Towards European Hydrogen Market Design: Perspectives from Transmission System Operators

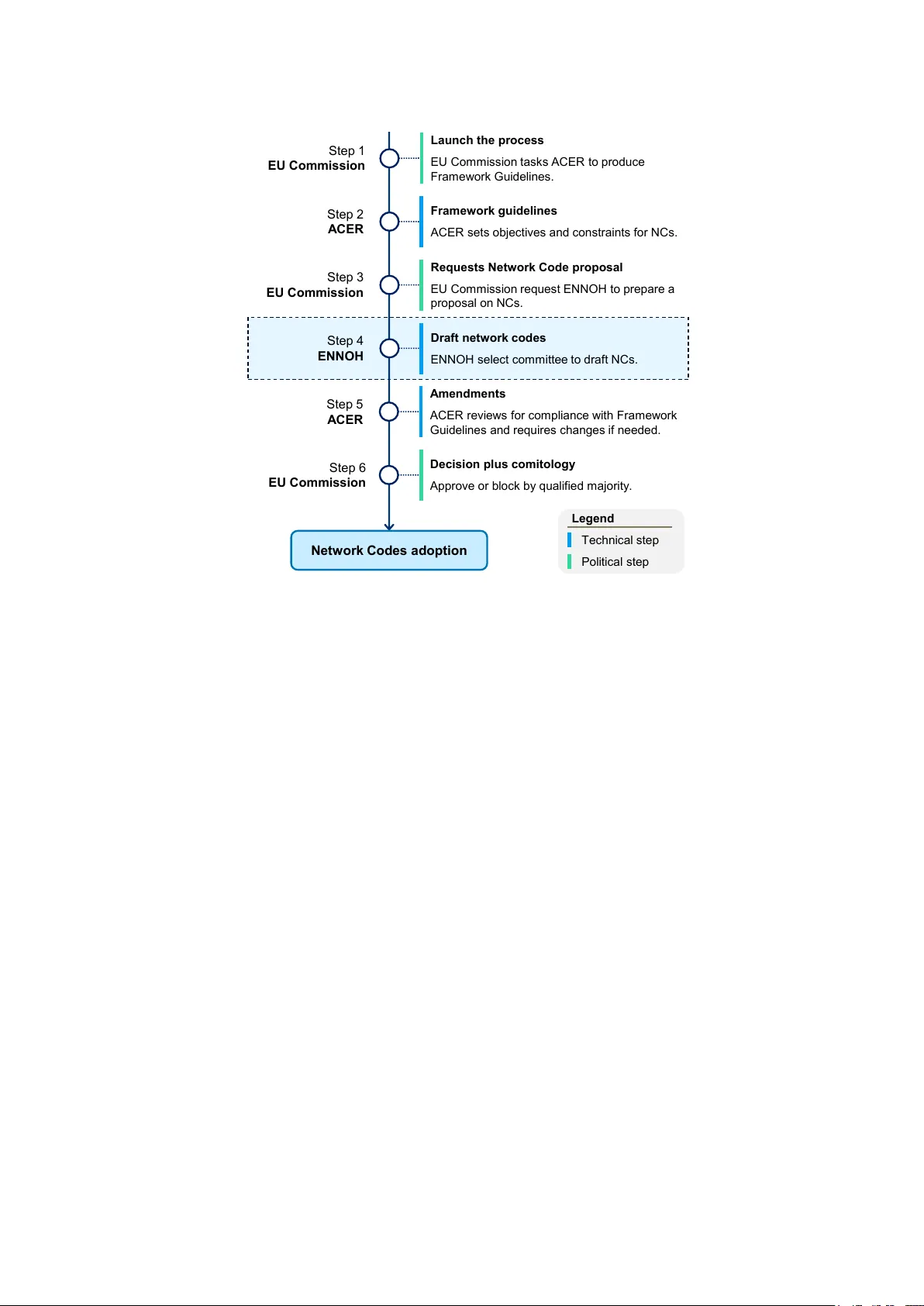

Despite hydrogen being central to Europe's decarbonisation strategy, only a small share of renewable hydrogen projects reached final investment decision. A key barrier is uncertainty about how future hydrogen markets will be designed and operated, pa…

Authors: Marco Saretta, Enrica Raheli, Jalal Kazempour

T o w ards Europ ean Hydrogen Mark et Design: P ersp ectiv es from T ransmission System Op erators Marco Saretta a,b, ∗ , Enrica Raheli b , Jalal Kazemp our a a T e chnical University of Denmark, Kgs. Lyngby, Denmark b R amboll Denmark A/S, Cop enhagen, Denmark Abstract Despite h ydrogen b eing cen tral to Europ e’s decarb onisation strategy , only a small share of re- new able h ydrogen pro jects reac hed final in vestmen t decision. A k ey barrier is uncertain ty about ho w future hydrogen markets will b e designed and op erated, particularly under Renew able F uels of Non-Biological Origin requiremen ts. This study inv estigates the exten t to which future hydro- gen mark et design can b e adapted from existing natural gas mark ets, and the c hallenges it must address. The analysis was based on a survey targeting Europ ean gas transmission system opera- tors, structured around five comp onen ts: market design principles, trading frameworks, capacity allo cation, tariffs, and balancing. The survey produced tw o outputs: an assessment of mec hanism transferabilit y and an iden tification of challenges for early h ydrogen mark et dev elopmen t. Core mark et design principles and trading frameworks are broadly transferable from natural gas markets, as en try-exit systems and virtual trading p oints. Capacity allo cation requires targeted adaptation to impro v e coupling with electricit y mark ets. T ariffs require adaptation through in tertemp oral cost allo cation, distributing infrastructure costs o ver time to protect early adopters. Balancing regimes should b e revisited to reflect hydrogen’s physical characteristics and different linepack flexibility usages. Key challenges for early hydrogen markets include: temp oral mismatches b et ween v ariable renew able supply and exp ected relativ ely stable industrial demand, limited operational flexibility due to scarce storage and reduced pip eline linepack, fragmented regional hydrogen clusters, and regulatory uncertaint y affecting long-term in v estment decisions. These findings pro vide empirical input to the hydrogen net work code led b y the Europ ean Netw ork of Hydrogen Netw ork Op erators and offer guidance to p olicymak ers designing h ydrogen market frameworks. Keywor ds: Hydrogen mark et design, Hydrogen p olicy, Balancing mec hanisms, Gas market fundamen tals, Sector coupling Nomenclature Acron yms A CER Agency for the Co op eration of Energy Regulators CET Cen tral Europ ean Time DSO Distribution System Op erator EEX Europ ean Energy Exchange AG EHB European Hydrogen Backbone ENTSOE Europ ean Netw ork of T ransmission System Operators for Electricity ∗ Corresp onding author. Email addresses: mcsr@dtu.dk (Marco Saretta), enri@ramboll.com (Enrica Raheli), jalal@dtu.dk (Jalal Kazemp our) Pr eprint submitte d to Energy Policy Mar ch 30, 2026 ENTSOG Europ ean Netw ork of T ransmission System Op erators for Gas ENNOH Europ ean Netw ork of Netw ork Op erators for Hydrogen EU Europ ean Union H 2 Hydrogen OTC Ov er-the-Counter RAB Regulatory Asset Base NC Net work Co des NC BAL Net work Co des on Balancing Regimes NC CAM Net work Co des on Capacity Allo cation NC T AR Net work Co des on T ariff Structures RFNBO Renew able F uels of Non-Biological Origin STP Standard T emperature and Pressure TSO T ransmission System Op erator TTF Title T ransfer F acilit y VTP Virtual T rading Poin t WDO Within Da y Obligation 2 1. In tro duction 1.1. Context and r ese ar ch gap As Europ e transitions tow ards climate neutrality , low-carbon and renewable hydrogen hav e b een identified as essential for decarb onising hard-to-abate sectors ( Shen et al. , 2024 ). Hydrogen’s cen tral role is also reflected in ambitious Europ ean targets and supp ort sc hemes: the REPo w erEU Strategy aims to reach 10 million tonnes of renewable hydrogen pro duction by 2030, supp orted b y 40 GW of electrolysers, and dedicated financial schemes ( Europ ean Hydrogen Observ atory , 2025 ). F urthermore, the Europ ean Hydrogen Bac kb one initiative aims to develop the pan-Europ ean in- frastructure and pip elines needed to connect pro ducers and consumers, led by 33 future h ydrogen T ransmission System Op erators (TSOs) ( Europ ean Hydrogen Bac kb one , 2024 ). Finally , the Eu- rop ean Commission has published a Delegated Act on Renew able F uels of Non-Biological Origin (RFNBO) ( Europ ean Parliamen t , 2023 ), defining requiremen ts for lo w-carb on and renew able h y- drogen pro ducers, mandating strict pro duction constraints, including temp oral and geographical correlation with renew able generation, additionality , and lifecycle emission thresholds. Y et ambition has not translated in to in vestmen t: despite these ambitious targets, only 25% of the exp ected 2030 renewable h ydrogen capacity has reached final inv estment decision ( F raile et al. , 2025 ). One reason for this is the uncertaint y around future market design. Without kno wing the rules under whic h the market will op erate, developers and off-takers are negatively affected on the bank abilit y of their pro jects ( Lagioia et al. , 2023 ). These rules are exp ected to b e co dified in dedicated Netw ork Co des (NC). Ho w ever, the dev elopment of NC is often a lengthy , m ulti-part y and m ulti-stage regulatory pro cess, illustrated in Figure 1 , in whic h the drafting responsibility is assigned to the Europ ean Net w ork of Netw ork Op erators for Hydrogen (ENNOH) under the sup er- vision of the Agency for the Co operation of Energy Regulators (ACER). Un til the hydrogen NC en ters into force, inv estors face an uncertain market framework, discouraging pro jects in vestmen t. While the EU natural gas market is often referenced as a mo del for future h ydrogen mark et design ( Johnson et al. , 2025 ), fundamental ph ysical and op erational differences (T able 1 ) prev ent direct replication. Hydrogen’s densit y is appro ximately one-ten th that of natural gas, directly re- ducing the mass of gas that can b e stored in pip elines at a giv en pressure, and although hydrogen has a higher Lo wer Heating V alue, its low er density results in a substan tially lo wer volumet- ric energy densit y , reducing av ailable linepack flexibility (i.e., the energy stored in pip elines for balancing purp oses). F rom an op erational p erspective, infrastructure limitations aggra v ate these ph ysical constraints: early Europ ean net works are exp ected to emerge as fragmented regional clus- ters rather than interconnected systems, and will initially lack mature bulk storage infrastructure. Hence, future market design cannot simply replicate gas mark et mechanisms, and it must accoun t for h ydrogen distinct physical and op erational c haracteristics. Recen t research addressed h ydrogen market design in Europ e from multiple persp ectives. A cen tral reference is Steinbac h and Bunk ( 2024 ), which deriv es three key market design criteria T able 1: Key physical and op erational differences b et ween hydrogen and natural gas transp ort. Density rep orted at Standard T emperature and Pressure (0 ° C, 1 bar). P arameter Natural Gas Hydrogen Densit y (STP) ∼ 0.75 kg/m 3 0.09 kg/m 3 Lo wer Heating V alue 50 MJ/kg 120 MJ/kg V olumetric Energy Density 39 MJ/m 3 10.8 MJ/m 3 Linepac k Capacity High Low Net work Maturit y P an-Europ ean F ragmen ted (early phase) Storage Av ailability Mature Limited (early phase) 3 L aun ch t h e p r o ce ss E U Com m i s s i on tas k s A CE R to produc e F r am ew ork G ui de l i ne s . S t ep 1 E U C ommi ssi on F r amew o r k g u idelines A CE R s ets ob j ec ti v es an d c on s tr ai nts f or NCs . S t ep 2 A C E R Dra f t n etw o r k cod es E NNO H s el ec t c om m i tte e to draf t NCs . S t ep 4 E N N O H A men d men t s A CE R r ev i ew s f or c om pl i an c e w i th F r am ew ork G ui de l i ne s an d r eq ui r es c ha ng es i f ne ed ed . S t ep 5 A C E R Deci sion plu s com it o log y A pp r ov e o r bl oc k by qu al i f i ed m aj orit y . S t ep 6 E U C o mmi ssi o n L egen d T ec hn i c al s tep P ol i ti c al s tep Requ es t s Net w o r k Co d e p r o p o sa l E U Com m i s s i on r eq ue s t E NNO H to prepare a propos al on NCs . S t ep 3 E U C ommi ssi on N etw or k C od es ad op t i on Figure 1: Netw ork Codes dev elopment pro cess for hydrogen in the European Union. This publication aims to con tribute to the fourth step by pro viding informed insights that will b e useful to ENNOH in drafting the Netw ork Co des. Image adapted from ENTSOE ( 2023 ). through in terviews with stak eholders across the h ydrogen v alue chain: policy supp ort measures, infrastructure regulation, and trading arrangemen ts. The study highligh ts the need, within these areas, to reduce regulatory uncertaint y , provide targeted financial supp ort, and in tro duce funda- men tal natural gas market principles, such as third-part y access, unbundling, and en try-exit sys- tems. Ho wev er, the analysis remains at a conceptual lev el and do es not sp ecify ho w these elemen ts translate into mark et design. Structured design analyses complement this p erspective, with the w ork from Niedrig et al. ( 2024 ) examining how market design evolv es across dev elopment stages. The study finds that, in the early phases, a fragmented infrastructure and limited participation are exp ected to fav our bilateral contracts, supp orting in vestmen t but constraining liquidit y . As net works expand and market areas integrate, exchange trading b ecomes feasible, impro ving trans- parency and short-term efficiency . F rom a regulatory economics p ersp ectiv e, Martinez-Ro driguez et al. ( 2026 ) argue that h ydrogen markets differ from natural gas markets due to the need for new infrastructure and w eaker natural-monopoly c haracteristics. The study propose s a mo del based on negotiated access, pip eline-level regulation, and long-term capacit y contracts to supp ort in- v estment, complemented by prop ortionate regulation and mark et-based co ordination mechanisms. Finally , physical and system-lev el studies define the b oundary conditions within which these de- signs must operate. Sargen t and Sargent ( 2025 ) show that hydrogen provides significan tly less usable linepack than natural gas, limiting the feasibility of balancing regimes based on passive flexibilit y . F urthermore, in tegrated energy system mo dels confirm the long-term role of h ydrogen net works in Europ e ( Neumann et al. , 2023 ), particularly in linking renewable supply regions with demand centres and reducing system costs, but typically assume p erfect co ordination and do not accoun t for detailed market rules, such as access and balancing mec hanisms. The literature con v erges on sev eral conclusions: regulatory clarity is a prerequisite for in v est- 4 men t, gas market mec hanisms are only partially transferable to h ydrogen, and physical constrain ts narro w the op erational flexibility av ailable to mark et designers. Despite these research efforts, a critical gap remains: no existing study offers a comprehensive analysis of how the future h ydrogen mark et design should b e structured and whic h c hallenges it m ust accoun t for, b efore b eing drafted in to official Netw ork Co des. 1.2. R ese ar ch questions and c ontributions This pap er addresses the identified gap via tw o researc h questions: (i) to what exten t can future h ydrogen design b e adapted or replicated from the current EU natural gas one? and (ii) what c hallenges must the hydrogen mark et design account for? T o address these questions, a structured surv ey was developed, targeting Europ ean gas TSOs. The survey results lead to tw o main contributions, b oth aimed at informing ENNOH during the drafting of h ydrogen Net work Co des in Step 4 of Figure 1 . First, it assesses the transferabilit y of gas mark et mechanisms to hydrogen across the five regulatory areas, iden tifying which are replicable and whic h require adaptation with minor or ma jor adjustments due to technical and op erational constrain ts. Second, it presents a risk analysis of challenges from TSO consultation, organised into op erational and regulatory challenges. 1.3. Pap er structur e The pap er is structured as follows. Section 2 presents the surv ey design and data analysis. Sec- tions 3 and 4 present the results of the study , respectively assessing the transferability of gas market comp onen ts to hydrogen and identifying the challenges in designing future h ydrogen markets. Sec- tion 5 discusses implications for market design and infrastructure p olicy . It is assumed that the reader is familiar with the general concepts of EU gas markets, e.g., entry-exit systems, capacity allo cation, nominations, balancing framew orks, virtual trading p oints, and commo dity trading. F or readers unfamiliar with these concepts, a comprehensive technical ov erview is provided in the supplemen tary materials ( Marco Saretta , 2025 ). 2. Metho ds T o address researc h questions (i) and (ii), the study employ ed a survey to collect the insights and p erspectives from EU gas TSOs. TSOs were selected as the primary survey recipien t due to their op erational exp ertise in gas netw ork managemen t and their roles in h ydrogen infrastructure dev elopment. The underlying metho dology was organised into three stages (Figure 2 ): survey design, TSO consultation, and results pro cessing. Complemen tary details on the metho dology are pro vided in App endix A . 2.1. Survey design A survey w as dev elop ed to assess the transferabilit y of EU gas mark et mechanisms to hydrogen net works and identify future challenges, totalling 37 questions. The survey was organised into fiv e sections: (a) Market and Regulatory Design, (b) T rading F ramew ork, (c) Net work Co des on Capacity Allocation (NC CAM), (d) Net work Codes on T ariff Structures (NC T AR), and (e) Net work Co des on Balancing Regimes (NC BAL). Sections (a) and (b) addressed general mark et design and trading mechanisms derived from the EU Hydrogen and Decarb onised Gas Mark et P ack age ( Europ ean Commission , 2025 ), while sections (c), (d), and (e) explored the adaptation of current EU natural gas net w ork co des for h ydrogen. Each section had its questions organised in to subtopics. Section (a) cov ered en try-exit systems, hydrogen da y/y ear, the role of shipp ers and DSO co operation. Section (b) included questions on Virtual T rading Poin ts (VTPs), Ov er-The- Coun ter (OTC) trading, the role of exchange-based platforms and general pricing structure. Section 5 Ra m b oll 1 Rep l i c a b l e M i n o r c h a n g e s M aj or c ha ng es 1 . Surv e y de s ig n Su rv e y s e c ti o n s 2 . TSOs c on s ul ta tio n s 3 . Res ul ts proc e s s in g A . M a r k e t d e s ign C . N C C a p a c it y E . N C B a lan c ing D . N C Tar if f s B . Tr a d ing f r a m e w o r k L i te ra tu re re v i e w Su rv e y d a ta Su b m i tt e d to EU G a s T SO s Cha l l e n g e s ri s k a n a l y s i s M a rk e t d e s i g n a n a l y s i s An s w e rs a m o n g DE, DK, FR, NL, BE, L T Im p a c t L i k e l i h o o d 1 st Ou t p u t 2 nd Ou t p u t Figure 2: Three-stage metho dology for assessing h ydrogen market design through TSO consultation. (c) addressed capacit y pro ducts, capacity allo cation mechanisms, nomination and renomination pro cedures, building from the natural gas NC CAM ( ENTSOG , 2017 ). Section (d) co vered capacit y pricing and congestion pro cedures based on the natural gas NC T AR ( ENTSOG , 2018b ). Section (e) addressed balancing regimes, the role of linepac k flexibilit y , and within-day obligations (WDOs), based on the natural gas NC BAL ( ENTSOG , 2018a ). Questions across the five sections were form ulated as a mix of op en-ended and yes/no formats. Before its distribution, the survey w as pilot-tested with Energinet (Danish TSO) in August 2024, after whic h questions w ere refined based on feedbac k. 2.2. TSO c onsultation and data c ol le ction All Europ ean gas TSOs w ere identified from the ENTSOG member directory , totalling 43 op- erators. F rom this set, TSOs w ere prioritised based on the presence of national hydrogen strategies and announced h ydrogen infrastructure dev elopments, in order to capture p ersp ectiv es from op era- tors already engaged in strategic dev elopment of h ydrogen net wor k planning. TSOs w ere con tacted b et w een Septem b er 2024 and January 2025. T o preserve confiden tiality , the TSO organisations and individual resp ondents w ere anon ymised, with resp onses rep orted only at the coun try level. Ex- cluding non-resp onses and declined participation, the survey received seven resp onses from TSOs across six countries: Belgium, Denmark, F rance, Germany , Lith uania, and the Netherlands. These coun tries account for appro ximately 45% of the planned length of the Europ ean hydrogen pip eline b y 2040, according to the Europ ean Hydrogen Backbone data ( ENTSOG et al. ). Interview ees held p ositions in op erations management, strategic planning, and regulatory affairs. 2.3. Data pr o c essing and synthesis Surv ey data was pro cessed as follows. Survey resp onses w ere analysed to identify patterns of agreement, div ergence, and uncertaint y across TSOs. Instances where consensus w as limited or absent are explicitly rep orted in the results. The pro cessed data pro duced tw o main outputs. The first is a transferabilit y assessment examining how current gas market mechanisms could b e applied to h ydrogen markets, with eac h mechanism categorised as fully replicable, replicable with minor mo difications, or replicable only with ma jor mo difications (Section 3 ). The second is a classification of challenges that hydrogen market design will need to accommo date, based on sub jects iden tified across surv ey resp onses (Section 4 ). These c hallenges were classified as either op erational or regulatory and subsequen tly assessed using a risk matrix, mapping them b y lik eliho o d and impact. 6 Ra m b oll 1 M ar ke t and reg u lat o ry d esig n En try /Ex i t Rol e o f Ex c h a n g e s DSO c o o rd i n a ti o n Hy d ro g e n d a y /ye a r Rol e o f s h i p p e rs NC CA M Cap a c i ty p ro d u c ts Cap a c i ty ta ri ff Cap a c i ty a l l o c a ti o n NC T A R Nom i n a ti o n Ren o m i n a ti o n NC BA L Pri c i n g Vi rtu a l tra d i n g p o i n ts O v e r - T h e - Cou n te r T rad in g f r amew o r k Ba l a n c i n g re g i m e L i n e p a c k W i th i n - D a y O b l i g a ti o n Con g e s ti o n Fully r e p li c a b le R e p li c a b le, m ino r c h a n g e s R e p li c a b le, m a jor c h a n g e s Lege nd Figure 3: T ransferability assessment of natural gas market design structure for the hydrogen market. Market design comp onen ts across five regulatory areas are classified into three categories based on TSO consensus: fully replicable (green), replicable with minor changes (yello w), and replicable with ma jor changes (orange). Assessment based on consultations with seven Europ ean gas TSOs representing Belgium, Denmark, F rance, Germany , Lithuania, and the Netherlands. 3. T ransferability of gas mark et mechanisms to hydrogen This section assesses the extent to which the current gas market can serve as a reference mo del for the design of the future hydrogen market. The assessment has b een conducted for each of the five survey sections, namely market and regulatory design, trading framework, Netw ork Co des on capacity allo cation mec hanisms, Netw ork Co des on capacit y tariffs, and Net work Co des on balancing schemes. Eac h survey section subtopic has b een translated into a mark ed design comp onen t and further categorised as fully replicable, replicable with minor mo difications, or with ma jor changes, as display ed in Figure 3 . 3.1. Market and r e gulatory design The market and regulatory design survey section w as structured around four subtopics: entry- exit systems, h ydrogen da y and year, shipp er roles and evolution, and DSO coordination. Survey ed TSOs indicated that the transferabilit y of these comp onents is largely set b y the EU Hydrogen and Decarb onised Gas Market Pac k age (Directive 2024/1788 and Regulation 2024/1789) ( Europ ean Commission , 2025 ). The entry/exit system is mandated for hydrogen net works b y the EU Hydrogen and Decar- b onised Gas Market Pac k age from Jan uary 2033. Under this system, a net w ork user w ould b ook capacit y at en try and exit p oin ts indep enden tly , with hydrogen injected or withdrawn resp ectively at entry and exit p oin ts in the netw ork. The P ac k age, ho wev er, do es not include an indication of the hydrogen da y and year definitions, as these need to be decided by the mem b er states. How- ev er, survey ed TSOs unanimously indicated the need to align the h ydrogen day and year with the calendar day (00:00-24:00 daily , January-Decem b er annually), moving aw a y from the gas mark et con ven tions (06:00-06:00 UTC gas da y , Octob er-Septem b er gas year). TSOs emphasised that this shift from gas da y/y ear to calendar day/y ear represents a necessary adjustment. The traditional gas mark et da y and year structures were originally designed to match daily and seasonal heating demand patterns. In contrast, aligning the hydrogen gas day with the calendar da y facilitates coupling with electricity mark ets, as hydrogen demand is exp ected to follow industrial load profiles and its pro duction is tightly coupled to the electricity market. The Hydrogen and Decarb onised Gas Mark et P ack age also indicates main taining the entit y of net work users, also known as shipp ers, inherited from existing natural gas market structures. 7 Ra m b oll In te gra te d s hi pp e rs Com m od ity s hi pp e rs Spe c ul a tiv e s hi pp e rs Ea rl y m a rk e t s ta g e M i d m a rk e t s ta g e M a tu re m a rk e t s ta g e Pro d u c e r a n d s h i p p e r c ou pl e d Pro d u c e r a n d s h i p p e r de c ou pl e d En h a n c e d tr ad ing ac tiv ity Figure 4: Expected evolution according to survey ed TSOs of shipper types across h ydrogen mark et developmen t stages. Net work users are defined as customers or p oten tial customers of a system op erator in v olved in transp ort and balancing functions, who are resp onsible for balancing their hydrogen injections and withdraw als ( Europ ean Commission , 2025 ). The terms shipp er and netw ork user are used in terchangeably throughout this pap er. Surv ey ed TSOs exp ect the shipp er’s role to evolv e along differen t market phases. As the hydrogen market ev olv es from early low-liquidit y stages to more mature phases, differen t shipp er t yp es are exp ected to emerge, as illustrated in Figure 4 . In the early stages, integrated shipp ers are exp ected to dominate: these are large energy companies that handle both pro duction and consumption, managing the en tire supply c hain from pro duction to deliv ery with limited trading in teractions. As h ydrogen av ailabilit y and demand grow, commo dit y shipp ers are expected to emerge, fo cusing on buying h ydrogen from pro ducers and selling it to con- sumers without direct in volv ement in pro duction. Finally , in mature mark et phases characterised b y high liquidit y , sp eculativ e shipp ers and traders are anticipated to engage primarily in arbitrage, lev eraging price differen tials across virtual trading points on energy exchanges. Speculative ship- p ers are the last to emerge, as their activity requires a high v olume of trades and sufficien t market liquidit y to generate profitable arbitrage opp ortunities. TSOs anticipated that DSO co op eration framew orks would b e main tained, though DSO in volv e- men t w ould dep end on the developmen t of the lo w-pressure distribution infrastructure. Hydrogen net works are exp ected to b e deplo y ed first through high-pressure transmission systems and later through lo w-pressure distribution, as liquidit y gro ws. Unlike natural gas DSOs, whic h mainly serv e households and smaller industries, hydrogen is exp ected to serve predominan tly large industrial consumers. Therefore, DSO in volv ement will likely b e limited in the early stages, as it is exp ected that TSO will handle h ydrogen transmission until sufficient liquidit y and infrastructure develop. 3.2. T r ading fr amework The trading framew ork section in the surv ey was c haracterised around four subtopics: virtual trading p oints, Over-The-Coun ter trading, exc hange-based platforms, and pricing mec hanisms. Surv eyed TSOs indicated a broad consensus that all of these comp onen ts are transferable from gas mark ets. Virtual trading p oin ts (VTPs) are foundational for a functional hydrogen market, as without them, hydrogen can only b e traded through ph ysical delivery . VTPs enable the transfer of the gas o wnership title, while h ydrogen remains within pipelines, allo wing netw ork users to trade bilaterally and indep enden tly of ph ysical lo cation within the en try-exit zone. Commo dit y trade is expected to follo w tw o configurations: Ov er-The-Counter (OTC) trading and exchange-based platforms. OTC trading inv olves bilateral contracts in whic h the parties agree on the gas volume to b e exc hanged, its price, and the contract’s tenor or duration. OTC agreemen ts are non-standard contracts b ecause they are customised as b oth parties negotiate the contr act details, and are t ypically non-public. Exchange-based trading o ccurs on organised platforms with 8 standardised contracts and public price discov ery , requiring VTPs as underlying infrastructure. The hydrogen mark et is an ticipated to b egin as OTC-dominated due to initial low liquidit y , with pro ducers and imp orters securing long-term supply contracts directly with consumers via bilateral agreemen ts. As netw orks in terconnect and liquidity increases, exchange-based trading is exp ected to dev elop alongside OTC markets, utilising VTPs for contin uous trading. Pricing mec hanisms are expected to follow exchange-based prices as the mark et matures. In the early stages, it is exp ected that OTC trades will dominate and, consequen tly , prices will b e less transparen t, as OTC contract details are not public. As liquidity increases, con tinuous price signals are exp ected to emerge at trading exchanges facilitated by VTPs, analogously to how the Dutc h Title T ransfer F acilit y (TTF) b ecame the reference VTP for natural gas trading in the Netherlands. Exc hange trading w ould likely represent only a p ortion of total volumes, with the remainder traded OTC, though exc hange prices would serve as mark et reference p oin ts. 3.3. Network Co des on Cap acity Al lo c ation Me chanisms The surv ey section on capacity allo cation included four subtopics: capacit y products, capac- it y allo cation mechanisms, nomination and renomination pro cedures. Surv eyed TSOs indicated consensus that these elemen ts are transferable from gas markets with minor adjustments. On the capacity pro ducts, TSOs indicated a preference for issuing them as long-term contracts in early market stages, typically in the form of yearly or multi-y ear agreemen ts, as substan tial infrastructure inv estmen t requires netw ork users to demonstrate long-term commitment. Contract lengths v ary among survey ed TSOs. The Danish TSO reported plans to offer capacity pro ducts ranging from short-term to one-y ear ann ual contracts for up to 15 y ears ahead, with a target b ooking lev el of 0.5 GW for at least 10 y ears needed to justify infrastructure inv estmen t ( ? ). In German y , the Bundesnetzagentur (federal netw ork regulator) established frameworks prop osing standard yearly capacity pro ducts while reserving at least 10% of capacit y for shorter-term pro d- ucts suc h as monthly and daily contracts ( Bundesnetzagen tur , 2024c ). A minor c hange from gas mark ets would align y early pro ducts with calendar years rather than gas years, reflecting h ydrogen’s industrial demand patterns rather than seasonal heating cycles. Regarding capacity allo cation metho ds, survey ed TSOs generally indicated a preference for the first-come first-serv ed allo cation metho d in early market phases, indicating a divergence from natural gas mark ets where auction mechanisms predominate. This preference is due to the expected limited num b er of market participants during initial net w ork developmen t and consequen t low liquidit y . German framew orks sp ecify that when demand exceeds av ailable capacity , allo cation should transition to auction-based mec hanisms to ensure efficien t distribution ( Bundesnetzagen tur , 2024c ). Surv eyed TSOs agreed that nomination and renomination pro cedures should be maintained, al- though gate-closure structures require adaptation to enable coupling with the electricity mark et. At the time of the surv ey , only Danish and German TSOs had developed detailed prop osals, with the other survey ed TSOs indicating that these asp ects were still under developmen t. The Danish TSO prop osal is des cribed as follows. It prop oses op ening h ydrogen nominations after the da y-ahead electricit y mark et has cleared, allo wing shipp ers to submit nominations based on realised mark et outcomes ( Energinet , 2024 ). This is particularly relev an t for mark et participants whose pro duction is closely coupled to electricity m ark ets, e.g., electrolyser-based pro ducers. T o incen tivise accurate nominations, it is also prop osed to implement a fee for nomination errors, as accurate nominations w ould reduce unforeseen hydrogen flo ws and system imbalances, enabling the TSO to minimise reserv e linepac k requirements and maximise a v ailable linepack flexibility for netw ork users. The sp ecific nomination time unit for Denmark, whether 15-minute aligned with electricit y mark ets or 1-hour blo c ks, had not b een finalised at the time of the survey . The German prop osal is contained in the W aKandA do cumen t ( Bundesnetzagentur , 2024c ). It states that shipp ers are required to 9 Ra m b oll 1 Capacity t ar if f EUR /M W h /h Cla s s i c a l ta ri ff In te rte m p o ra l ta ri ff P ea k r eg ul ato r y de bt Y ea r s Earl y m ark et s ta g e M a tu re m a rk e t s ta g e Y ea r s Earl y m ark et s ta g e M a tu re m a rk e t s ta g e Regu lato r y d ebt EUR O v er - r ec ov ery U nder - r ec ov ery O v er - r ec ov ery Unde r - r ec ov ery (a) Classical and in tertemp oral tariff schemes comparison. Ra m b oll 1 Capacity t ar if f EUR /M W h /h Cla s s i c a l ta ri ff In te rte m p o ra l ta ri ff P ea k r eg ul ato r y de bt Y ea r s Earl y m ark et s ta g e M a tu re m a rk e t s ta g e Y ea r s Earl y m ark et s ta g e M a tu re m a rk e t s ta g e Regu lato r y d ebt EUR O v er - r ec ov ery U nder - r ec ov ery O v er - r ec ov ery Unde r - r ec ov ery (b) Pro jected regulatory debt under intertemporal tariff. Figure 5: Intertemporal cost allocation under h ydrogen en try-exit regulation. Panel (a) shows classical versus in tertemp oral tariffs across market stages. P anel (b) shows regulatory debt ev olution ov er time. Adapted from Martinez-Ro driguez et al. ( 2026 ). nominate hourly en try and exit quantities, with TSOs defining uniform deadlines aligned with balancing requirements. Exit nominations are required only for storage injection, cross-b order transp ort, or where multiple shipp ers b ook the same exit p oin t across different balancing groups. A k ey difference b etw een the German and Danish prop osed nomination pro cedures lies in timing sp ecificit y: Denmark anc hors gate closures to day-ahead market outcomes as a design principle, while German y delegates sp ecific times to TSO co ordination, with implemen tation exp ected by Octob er 2026. Renomination procedures would allo w shipp ers to adjust nominations in resp onse to intrada y electricit y price signals. The Danish TSO indicated that net work users must b e able to p erform renominations, whic h is allow ed righ t after the first nomin ation deadline, while more sp ecific details remain under developmen t ( Energinet , 2024 ). German frameworks allow multiple intrada y renom- inations with no frequency limits, provided that deadlines allow sufficient time for TSO pro cessing ( Bundesnetzagen tur , 2024c ). 3.4. Network Co de on T ariffs Net work tariff design in the survey cov ered tw o comp onents: capacity tariff structures and congestion managemen t. Survey ed TSOs indicated that b oth would require fundamental redesign to a void p enalising early market play ers. Capacit y tariffs, generally expressed in EUR/MWh/h, gran t net w ork users the right to inject or withdra w hy drogen up to a con tracted capacity lev el and constitute a primary reven ue stream for TSOs. These rev enues are regulated to ensure cost reco very of the Regulatory Asset Base (RAB), whic h reflects the v alue of approv ed net work assets, including h ydrogen pip elines and repurp osed gas infrastructure. F or hydrogen markets, a cen tral c hallenge arises: if the classical tariff scheme w ere applied from natural gas mark ets, RAB-related costs w ould need to b e recov ered across lo w transp orted volumes, resulting in high p er-unit tariffs. Suc h high tariffs would b e b orne by early net work users, p oten tially deterring participation and slo wing demand gro wth. Therefore, directly adopting traditional natural gas tariff sc hemes for h ydrogen could threaten market dev elopmen t at a stage when net work uptake is most critical. T o address this, the intertemporal cost allo cation sc heme has b een in tro duced in Article 5 of EU Regulation 2024/1789 ( Europ ean Parliamen t , 2024 ), which allo ws TSOs to set tariffs b elo w full cost-recov ery lev els in early market stages, thereby p ostponing the resulting rev en ue gaps to 10 later p erio ds, once netw ork utilisation has gro wn. Figure 5 illustrates the tw o core elements of the mechanism. Panel 5a displa ys illustrative classical and intertemporal tariff pro jections. Under the classical approach, tariffs are initially high b ecause RAB costs are recov ered across low initial transp orted v olumes, and they decline as mark et liquidity grows and more capacity is bo oked. In con trast, intertemporal tariffs are set at a low e r level in early stages, resulting in initial under- reco very , follo wed b y o ver-reco very as mark et liquidit y rises, with the classical tariff falling b elo w it. While sho wn as constant for illustrative purp oses, in practice, the intertemporal tariff is p e- rio dically adjusted as demand forecasts and cost pro jections are up dated. P anel 5b shows the resulting regulatory debt. During the under-recov ery phase, uncollected reven ues accum ulate as debt, whic h p eaks at the transition to o ver-reco very . As rev enues then exceed allow ed costs, the debt is gradually repaid until the break-even p oin t is reached. The mec hanism, therefore, shifts cost reco very forw ard in time while ensuring that netw ork users ultimately b ear all infrastructure costs. F or a comprehensive description of the mechanism, the authors refer to Martinez-Ro driguez et al. ( 2026 ). Survey ed TSOs indicated the need to adopt the intertemporal cost allo cation mechanism. A t the time of the survey , Germany ( Bundesnetzagentur , 2024a ) and Denmark ( Klima Energi og F orsyningsministeriet , 2025 ) ha v e prop osed capacity tariff sc hemes based on intertemporal cost al- lo cation, while the other surv ey ed TSOs indicated that they w ere undergoing regulatory ev aluation of tariff metho dologies. F urthermore, A CER conducted a consultation on hydrogen tariff design ( A CER , 2025a ), con- cluded in July 2025 with an endorsemen t of intertemporal cost allo cation ( A CER , 2025b ). Although its recommendation, ACER stressed that the intertemporal cost allo cation sc heme alone is insuffi- cien t, as hydrogen net works lack binding long-term capacit y commitments, leaving TSOs without predictable reven ues to recov er inv estment costs. Hence, ACER iden tified three complemen tary elemen ts. First, national risk-sharing schemes, suc h as subsidies or pre-bo oking capacity obliga- tions, are needed to directly reduce v olume risk. Second, regulated reven ues must reflect only the residual risks b orne b y TSOs after public supp ort is applied, a voiding double compensation for risks already co v ered b y state instrumen ts. Third, regulatory design m ust ensure credibility and adaptabilit y through scenario-based demand forecasting, immediate reco very of v ariable op erating costs, and explicit appro v al of assets sub ject to intertemporal allo cation. Regarding congestion management, the exp ected limited net work utilization exp ected during early mark et phases leads TSOs to an ticipate low lev els of congestion. As a result, congestion man- agemen t framew orks remain largely under dev elopment across surv ey ed TSOs, and are exp ected to ev olve in parallel with market maturation. 3.5. Network Co des Balancing The NC balancing surv ey cov ered three comp onents: balancing regime design, linepac k allo- cation, and Within-Day Obligations (WDO). Survey ed TSOs indicated that, due to the nature of h ydrogen and its infrastructure, ma jor c hanges will b e required to the balancing regime. While most TSOs are still developing their approac hes, at the time of the survey , initial designs w ere a v ailable for Denmark, Germany , and the Netherlands. The purp ose of a balancing regime is to k eep pip eline pressure within safe op erational b ounds. T o ac hiev e this, TSOs allo cate p ortions of the total av ailable pip eline pressure to sp ecific purp oses. As shown in Figure 6 , a pip eline pressure is generally organised in to four comp onen ts: supp ort linepac k (the minim um cushion gas pressure), reserve linepack held for TSO interv entions, sys- tem linepack flexibilit y (SLF) for balancing, and flow linepac k providing the pressure differential required for transp ort. In essence, a balancing regime is defined by how the SLF portion of the pip eline is used for balancing actions. The survey iden tified three balancing regimes across Ger- man y , Denmark, and the Netherlands, reflected in the Bundesnetzagentur W asABI consultation ( Bundesnetzagen tur , 2024b ), the Energinet prop osal ( Energinet , 2024 ), and the Dutch Hynet w ork 11 Ra m b oll 1 D e s ig n a t e d L in e p a c k Fle x ib ili t y N o n - D e s ign a t e d L ine p a c k Flex ibili t y Lege nd S up po r t Li ne pa c k Res erv e Li ne pa c k S y s tem Li ne pa c k F l ex i bi l i t y ( S LF) F l ow Li ne pa c k N on - DLF T ota l Li ne pa c k P r es sure Ba r P ipel ine le ng t h Km DLF Non - DLF DLF DE In i ti a l Non - DLF DK Hy b ri d (p ro p o s a l ) NL In i ti a l DLF P m i n P m ax Non - DLF Res erv e Li ne pa c k Figure 6: Linepack flexibility regions in hydrogen pipeline systems. The diagram illustrates the system linepack flexibilit y , sub divided into designated linepack flexibilit y (DLF), allo cated to individual net work users, and non- designated linepac k flexibility (Non-DLF), av ailable collectively . Pipeline partition illustration based on ( Energinet , 2024 ). terms and conditions ( Gasunie Netherlands , 2026 ). These balancing regimes differ in their use of a newly in tro duced approach, namely Designated Linepac k Flexibility (DLF), in whic h the total SLF is partitioned in to multiple parts, designated and allo cated to individual users. This con trasts with the traditional gas balancing framew ork, in which SLF is managed at the system lev el via balancing zones and a help er-causer mechanism. F or the purp oses of this pap er, this traditional approac h is referred to as Non-DLF, simply to indicate and differentiate the p ortion of SLF man- aged collectiv ely as in gas markets, from the newly in tro duced DLF approac h. The three balancing regimes differ in the allo cation of the SLF b et ween DLF and non-DLF as shown in Figure 6 . It is imp ortant to note that these designs should b e interpreted as transitional. While harmonised h ydrogen Net work Co des are expected to emerge as the mark et matures, current approac hes reflect early mark et conditions and are therefore likely to evolv e. The German W asABI consultation prop oses a fully non-DLF balancing regime, aligned with natural gas mark et design. Like in natural gas mark ets, the system is organised into balancing zones with an accum ulated system balance represen ting the aggregate im balance of all netw ork users. This v alue is contin uously calculated and published at least every 15 minutes ( Bundesnetzagentur , 2024b ). The framework adopts the familiar green, yello w, and red zone structure. In the green zone, system conditions are stable, and no balancing actions are required. In the y ellow zone, the system enters a critical state, and the help er-causer mechanism is activ ated: net w ork users whose im balance has the same sign as the system imbalance are classified as causers, while those with an opp osite sign are help ers. In the red zone, system conditions b ecome critical and require immediate TSO interv ention. This may include the pro curemen t of balancing energy or the use of non-commercial measures. When balancing energy is pro cured, costs are allo cated to the causers based on their contribution to the im balance. If balancing energy is not pro cured, p enalties are calculated using the EEX HYDRIX index ( EEX , 2026 ), which aims to represen t the wholesale h ydrogen price in German y . As the hydrogen mark et dev elops, the index is exp ected to improv e as mark et liquidity increases. Penalt y rev enues are redistributed to help ers. The Danish TSO has prop osed a hybrid balancing mo del combining DLF and Non-DLF ele- men ts ( Energinet , 2024 ). In the hybrid design, total system linepack flexibilit y consists of a DLF p ortion and a shared Non-DLF p ortion. The DLF share is allocated to shippers on a pro rata basis, prop ortional to b o ok ed capacity . F or example, a shipp er holding 10% of total capacity receives ac- cess to 10% of the av ailable DLF. Shippers are allow ed to main tain an imbalanced p ortfolio position 12 within this allo cated flexibilit y without incurring p enalties. DLF is also exp ected to b e tradable b et w een users, enabling mark et-based reallo cation of flexibilit y . The remaining SLF forms a shared Non-DLF p ortion. If multiple users exceed their individual DLF allo cations in the same direction, the accumulated system balance approac hes the b oundary of the total DLF range. Before the re- serv e linepack is reached and TSO interv ention b ecomes necessary , the Non-DLF p ortion provides additional buffer at the system lev el. If the accum ulated system balance exceeds the o verall SLF limits, balancing actions are triggered, and the use rs con tributing to the im balance are classified as causers and b ear the asso ciated costs. The Danish TSO noted that at the time of writing, their final c hoice b et ween a hybrid approac h and a full DLF regime has not yet b een made. The Dutc h h ydrogen net w ork proposes a balancing regime based fully on DLF ( Gasunie Nether- lands , 2026 ). As previously men tioned, under this approach, system linepack flexibilit y is allo cated to individual netw ork users, allowing them to maintain im balances within their designated flexi- bilit y range without immediate balancing consequences. Dutch TSO indicates that this design is in tended for the initial phase of net work dev elopment, when the hydrogen system is not yet fully in terconnected and market liquidity remains limited. In later stages, once the netw ork b ecomes more in tegrated, the system is expected to transition to ward a Non-DLF regime based on balancing zones, similar to those used in natural gas mark ets. In conclusion, the three approac hes reflect different trade-offs b et ween individual flexibilit y and collective buffer capacity . F ull DLF maximises individual shipp er flexibilit y but offers no collectiv e buffer b efore reserve linepac k is reached. The hybrid approac h adds a shared buffer at the cost of smaller individual allo cations and is harder to op erate in illiquid markets. Non-DLF is op erationally familiar from gas markets but places immediate balancing resp onsibilit y on shipp ers. Hydrogen balancing is not y et regulated at EU lev el, hence curren t prop osed frameworks, e.g. full-DLF approach, are member-state designs and may differ in implemen tation even where similar principles are adopted. Within-da y obligations are implemen ted through frequent system up dates and flexible nomi- nation pro cesses. In German y , 15-minute balance updates pro vide contin uous adjustmen t signals. In Denmark, within-da y balancing is enabled through renomination cycles aligned with 15-min ute mark et interv als. The Dutch prop osal do es not yet define detailed WDO pro cedures. 4. Challenges for the design of future h ydrogen mark ets The second output of this study identifies seven challenges relev an t to early hydrogen market dev elopment, grouped into op erational and regulatory categories. Op erational c hallenges include a supply-demand mismatch, limited initial storage, a fragmen ted net work, and limited linepac k flexibilit y . Regulatory challenges in v olved regulatory uncertaint y , a lac k of harmonised hydrogen qualit y standards, and insufficien t cross-b order co ordination. The identified challenges dra w from t wo sources: those that emerged directly from survey questions, and those that emerged across other sections of the surv ey during broader TSO discussions. F or each c hallenge, participating TSOs pro vided con textual information to supp ort a more precise c haracterisation, whic h directly informed the subsequent risk assessment. The impact and lik eliho o d ratings assigned to each c hallenge reflect the conditions and circumstances describ ed by the TSOs. Figure 7 organises eac h c hallenge by risk level, mapp ed by impact severit y and likelihoo d of o ccurrence. The most pressing op erational challenge is a temp or al mismatch b etwe en supply and demand . In natural gas systems, supply is largely dispatchable, and demand generally follows seasonal cycles. Instead, with h ydrogen this structure is in verted. Consumption from sectors suc h as steelmaking, chemicals, and fuel pro duction is relatively stable and contin uous, while supply is inheren tly v olatile, driv en b y the intermitten t nature of renewable generation rather than op erator dispatc h. The result is a supply and a demand curve with a structural mismatch that could in terfere with the normal system operations. The absenc e of lar ge-sc ale stor age contracted at the 13 Ra m b oll 1 L ike liho o d Low M e d i u m Hig h Low M e d i u m Hi g h Im p act L egen d 1 2 3 4 6 7 1. Su p p l y - d e m a n d m i s m a tc h 2. Ab s e n c e o f s to ra g e 3. Fra g m e n te d n e tw o rk 4. L i m i te d l i n e p a c k fl e x i b i l i ty 5. Reg u l a to ry u n c e rta i n ty 6. Hy d ro g e n q u a l i ty s ta n d a rd s 7. Cros s - b o rd e r c o o rd i n a ti o n Reg ul a tory c ha ll e ng e s 5 O pe rati on a l c ha ll e ng e s Figure 7: Risk matrix for hydrogen market c hallenges. TSO-lev el amplifies the previous risk. Without it, system-level balancing relies mainly on pip eline linepac k. Although ad ho c prop osals exist to allo cate linepack flexibility among users ( Energinet , 2024 ), av ailable linepack is exp ected to remain limited in early mark et phases. Some TSOs rep ort activ e developmen t of salt cav ern storage, but high capital costs and limited geological a v ailability constrain its deploymen t. F urthermore, early h ydrogen netw orks are exp ected to be fr agmente d networks organised into regional clusters, each functioning as an indep enden t balancing zone with limited cross-b order in terconnection. This results in low liquidity and a small participant base, