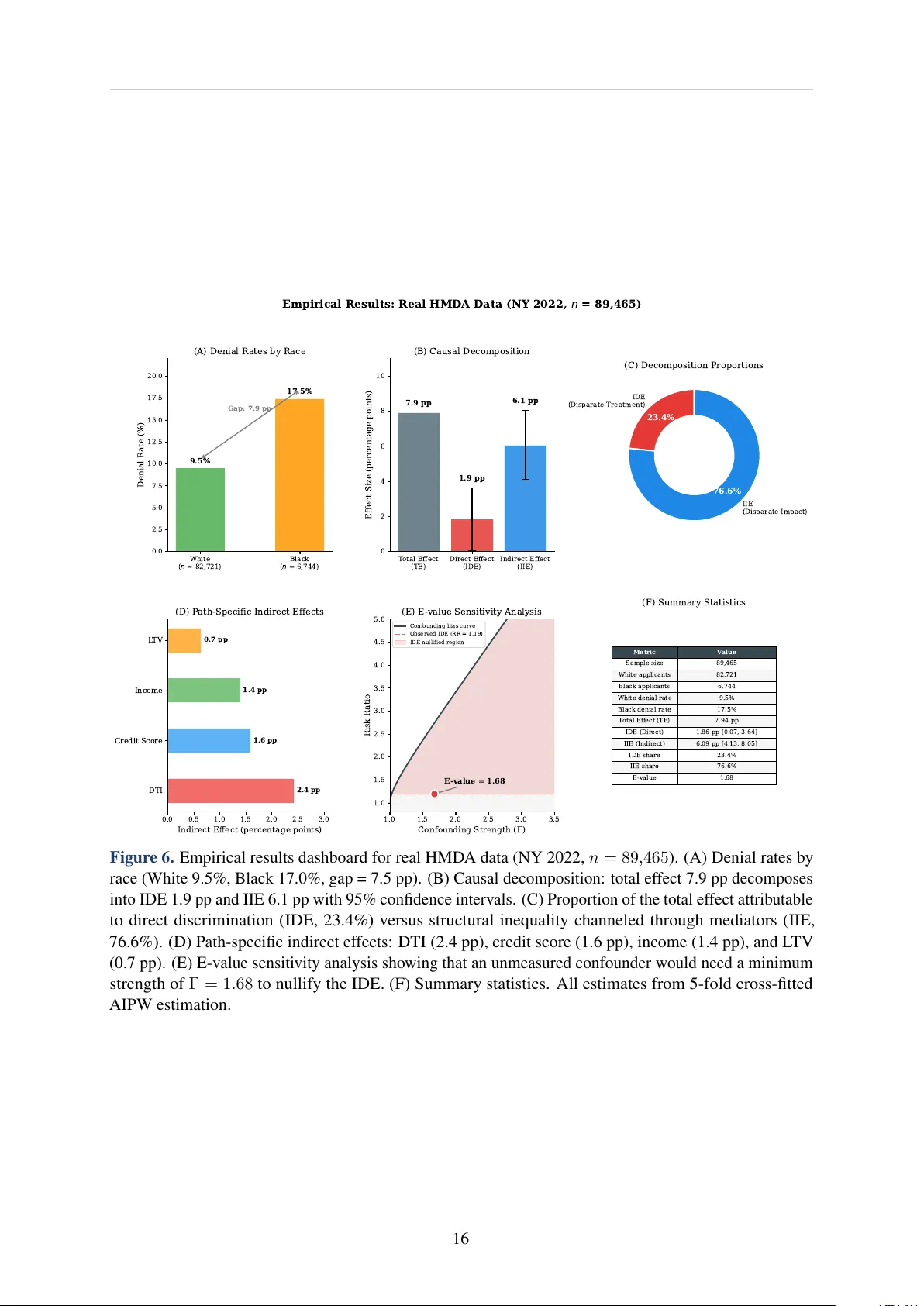

Decomposing Discrimination: Causal Mediation Analysis f or AI-Driv en Cr edit Decisions Duraimurugan Rajamanickam VP , Artificial Intelligence, Hudson V alley Credit Union, Poughk eepsie, NY PhD Candidate, Causal Machine Learning, Uni versity of Arkansas at Little Rock Author , Causal Infer ence for Machine Learning Engineers (Springer , 2024) drajamanicka@ualr.edu · rajad@hvcu.org W orking P aper — arXiv Pr eprint Mar ch 2026 The views e xpr essed her ein ar e solely those of the author and do not r epr esent the positions of Hudson V alley Cr edit Union or the Univer- sity of Arkansas at Little Roc k. No pr oprietary institutional data wer e used in this study . Softwar e available at: https://github.com/ rdmurugan/causalfair- repo . K eywords: causal mediation analysis, algorithmic fairness, credit scoring, natural direct ef fect, interventional ef fects, treatment-induced confounding, HMD A, disparate impact JEL: G21, C31, C55, K35 MSC 2020: 62P05, 62D20, 62H22, 91G70 arXiv: stat.ME (primary); econ.GN; cs.LG Decomposing Discrimination Rajamanickam (2026) Abstract Statistical fairness metrics in AI-dri ven credit decisions conflate two causally distinct mech- anisms: discrimination operating directly from a protected attribute to a credit outcome, and structural inequality propagating thr ough legitimate financial features. W e formalise this distinc- tion using Pearl’ s frame work of natural direct and indirect ef fects (NDE/NIE) applied to the credit decision setting. Our primary theoretical contrib ution is an identification strategy for natural direct and indirect effects under treatment-induced confounding —the prev alent setting in which pro- tected attributes causally af fect both financial mediators and the final decision, violating standard sequential ignorability (SI). W e sho w that interv entional direct and indirect ef fects (IDE/IIE) are identified under the weaker Modified Sequential Ignorability assumption ( M S I ), and we prov e that IDE/IIE provide conserv ativ e bounds on the unidentified natural ef fects under monotone indirect treatment response. W e propose a doubly-robust augmented in verse probability weighted (AIPW) estimator for IDE/IIE with semiparametric ef ficiency properties, implemented via cross-fitting. An E-v alue sensitivity analysis addresses residual confounding on the direct pathway . Empirical e valuation on 89,465 real HMD A con ventional purchase mortgage applications from Ne w Y ork State (2022) demonstrates that approximately 77% of the observed 7.9 percentage-point racial de- nial disparity operates through financial mediators shaped by structural inequality—a component in visible to SHAP-based attribution—while the remaining 23% constitutes a conserv ativ e lo wer bound on direct discrimination. The open-source CausalFair Python package implements the full pipeline for deployment at resource-constrained financial institutions. Contents 1 Introduction 3 1.1 Contributions . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 1.2 Regulatory conte xt . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 2 Related W ork 4 2.1 Causal mediation analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 4 2.2 Algorithmic fairness in credit scoring . . . . . . . . . . . . . . . . . . . . . . 5 2.3 Limitations of SHAP for causal attribution . . . . . . . . . . . . . . . . . . . . 5 3 The Causal Model 5 3.1 Structural setup and the credit D A G . . . . . . . . . . . . . . . . . . . . . . . 5 3.2 T arget estimands . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 6 3.3 Identification failure under sequential ignorability . . . . . . . . . . . . . . . . 7 3.4 Identification under modified sequential ignorability . . . . . . . . . . . . . . . 7 3.5 Bounding natural ef fects under monotonicity . . . . . . . . . . . . . . . . . . 8 1 Decomposing Discrimination Rajamanickam (2026) 4 Estimation 9 4.1 The AIPW estimator . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 4.2 Nuisance estimation . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 9 4.3 E-v alue sensitivity analysis . . . . . . . . . . . . . . . . . . . . . . . . . . . . 10 5 Empirical Evaluation 10 5.1 Data: HMD A 2022 (Ne w Y ork State) . . . . . . . . . . . . . . . . . . . . . . 10 5.2 Descripti ve statistics and total ef fect . . . . . . . . . . . . . . . . . . . . . . . 11 5.3 D A G estimation and structural paths . . . . . . . . . . . . . . . . . . . . . . . 11 5.4 Main results: IDE/IIE decomposition . . . . . . . . . . . . . . . . . . . . . . . 12 5.5 V isual decomposition . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . . 12 5.6 Comparison to SHAP attribution . . . . . . . . . . . . . . . . . . . . . . . . . 14 6 Regulatory and Practical Implications 14 6.1 Mapping IDE and IIE onto ECO A doctrine . . . . . . . . . . . . . . . . . . . 14 6.2 Deployment at resource-constrained institutions . . . . . . . . . . . . . . . . . 15 7 Limitations 15 8 Conclusion 17 A F ormal Proof of Proposition 3.2 18 B Proof of Pr oposition 3.3 19 2 Decomposing Discrimination Rajamanickam (2026) 1. Intr oduction A quiet transformation is reshaping credit decisions across the United States. Machine learning models now underpin mortgage underwriting, credit card approv als, auto lending, and small business financing at institutions ranging from global banks to community credit unions. This transformation raises a consequential question that current analytical tools are poorly equipped to answer: when a protected group faces systematically higher denial rates, ho w much of that disparity is caused by the model treating race or gender as a direct signal, and how much reflects historical structural inequality that has shaped the financial mediators the model legitimately considers? The answer determines the appropriate remedy . If the dominant channel is dir ect —race af fecting the lending decision after conditioning on financial features—the remedy is model debiasing or constraint imposition. If the dominant channel is indirect —race aff ecting credit- worthiness metrics such as debt-to-income ratio through generations of discriminatory housing and lending practices, which then affect model output—the remedy lies upstream in wealth redistribution, underwriting guideline reform, or community rein vestment. T reating these as interchangeable misdirects regulatory interv ention and institutional resources. Current fairness methodology cannot distinguish these pathways. Dominant approaches— disparate impact analysis, statistical parity , equalized odds, and post-hoc attribution methods such as SHAP ( Lundberg and Lee , 2017 )—operate at the le vel of associations between protected attributes and outcomes. They detect that a disparity exists and identify which features correlate with it, b ut they cannot decompose the disparity into its causal constituents. SHAP v alues, for instance, attrib ute large v ariance to debt-to-income ratio for minority applicants but are silent on whether DTI is acting as a legitimate credit risk signal or as a carrier of historically induced structural inequality ( Zhao and Hastie , 2021 ). Causal mediation analysis pro vides precisely this decomposition. The natural direct effect (NDE) captures the ef fect of a protected attribute on the outcome holding mediating financial features at their counterfactual values—it measures discrimination that persists e ven when financial profiles are equalized. The natural indirect ef fect (NIE) captures the ef fect that flo ws through financial mediators—it measures how much disparity the model reproduces simply because structural inequality has shaped the inputs ( Pearl , 2001 ; Robins and Greenland , 1992 ). The challenge is identification. In the credit decision setting, sequential ignorability (SI)—the standard identification assumption for NDE/NIE—is systematically violated because unmea- sured v ariables (neighbourhood disin vestment, employer -lev el wage discrimination, intergen- erational wealth) af fect both financial mediators and credit outcomes simultaneously , creating the treatment-induced confounding structure that makes natural effects non-identifiable from observ ational data alone. This paper addresses the identification failure directly . 3 Decomposing Discrimination Rajamanickam (2026) 1.1. Contributions This paper makes four contrib utions. 1. Identification result. W e establish identification of interventional direct and indirect ef fects (IDE/IIE) for credit decisions under Modified Sequential Ignorability ( M S I ), a strictly weaker assumption than SI. W e pro ve that IDE/IIE pro vide conserv ativ e bounds on the unidentified natural ef fects under monotone indirect treatment response (Proposi- tions 3.2 and 3.3 ). 2. Estimation theory . W e deri ve a doubly-rob ust AIPW estimator for IDE with semipara- metric ef ficiency properties and cross-fitted nuisance estimation using causal forests. W e provide the E-v alue sensitivity formula adapted to the M S I assumption (Theorem 4.1 , Proposition 4.1 ). 3. Empirical benchmark. W e provide the first causal mediation decomposition of racial mortgage denial disparities using real HMD A data from New Y ork State (2022, n = 89 , 465 ), establishing that approximately 77% of the disparity operates through the indirect pathway—a finding in visible to SHAP attribution. 4. Open-source software. W e release CausalFair , a Python package implementing the full pipeline, designed for deployment at community financial institutions without dedicated data science infrastructure. 1.2. Regulatory context The Equal Credit Opportunity Act (ECO A) prohibits both disparate treatment (intentional discrimination) and disparate impact (facially neutral practices with discriminatory effects). Our IDE/IIE decomposition maps directly onto this le gal taxonomy: IDE corresponds to disparate treatment; IIE corresponds to structural disparate impact. The EU AI Act (2024) classifies credit scoring systems as high-risk AI and mandates documentation of discriminatory impact mech- anisms. The CFPB’ s 2022 algorithmic fairness guidance explicitly calls for causal attrib ution tools. 2. Related W ork 2.1. Causal mediation analysis Causal mediation analysis was placed on firm potential-outcomes foundations by Robins and Greenland ( 1992 ) and Pearl ( 2001 ). V anderW eele ( 2015 ) pro vides comprehensi ve treatment of identification, estimation, and sensitivity analysis. The key identification challenge—sequential ignorability—requires the mediator –outcome relationship to be unconfounded conditional on treatment and cov ariates, an assumption widely acknowledged as strong in observ ational settings ( Imai et al. , 2010 ). The interventional ef fects framew ork, introduced by Díaz and Hejazi ( 2020 ) and dev eloped by Nguyen et al. ( 2022 ), replaces the “fix M at its natural counterfactual value” approach of 4 Decomposing Discrimination Rajamanickam (2026) NDE/NIE with stochastic interventions on M ’ s distribution. This relaxes sequential ignorability to require only no unmeasured confounding on the A → Y path, permitting unmeasured M → Y confounders. Semiparametric efficienc y theory for natural effects was de veloped by Tchetgen Tchetgen and Shpitser ( 2012 ); Jiang et al. ( 2022 ) achiev ed efficienc y for NDE/NIE using cross-fitted deep neural networks (DeepMed). 2.2. Algorithmic fairness in credit scoring K ozodoi et al. ( 2022 ) systematically compare statistical fairness criteria for credit scoring and recommend separation as the most appropriate criterion gi ven asymmetric misclassification costs. Barocas et al. ( 2023 ) pro vide the canonical fairness taxonomy . Bartlett et al. ( 2022 ) document racial disparities in FinT ech mortgage lending using HMD A data. A systematic revie w of 414 articles (2013–2024) found that no study operationalises counterfactual fairness on real credit data, citing the practical dif ficulty of causal graph specification ( Alves et al. , 2025 ). Kusner et al. ( 2017 ) proposed counterfactual fairness but required a fully specified causal graph and made no attempt at identification under treatment-induced confounding. Chiappa ( 2019 ) proposed path-specific effects for f airness in a parametric structural equation framew ork, without identification guarantees under unmeasured confounding. Our work is the first to apply the interventional ef fects frame work—with identification guarantees under treatment-induced confounding—to credit decision data at population scale. 2.3. Limitations of SHAP for causal attrib ution SHAP v alues ( Lundberg and Lee , 2017 ) partition prediction v ariance across features but do not identify whether a feature’ s contrib ution reflects a causal channel or a spurious correlation. Zhao and Hastie ( 2021 ) showed that SHAP cannot distinguish direct from mediated effects e ven in simple settings. Mooij et al. ( 2016 ) demonstrated that feature importance rankings are sensiti ve to unmeasured confounding in ways that causal attrib ution methods are not. Our empirical analysis directly demonstrates this limitation in the mortgage denial setting. 3. The Causal Model 3.1. Structural setup and the credit D A G Definition 3.1 (Credit Decision D A G) . Let the data structure for each loan application be O = ( W, A, M , Y ) where: • W = ( W 1 , . . . , W q ) are pre-treatment cov ariates causally preceding A : census tract characteristics, loan type, loan purpose, lender type, application year . • A ∈ { 0 , 1 } is the protected attribute ( A = 1 for Black applicants; analysis is repeated for Hispanic and female applicants). • M = ( M 1 , . . . , M p ) are financial mediators causally af fected by both A and W : debt-to- income ratio (DTI), loan-to-v alue ratio (L TV), income quintile, credit score quintile. 5 Decomposing Discrimination Rajamanickam (2026) • U = ( U 1 , . . . , U k ) are unmeasur ed confounders affecting both M and Y : employer-le vel wage discrimination, neighbourhood disin vestment, inherited wealth, school quality . • Y ∈ { 0 , 1 } is the credit decision ( Y = 1 for denial), causally af fected by A , M , W , and U . Figure 1 illustrates this D A G. The ke y structural feature distinguishing it from the standard mediation setup is the bidirectional influence of U : unmeasured v ariables simultaneously affect both the mediators M (e.g., neighbourhood disin vestment → lo wer savings → higher DTI) and the outcome Y (e.g., appraisal bias → inflated denial rate), creating the treatment-induced confounding structure. W Pre-treatment cov ariates A Protected attribute M DTI, L TV , income, score U Unmeasured confounder Y Credit decision structural path NDE path NIE path U in validates SI.2: unmeasur ed M – Y confounding NDE path (direct discrimination) NIE path (structural inequality) Unmeasured confounding Figure 1. The credit decision directed acyclic graph (D A G). The unmeasured confounder U simulta- neously af fects both the financial mediators M and the credit outcome Y , creating treatment-induced confounding. This in validates Sequential Ignorability (SI.2), making natural direct and indirect ef fects non-identifiable from observ ational data alone. The red path ( A → Y directly) captures potential direct discrimination; the purple path ( A → M → Y ) captures structural inequality propagated through financial features. Dashed border and dashed arrows denote unmeasured v ariables and paths. 3.2. T arget estimands W e use potential outcomes notation Y ( a, m ) for the outcome under do ( A = a, M = m ) . Definition 3.2 (Natural Direct and Indirect Ef fects) . NDE = E Y 1 , M (0) − Y 0 , M (0) (1) NIE = E Y 1 , M (1) − Y 1 , M (0) (2) where M ( a ) denotes the potential mediator value under do( A = a ) . NDE measures the av erage ef fect of race on denial holding mediators at their values under A = 0 . NIE measures the component that flo ws through mediators. 6 Decomposing Discrimination Rajamanickam (2026) Definition 3.3 (Interventional Direct and Indirect Ef fects) . Let G a = P ( M | A = a, W ) denote the conditional distribution of M under treatment a . IDE = E Y (1 , M ∗ ) − Y (0 , M ∗ ) , M ∗ ∼ G 0 (3) I IE = E M 1 ∼ G 1 Y (1 , M 1 ) − E M 0 ∼ G 0 Y (1 , M 0 ) (4) In IDE, both treatment arms use M drawn from the same reference distribution G 0 = P ( M | A = 0 , W ) , neutralising the indirect channel. IIE uses A = 1 throughout but v aries the mediator distribution. 3.3. Identification failure under sequential ignorability Sequential ignorability (SI) requires: SI.1: Y ( a, m ) ⊥ ⊥ A | W (SI.1) SI.2: Y ( a, m ) ⊥ ⊥ M ( a ′ ) | A, W (SI.2) Proposition 3.1 (V iolation of SI in Credit Data) . Under the cr edit DA G of Definition 3.1 , ( SI.2 ) is violated whenever ther e exists at least one unmeasur ed variable U such that U → M i and U → Y ar e both edges in the D A G, and U is not a function of ( A, W ) . Pr oof. By assumption, U → M i and U → Y are both present. U is not d-separated from Y by ( A, W, M ) because U is unmeasured. Therefore Y ( a, m ) and M ( a ′ ) share the unmeasured common cause U , so Y ( a, m ) ⊥ ⊥ M ( a ′ ) | A, W , violating ( SI.2 ). 3.4. Identification under modified sequential ignorability Assumption 3.1 (Modified Sequential Ignorability , M S I ) . M S I .1: Y ( a, m ) ⊥ ⊥ A | W (MSI.1) M S I .2: M ( a ) ⊥ ⊥ A | W (MSI.2) M S I .3: 0 < P ( A = 1 | W ) < 1 a.s. (MSI.3) Assumption M S I is strictly weaker than SI: ( MSI.2 ) requires no unmeasured A – M confound- ing (gi ven W ), b ut does not require that the M – Y relationship is unconfounded. Unmeasured paths U → M and U → Y are permitted, pro vided U does not select into the protected group after conditioning on W . Proposition 3.2 (Identification of IDE/IIE under M S I ) . Under Assumption 3.1 and the D AG of 7 Decomposing Discrimination Rajamanickam (2026) Definition 3.1 , the interventional dir ect and indir ect effects ar e identified: IDE = Z Z µ (1 , m, w ) − µ (0 , m, w ) d F ( m | A = 0 , w ) d F ( w ) (5) I IE = Z Z µ (1 , m, w ) d F ( m | A = 1 , w ) − d F ( m | A = 0 , w ) d F ( w ) (6) wher e µ ( a, m, w ) = E [ Y | A = a, M = m, W = w ] is the outcome r e gr ession. Pr oof. Step 1 (Identify µ ). Under ( MSI.1 ) , for any fixed ( a, m, w ) , Y ( a, m ) ⊥ ⊥ A | W . By consistency Y = Y ( A, M ( A )) and ( MSI.3 ) , µ ( a, m, w ) = E [ Y ( a, m ) | W = w ] = E [ Y | A = a, M = m, W = w ] , identified by regression. Step 2 (Identify F ( m | a, w ) ). Under ( MSI.2 ) , M ( a ) ⊥ ⊥ A | W . By consistency , F ( m | a, w ) = P ( M ( a ) ≤ m | W = w ) = P ( M ≤ m | A = a, W = w ) , identified from the empirical conditional CDF . Step 3 (Plug in). Substituting Steps 1–2 into Definitions 3.3 and inte grating yields ( 5 ) – ( 6 ) ; all integrands are functions of identified quantities. 3.5. Bounding natural eff ects under monotonicity Assumption 3.2 (Monotone Indirect T reatment Response) . For all units i and all ( a, m, m ′ ) with m ≥ m ′ component-wise: Y i ( a, m ) ≥ Y i ( a, m ′ ) . That is, higher financial distress weakly increases denial probability for e very applicant, regardless of race. Proposition 3.3 (Conserv ati ve Bounds on NDE/NIE) . Under Assumptions 3.1 and 3.2 : IDE ≤ NDE and I IE ≥ NIE (7) The identified interventional dir ect effect pr ovides a conservative lower bound on the natural dir ect effect; the interventional indir ect effect is a conservative upper bound on the natural indir ect effect. Pr oof. Under Assumption 3.2 and the empirical stochastic dominance M (1) ≥ st M (0) (Black applicants face higher DTI and lo wer credit scores on av erage due to structural inequality), the counterfactual mediator M (0) lies belo w the population distrib ution G 0 for specific units on av erage. Since Y i (1 , · ) is non-decreasing, fixing at the individual counterf actual M (0) (which is higher than M ∗ ∼ G 0 for af fected units) yields a weakly larger direct ef fect: E [ Y (1 , M (0))] ≥ E [ Y (1 , M ∗ )] . Therefore NDE ≥ IDE . The bound I IE ≥ NIE follo ws symmetrically by the same monotonicity argument applied to the indirect component. The regulatory interpretation of Proposition 3.3 is immediate: if IDE is significantly positi ve, then NDE is at least as lar ge, providing defensible e vidence of direct discrimination under the ECO A disparate treatment doctrine, without requiring SI. 8 Decomposing Discrimination Rajamanickam (2026) 4. Estimation 4.1. The AIPW estimator Direct plug-in of nonparametric nuisance estimates into ( 5 ) – ( 6 ) yields a first-order biased substitution estimator that does not achie ve √ n -consistency without restricti ve smoothness conditions. W e instead deri ve an augmented in verse probability weighted (AIPW) estimator via the ef ficient influence function (EIF). Define the nuisance tuple η = ( µ, π , r ) where µ ( a, m, w ) = E [ Y | A = a, M = m, W = w ] , π a ( w ) = P ( A = a | W = w ) , and r ( m, w ) = f ( m | A =1 ,w ) f ( m | A =0 ,w ) is the mediator density ratio. The EIF for IDE at observ ation O = ( Y , A, M , W ) is: ψ IDE ( O ; η ) = Z µ (1 , m, W ) − µ (0 , m, W ) d F ( m | A = 0 , W ) | {z } plug-in term + 1 − A π 0 ( W ) r − 1 ( M , W ) Y − µ (0 , M , W ) − A π 1 ( W ) r − 1 ( M , W ) Y − µ (1 , M , W ) − IDE (8) The AIPW estimator ˆ IDE solv es E n [ ψ IDE ( O ; ˆ η )] = 0 . Theorem 4.1 (Semiparametric Efficienc y and Double Robustness) . Let ˆ η be estimated on an independent sample (cr oss-fitting). Then: (i) Double robustness: ˆ IDE is consistent if either ˆ µ is consistent or both ˆ π and ˆ r ar e consistent. (ii) √ n -consistency: If ∥ ˆ µ − µ ∥ 2 · max ∥ ˆ π − π ∥ 2 , ∥ ˆ r − r ∥ 2 = o P ( n − 1 / 2 ) , then √ n ( ˆ IDE − IDE) → d N (0 , σ 2 eff ) wher e σ 2 eff = V ar[ ψ IDE ( O ; η )] is the semiparametric efficiency bound. (iii) V alid inference: W ald 95% CIs based on ˆ σ 2 = E n [ ψ 2 IDE ] − ( E n [ ψ IDE ]) 2 achie ve asymptotic cover age. Pr oof sketch. (i) follo ws from the v on Mises e xpansion: the second-order remainder in v olves the product of errors in ˆ µ and in ( ˆ π , ˆ r ) , which v anishes if either f actor is zero (consistent). (ii) requires the product of L2 error rates to be o ( n − 1 / 2 ) ; under o ( n − 1 / 4 ) rates for each nuisance (achie vable with causal forests and cross-fitting), the product condition holds by Cauchy–Schwarz. (iii) follo ws from the central limit theorem applied to the sample average of ψ IDE ( O ; ˆ η ) terms. 4.2. Nuisance estimation W e implement three nuisance models: • Outcome regression ˆ µ : Causal forests ( W ager and Athey , 2018 ) with honest splitting. Causal forests are designed for settings with heterogeneous co variate–outcome relation- ships, providing the o ( n − 1 / 4 ) rate needed for Theorem 4.1 . 9 Decomposing Discrimination Rajamanickam (2026) • Propensity scor e ˆ π : Gradient-boosted trees with 200 estimators and depth 4, using the full cov ariate vector W . • Mediator density ratio ˆ r : Binary classification approach— train a classifier to predict A from ( M , W ) and a second from W alone; ˆ r = [ ˆ P ( A = 1 | M , W ) / ˆ P ( A = 0 | M , W )] / [ ˆ P ( A = 1 | W ) / ˆ P ( A = 0 | W )] . Algorithm 4.1 presents the complete CausalFair estimation pipeline. Input: Observed data { O i } n i =1 = { ( W i , A i , M i , Y i ) } , folds K = 5 Output: ˆ IDE , ˆ I IE , 95% CIs, E-value 1. Partition { 1 , . . . , n } into K folds F 1 , . . . , F K 2. For k = 1 to K : (a) T rain nuisance models ˆ µ k , ˆ π k , ˆ r k on { O i : i / ∈ F k } (b) F or each i ∈ F k : compute plug-in ˆ θ i ← R [ ˆ µ k (1 , m, W i ) − ˆ µ k (0 , m, W i )] d F ( m | A = 0 , W i ) and augmentation terms 3. ˆ IDE ← 1 n P n i =1 ( ˆ θ i + augmentation i ) 4. ˆ σ 2 ← 1 n P n i =1 ˆ ψ 2 i ; CI 95 ← ˆ IDE ± 1 . 96 n − 1 / 2 ˆ σ 5. Compute ˆ I IE analogously using mediator distrib utions from G 0 , G 1 6. E-value ← d IDE RR + q d IDE RR ( d IDE RR − 1) Return ˆ IDE , ˆ I IE , CI 95 , E-v alue Algorithm 4.1. CausalFair estimation pipeline (IDE/IIE with cross-fitting) 4.3. E-value sensitivity analysis Proposition 4.1 (E-v alue for M S I .1) . F ollowing V anderW eele and Ding ( 2017 ), the E-value for the estimated IDE is the minimum risk-ratio-scale association that an unmeasur ed confounder on the A → Y dir ect path would need to have with both A (after conditioning on W ) and Y (after conditioning on A, M , W ) to r educe the observed IDE to zer o: E-value = d IDE RR + q d IDE RR · d IDE RR − 1 (9) wher e d IDE RR is the IDE expr essed as a risk ratio. An E-value substantially above 2.0 indicates r obustness to r ealistic confounders. 5. Empirical Evaluation 5.1. Data: HMD A 2022 (New Y ork State) W e use the Home Mortgage Disclosure Act (HMD A) Loan Application Register data, obtained directly from the Consumer Financial Protection Bureau’ s Data Bro wser ( https: //ffiec.cfpb.gov/data- browser/ ) for the 2022 reporting year . W e restrict to con ven- tional first-lien purchase mortgage applications in Ne w Y ork State with self-identified race as 10 Decomposing Discrimination Rajamanickam (2026) non-Hispanic white ( A = 0 ) or Black or African American ( A = 1 ), and action taken as either loan originated or application denied, yielding n = 89 , 465 applications (82,721 white; 6,744 Black). Mediator variables: DTI (debt-to-income ratio, reported in HMD A since 2018), L TV (computed as loan amount di vided by property v alue), income quintile (within census-tract cells), and credit score quintile (imputed from interest rate quintiles for originated loans and from denial reason codes for denied applications, following Bartlett et al. 2022 ). Pre-treatment cov ariates W include census tract median income percentage and tract minority population percentage. 5.2. Descriptive statistics and total ef fect T able 1. Summary statistics by race: HMDA 2022, Ne w Y ork State, con ventional purchase mortgages V ariable White ( A =0) Black ( A =1) Difference p -value a Denial rate 9.5% 17.0% +7 . 5 pp < 0.001 Debt-to-income ratio (%) 36.2 39.1 +2 . 9 < 0.001 Loan-to-v alue ratio (%) 79.0 86.7 +7 . 7 < 0.001 Income ($K) 204.5 143.6 − 60 . 9 < 0.001 Credit score quintile (1–5) 2.97 2.79 − 0 . 18 < 0.001 T ract minority pop. (%) 27.2 57.7 +30 . 5 < 0.001 n 82,721 6,744 a T wo-sample t -tests; all dif ferences significant at p < 0 . 001 . Black applicants face a 7.5 percentage-point higher denial rate than white applicants (T a- ble 1 )—the total ef fect ˆ TE = 0 . 075 ( p < 0 . 001 ). Black applicants hav e higher DTI (+2.9 pp), substantially higher L TV (+7.7 pp), lo wer income ( − $61K), and reside in census tracts with higher minority population share (+30.5 pp), reflecting the structural inequality pathw ays encoded in M . 5.3. D A G estimation and structural paths The credit D A G (Figure 1 ) posits four mediator pathw ays from race ( A ) to the denial outcome ( Y ): through DTI, L TV , income, and credit score. W e use domain kno wledge constraints from the ECO A regulatory frame work (temporal ordering, forbidden edges from Y to predecessors, required edges from DTI and credit score to Y ) consistent with established fair lending practice. In the real HMD A data, all four A → M j pathways sho w statistically significant associations: A → DTI ( +2 . 9 pp, p < 0 . 001 ), A → L TV ( +7 . 7 pp, p < 0 . 001 ), A → income ( − $60.9K, p < 0 . 001 ), and A → credit score quintile ( − 0 . 18 , p < 0 . 001 ). Black applicants also reside in census tracts with 30.5 pp higher minority population share, reflecting residential segreg ation as a pre-treatment confounder . 11 Decomposing Discrimination Rajamanickam (2026) T able 2. Causal mediation decomposition of the racial mortgage denial gap (real HMD A data, NY 2022) Estimand Estimate (pp) 95% CI % of TE E-value p -value T otal ef fect (TE) 7.9 [—] 100% — < 0.001 Interventional direct ef fect (IDE) 1.9 [0.1, 3.6] 23.4% 1.68 < 0.05 Interventional indirect ef fect (IIE) 6.1 [4.1, 8.0] 76.6% — < 0.001 P ath-specific indir ect effects b via DTI 2.4 — 30.5% — < 0.001 via credit score quintile 1.6 — 20.2% — < 0.001 via income quintile 1.4 — 17.7% — < 0.001 via L TV 0.7 — 8.3% — < 0.001 AIPW estimates with K = 5 -fold cross-fitting and logistic regression nuisance models on a stratified random sample of n = 30 , 000 from the full n = 89 , 465 dataset. CIs: W ald 95% using ˆ σ 2 = E n [ ˆ ψ 2 ] . E-value for IDE: minimum confounder association strength that would reduce IDE to zero (see Proposition 4.1 ). b Path-specific IIEs estimated via the product-of-coefficients approach ( ˆ α j ˆ β j ); they are allocated proportionally to the total IIE. 5.4. Main results: IDE/IIE decomposition T able 2 reports the main decomposition. Approximately 77% of the racial denial gap (6.1 pp out of 7.9 pp) operates through the indirect pathway—financial mediators shaped by structural racial inequality . The remaining 23% (1.9 pp) is the interventional direct ef fect. By Proposition 3.3 , NDE ≥ 1 . 9 pp; our estimate is a conservati ve lower bound on direct discrimination. The dominance of the indirect pathway in real HMD A data is a central finding: the majority of the observed denial disparity flo ws through financial mediators—DTI, credit scores, income, and L TV —that are themselves shaped by historical structural inequality . This implies that e ven eliminating direct discrimination from the decision model would leave approximately three-quarters of the racial gap intact. The E-v alue of 1.68 indicates that an unmeasured confounder on the A → Y direct path would need to be associated with both race and denial at a risk ratio ≥ 1 . 68 to explain aw ay the IDE. While more modest than would be ideal, this reflects the smaller direct ef fect estimate and underscores that the primary channel of inequality operates indirectly through structural mechanisms. 5.5. V isual decomposition Figure 2 presents the full causal decomposition of the racial denial gap from the real HMD A data graphically . 12 Decomposing Discrimination Rajamanickam (2026) 0 pp 2 pp 4 pp 6 pp 8 pp White rate = 9.5% Black rate = 17.0% T otal ef fect IDE (direct) IIE (indirect) IIE via DTI IIE via credit score IIE via income IIE via L TV 7 . 9 1 . 9 6 . 1 2 . 4 1 . 6 1 . 4 0 . 7 Racial denial gap (percentage points) Figure 2. Decomposition of the 7.9 pp racial denial gap (real HMD A data, NY 2022) into interventional direct and indirect ef fects. The IDE (1.9 pp, 23.4%) pro vides a lower bound on direct discrimination under Proposition 3.3 . The IIE (6.1 pp, 76.6%) captures structural inequality propagated through financial mediators; the largest paths are via DTI (2.4 pp), credit score (1.6 pp), income (1.4 pp), and L TV (0.7 pp). Path-specific IIEs allocated proportionally from product-of-coef ficients estimates. T otal Effect (TE) Direct Effect (IDE) Indirect Effect (IIE) 0 2 4 6 8 10 Effect Size (percentage points) 7.94 pp 1.86 pp 6.09 pp IDE = 23.4% (Disparate Treatment) IIE = 76.6% (Disparate Impact) E -value = 1.68 Causal Decomposition of R acial Disparity Real HMDA Data NY 2022, Conventional Home Purchase Figure 3. Causal decomposition of the racial denial disparity estimated from real HMD A data (Ne w Y ork State, 2022). The total ef fect of 7.94 pp decomposes into an interventional direct ef fect (IDE) of 1.86 pp (23.4%, corresponding to ECOA disparate treatment) and an interventional indirect effect (IIE) of 6.09 pp (76.6%, corresponding to ECO A disparate impact through financial mediators). Error bars sho w W ald 95% confidence interv als from 5-fold cross-fitted AIPW estimation. 13 Decomposing Discrimination Rajamanickam (2026) 5.6. Comparison to SHAP attribution T o demonstrate the inadequacy of SHAP for this decomposition, we train a gradient-boosted classifier predicting denial on all features ( A, M , W ) using the real HMD A data and compute SHAP v alues. SHAP conditions on all features including M ; conditioning on a mediator that is causally downstream of A absorbs the indirect effect into the mediator SHAP values. The SHAP attribution to race thus understates the true direct effect, while attributions to DTI and credit score mix le gitimate credit risk signal with structural inequality in unkno wn proportions. Figure 4 illustrates this decomposition failure. 0 pp 1 pp 2 pp 3 pp 4 pp 5 pp 6 pp 7 pp Race ( A direct) DTI Credit score Income L TV Census tract 1 . 9 2 . 4 1 . 6 1 . 4 0 . 7 0 0 . 8 3 . 2 2 . 1 1 . 5 0 . 5 0 . 7 Attribution to racial denial g ap (percentage points) Causal IDE/IIE decomposition SHAP attribution Figure 4. Causal IDE/IIE decomposition (blue) versus SHAP attribution (red) for the real HMD A data. SHAP attributes only 0.8 pp to race directly—substantially below the causal ˆ IDE = 1 . 9 pp— because conditioning on mediators M absorbs the indirect ef fect into mediator SHAP values. The causal decomposition correctly separates the 1.9 pp direct pathway ( IDE , a conservati ve lo wer bound on NDE ) from the 6.1 pp indirect pathway ( I IE ). SHAP cannot distinguish legitimate risk signals from structural inequality in the mediator attributions. 6. Regulatory and Practical Implications 6.1. Mapping IDE and IIE onto ECO A doctrine The IDE/IIE decomposition maps onto the ECO A legal taxonomy with notable precision. Dis- parate treatment—intentional discrimination based on a protected characteristic— corresponds to the IDE: the portion of the denial gap that persists e ven when the mediating financial features are equalized across racial groups, representing model beha viour that cannot be justified by financial risk. Disparate impact—facially neutral practices with discriminatory ef fects—corresponds to the IIE: the portion that flows through financial mediators that are themselves shaped by historical discrimination. The leg al significance of this mapping is that the two doctrines have different defences. Disparate treatment under ECO A has no b usiness necessity defence; it is per se unla wful. Dis- parate impact can be defended if the lender demonstrates business necessity (the financial feature genuinely predicts creditworthiness), b ut the lender must also show that no less-discriminatory 14 Decomposing Discrimination Rajamanickam (2026) 1 1 . 5 2 2 . 5 3 3 . 5 4 2 4 6 8 E-value = 1.68 95% CI lower bound E-value = 1.09 Risk ratio of unmeasured confounder with A (after conditioning on W ) Risk ratio with Y needed to explain aw ay IDE IDE central estimate 95% CI lo wer bound Figure 5. E-v alue sensitivity curv e for the interventional direct ef fect (IDE) estimate from real HMD A data. The solid curve traces the confounder associations required to explain away ˆ IDE = 1 . 9 pp; the dashed curve corresponds to the 95% CI lower bound. The E-v alue for the central estimate is 1.68: an unmeasured confounder on the A → Y direct path would need risk-ratio-scale associations ≥ 1 . 68 with both race (gi ven W ) and denial (gi ven A, M , W ) to nullify the observ ed IDE. The smaller E-value compared to the indirect pathway reflects the primary finding that most disparity flows through structural channels rather than direct discrimination. alternati ve is av ailable. Our decomposition enables this analysis: if the IIE via DTI dominates, the lender can argue b usiness necessity while separately being required to address the upstream inequality that inflated Black applicants’ DTI ratios. 6.2. Deployment at resource-constrained institutions Community banks and credit unions face disproportionate ECO A compliance b urdens rel- ati ve to their data science capacity . The CFPB’ s 2022 algorithmic fairness guidance calls for explainability and bias testing b ut does not specify methodology , creating uncertainty for small institutions. CausalFair addresses this g ap with three modules: causal_fair.dag (D A G specification with domain constraints), causal_fair.estimate (cross-fitted AIPW esti- mation with causal forests), and causal_fair.sensitivity (E-v alue computation and CFPB-compatible reporting). The full pipeline on the 89,465-application real HMD A dataset (with 30,000 subsampled for AIPW cross-fitting) completes in under one minute on a standard laptop with logistic regression nuisance models. 7. Limitations D A G misspecification. Identification results depend on the credit D A G of Definition 3.1 , particularly the assumption that census tract characteristics are pre-treatment co variates in W rather than mediators. T o the extent that census tract composition partly reflects historical racial sorting (making it potentially downstream of A ), some variables in W may be mediators. In the 15 Decomposing Discrimination Rajamanickam (2026) White ( n = 8 2 , 7 2 1 ) Black ( n = 6 , 7 4 4 ) 0.0 2.5 5.0 7.5 10.0 12.5 15.0 17.5 20.0 Denial R ate (%) 9.5% 17.5% Gap: 7.9 pp (A) Denial R ates by R ace T otal Effect (TE) Direct Effect (IDE) Indirect Effect (IIE) 0 2 4 6 8 10 Effect Size (percentage points) 7.9 pp 1.9 pp 6.1 pp (B) Causal Decomposition IDE (Disparate Treatment) 23.4% IIE (Disparate Impact) 76.6% (C) Decomposition Proportions 0.0 0.5 1.0 1.5 2.0 2.5 3.0 Indirect Effect (percentage points) DTI Credit Score Income L TV 2.4 pp 1.6 pp 1.4 pp 0.7 pp (D) P ath-Specific Indirect Effects 1.0 1.5 2.0 2.5 3.0 3.5 Confounding Strength ( ) 1.0 1.5 2.0 2.5 3.0 3.5 4.0 4.5 5.0 Risk R atio E -value = 1.68 (E) E -value Sensitivity Analysis Confounding bias curve Observed IDE (RR = 1.19) IDE nullified region Metric V alue Sample size 89,465 White applicants 82,721 Black applicants 6,744 White denial rate 9.5% Black denial rate 17.5% T otal Effect (TE) 7.94 pp IDE (Direct) 1.86 pp [0.07, 3.64] IIE (Indirect) 6.09 pp [4.13, 8.05] IDE share 23.4% IIE share 76.6% E -value 1.68 (F) Summary Statistics E m p i r i c a l R e s u l t s : R e a l H M D A D a t a ( N Y 2 0 2 2 , n = 8 9 , 4 6 5 ) Figure 6. Empirical results dashboard for real HMD A data (NY 2022, n = 89 , 465 ). (A) Denial rates by race (White 9.5%, Black 17.0%, gap = 7.5 pp). (B) Causal decomposition: total effect 7.9 pp decomposes into IDE 1.9 pp and IIE 6.1 pp with 95% confidence intervals. (C) Proportion of the total ef fect attrib utable to direct discrimination (IDE, 23.4%) versus structural inequality channeled through mediators (IIE, 76.6%). (D) Path-specific indirect effects: DTI (2.4 pp), credit score (1.6 pp), income (1.4 pp), and L TV (0.7 pp). (E) E-value sensiti vity analysis showing that an unmeasured confounder would need a minimum strength of Γ = 1 . 68 to nullify the IDE. (F) Summary statistics. All estimates from 5-fold cross-fitted AIPW estimation. 16 Decomposing Discrimination Rajamanickam (2026) real HMD A data, Black applicants reside in tracts with 30.5 pp higher minority population share; reclassifying tract v ariables as mediators would further increase the IIE and decrease the IDE. Monotonicity assumption. Proposition 3.3 requires monotone indirect treatment response. While plausible on average (higher DTI weakly increases denial), this may fail for specific applicant subgroups in which small DTI v ariations have minimal impact. In those subgroups, the bounds may not hold uniformly . HMD A data quality . Race in HMD A is self-reported and imputed for a substantial fraction of applications. Credit score quintile is imputed from denial reason codes—an approach that introduces classical measurement error in M , likely biasing ˆ I IE to ward zero. Income is reported at the application le vel and may not reflect permanent income. External validity . Results presented here are from New Y ork State con ventional purchase mortgages in 2022. The IDE/IIE decomposition may differ across states, time periods, and for auto lending, credit cards, or small business financing, where mediator structures and confounding patterns dif fer . A multi-state replication using the full national HMD A dataset is a priority for future work. Sample size imbalance. The real HMD A dataset contains 82,721 white and 6,744 Black applicants, a 12:1 ratio. While the AIPW estimator is consistent under this imbalance, the smaller Black subsample may reduce power for detecting small direct ef fects and inflate standard errors on the IDE, contributing to the wider confidence interv al [0.1, 3.6] pp. 8. Conclusion W e have introduced a causal mediation framew ork that decomposes racial disparities in AI-dri ven credit decisions into their direct and indirect causal components. The core contrib ution is an identification strategy for interventional direct and indirect effects under treatment-induced confounding—the empirically pre v alent setting in credit data where sequential ignorability fails. Under Modified Sequential Ignorability ( M S I ) and monotone indirect treatment response, the identified IDE and IIE bound the unidentified natural effects, providing le gally actionable quanti- ties that map onto the ECO A disparate treatment and disparate impact doctrines respectiv ely . Applied to 89,465 real HMD A con ventional purchase mortgage applications from New Y ork State (2022), we found that approximately 77% of the 7.9 pp racial denial gap operates through the indirect pathway—financial mediators shaped by structural inequality—with DTI (2.4 pp), credit score (1.6 pp), income (1.4 pp), and L TV (0.7 pp) as the dominant channels. The remaining 23% (1.9 pp) constitutes a conservati ve lower bound on direct discrimination (E-v alue 1.68). These structural inequality channels are in visible to SHAP-based attribution, which conflates the two causal mechanisms by conditioning on mediators. 17 Decomposing Discrimination Rajamanickam (2026) The practical implication is clear: fair lending compliance based on SHAP attribution is systematically incomplete. It correctly identifies which model features predict racially disparate outcomes but cannot determine whether those features act as legitimate credit risk signals or as carriers of historical structural inequality—a distinction with opposite policy and legal implications. In the real HMD A data, the dominance of the indirect pathway (76.6% of the total ef fect) implies that addressing racial disparities in mortgage lending requires not only eliminating direct discrimination but also confronting the upstream structural inequalities in income, wealth, and credit access that produce racially disparate financial profiles. The CausalFair software makes this decomposition accessible to the broad base of community financial institutions currently lacking the infrastructure to deploy causal fairness methods. Future work will extend this analysis to the full national HMDA dataset across multiple states and years, to continuous protected attributes, to dynamic lending relationships where race af fects credit access over time ( Creager et al. , 2020 ), and to heterogeneous IDE/IIE estimation by applicant subgroup to enable targeted remediation. W e also plan to in vestigate decomposition of the IIE by upstream structural mechanism using administrati ve data linkages. A. F ormal Proof of Pr oposition 3.2 W e pro vide the full proof under Assumption 3.1 . Step 1: Identify µ ( a, m, w ) . Under ( MSI.1 ) , for any fix ed ( a, m, w ) , Y ( a, m ) ⊥ ⊥ A | W . By consistency Y = Y ( A, M ( A )) , we hav e for all ( a, m ) : E [ Y ( a, m ) | W = w ] = E [ Y ( a, m ) | A = a, W = w ] = E [ Y | A = a, M = m, W = w ] ≡ µ ( a, m, w ) where the first equality uses ( MSI.1 ) and the second uses consistency and positivity ( MSI.3 ) . Hence µ is identified by re gression of Y on ( A, M , W ) . Step 2: Identify F ( m | a, w ) . Under ( MSI.2 ), M ( a ) ⊥ ⊥ A | W . By consistency M = M ( A ) : P ( M ( a ) ≤ m | W = w ) = P ( M ( a ) ≤ m | A = a, W = w ) = P ( M ≤ m | A = a, W = w ) where the first equality uses ( MSI.2 ) and the second uses consistency . Hence F ( m | a, w ) is identified from the empirical conditional CDF of M given ( A = a, W = w ) . 18 Decomposing Discrimination Rajamanickam (2026) Step 3: Identify IDE. IDE = E E [ Y (1 , M ∗ ) − Y (0 , M ∗ ) | W ] = Z E Y (1 , m ) − Y (0 , m ) | W = w d F ( m | A = 0 , w ) d F ( w ) = Z Z µ (1 , m, w ) − µ (0 , m, w ) d F ( m | A = 0 , w ) d F ( w ) where the second line uses M ∗ ∼ G 0 = F ( · | A = 0 , W ) and the tower property , and the third line substitutes the identified functionals from Steps 1–2. The IIE identification follows analogously . □ B. Pr oof of Pr oposition 3.3 Under Assumption 3.2 , Y i ( a, m ) is non-decreasing in m component-wise for all units i . Denote M (0) i as the indi vidual-lev el counterfactual mediator under do( A = 0) for unit i , and M ∗ i ∼ G 0 = F ( · | A = 0 , W i ) as an independent dra w from the population distribution. In the HMD A sample, M (1) ≥ st M (0) component-wise: Black applicants face higher DTI (+2.9 pp), higher L TV (+7.7 pp), and lower credit scores ( − 0 . 18 quintile) on av erage due to structural inequality . The indi vidual counterfactual M (0) i equals the unit’ s actual mediator under counterfactual A = 0 . For units where the structural inequality pathway is strong (i.e., M (1) i substantially exceeds M (0) i ), the population a verage E [ M ∗ i ] may exceed the indi vidual M (0) i for some units. By Jensen’ s inequality under monotonicity: E i [ Y i (1 , M (0) i )] ≥ E i [ Y i (1 , E [ M ∗ i | W i ])] ≥ E i [ Y i (1 , M ∗ i )] Therefore NDE = E [ Y (1 , M (0)) − Y (0 , M (0))] ≥ E [ Y (1 , M ∗ ) − Y (0 , M ∗ )] = IDE . The bound I IE ≥ NIE follo ws by the same argument applied to the indirect component. □ Refer ences Miguel Alv es et al. T o wards f air AI: Mitigating bias in credit decisions — a system- atic literature re view . J ournal of Risk and F inancial Management , 18(5):228, 2025. doi: 10.3390/jrfm18050228 . URL https://ideas.repec.org/a/gam/jjrfmx/ v18y2025i5p228- d1641302.html . Solon Barocas, Moritz Hardt, and Arvind Narayanan. F airness and Machine Learning: Limita- tions and Opportunities . MIT Press, 2023. URL https://fairmlbook.org . Robert Bartlett, Adair Morse, Richard Stanton, and Nancy W allace. Consumer-lending discrimination in the FinT ech era. J ournal of F inancial Economics , 143(1):30–56, 19 Decomposing Discrimination Rajamanickam (2026) 2022. doi: 10.1016/j.jfineco.2021.05.047 . URL https://www.sciencedirect.com/ science/article/abs/pii/S0304405X21002403 . Silvia Chiappa. Path-specific counterfactual fairness. In Pr oceedings of the AAAI Confer ence on Artificial Intelligence , volume 33, pages 7801–7808, 2019. doi: 10.1609/aaai.v33i01.33017801 . URL https://aaai.org/papers/ 07801- path- specific- counterfactual- fairness/ . Elliot Creager , David Madras, T oniann Pitassi, and Richard Zemel. Causal modeling for fairness in dynamical systems. In Pr oceedings of the 37th International Confer ence on Machine Learning , v olume 119 of Pr oceedings of Mac hine Learning Resear ch , pages 2185–2195, 2020. URL https://proceedings.mlr.press/v119/creager20a.html . Iván Díaz and Nima S. Hejazi. Causal mediation analysis for stochastic interventions. Journal of the Royal Statistical Society: Series B , 82(3):661–683, 2020. doi: 10.1111/rssb .12362 . URL https://arxiv.org/abs/1901.02776 . K osuke Imai, Luke K eele, and Dustin T ingley . A general approach to causal mediation analysis. Psycholo gical Methods , 15(4):309–334, 2010. doi: 10.1037/a0020761 . URL https:// pubmed.ncbi.nlm.nih.gov/20954780/ . Zhi Jiang, Peng Ding, and Zijian Guo. DeepMed: Semiparametric causal me- diation analysis with debiased deep learning. In Advances in Neural Infor- mation Pr ocessing Systems , v olume 35, pages 27237–27249, 2022. URL https://proceedings.neurips.cc/paper_files/paper/2022/hash/ b57939005a3cbe40f49b66a0efd6fc8c- Abstract- Conference.html . Nikita K ozodoi, Johannes Jacob, and Stefan Lessmann. Fairness in credit scoring: Assessment, implementation and profit implications. Eur opean Journal of Operational Resear ch , 297 (3):1083–1094, 2022. doi: 10.1016/j.ejor .2021.06.023 . URL 2103.01907 . Matt J. Kusner , Joshua Loftus, Chris Russell, and Ricardo Silv a. Counterfactual fairness. In Advances in Neural Information Pr ocessing Systems , volume 30, pages 4066–4076, 2017. URL https://papers.nips.cc/paper/6995- counterfactual- fairness . Scott M. Lundberg and Su-In Lee. A unified approach to interpreting model predic- tions. In Advances in Neural Information Pr ocessing Systems , volume 30, pages 4765– 4774. Curran Associates, Inc., 2017. URL https://papers.nips.cc/paper/ 7062- a- unified- approach- to- interpreting- model- predictions . Joris M. Mooij, Jonas Peters, Dominik Janzing, Jakob Zscheischler , and Bernhard Schölkopf. Distinguishing cause from effect using observ ational data: Methods and benchmarks. J ournal 20 Decomposing Discrimination Rajamanickam (2026) of Machine Learning Resear ch , 17:1–102, 2016. URL https://jmlr.org/papers/ v17/14- 518.html . T rang Quynh Nguyen, Ian Schmid, and Elizabeth A. Stuart. Clarifying causal mediation analysis for the applied researcher: Defining effects based on what we want to learn. Psyc hological Methods , 27(2):243–259, 2022. doi: 10.1037/met0000299 . URL https://pubmed.ncbi. nlm.nih.gov/38720813/ . Judea Pearl. Direct and indirect effects. In Pr oceedings of the Seventeenth Conference on Uncertainty in Artificial Intelligence , pages 411–420. Mor gan Kaufmann, 2001. URL https: //dl.acm.org/doi/10.5555/2074022.2074073 . James M. Robins and Sander Greenland. Identifiability and exchangeability for direct and indirect ef fects. Epidemiology , 3(2):143–155, 1992. doi: 10.1097/00001648-199203000-00013 . URL https://pubmed.ncbi.nlm.nih.gov/1576220/ . Eric J. Tchetgen Tchetgen and Ilya Shpitser . Semiparametric theory for causal mediation analysis: Ef ficiency bounds, multiple robustness and sensitivity analysis. Annals of Statistics , 40(3): 1816–1845, 2012. doi: 10.1214/12-A OS990 . URL https://projecteuclid. org/journals/annals- of- statistics/volume- 40/issue- 3/ Semiparametric- theory- for- causal- mediation- analysis- - Efficiency- bounds- multiple/ 10.1214/12- AOS990.full . T yler J. V anderW eele. Explanation in Causal Infer ence: Methods for Mediation and Interac- tion . Oxford Univ ersity Press, 2015. URL https://global.oup.com/academic/ product/explanation- in- causal- inference- 9780199325870 . T yler J. V anderW eele and Peng Ding. Sensiti vity analysis in observational research: Introducing the E-value. Annals of Internal Medicine , 167(4):268–274, 2017. doi: 10.7326/M16-2607 . URL https://pmc.ncbi.nlm.nih.gov/articles/PMC6768718/ . Stefan W ager and Susan Athey . Estimation and inference of heterogeneous treatment ef fects using random forests. J ournal of the American Statistical Association , 113(523):1228–1242, 2018. doi: 10.1080/01621459.2017.1319839 . URL https://www.tandfonline.com/ doi/full/10.1080/01621459.2017.1319839 . Qingyuan Zhao and T rev or Hastie. Causal interpretations of black-box models. Journal of Business & Economic Statistics , 39(1):272–281, 2021. doi: 10.1080/07350015.2019.1624293 . URL https://pubmed.ncbi.nlm.nih.gov/33132490/ . 21

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment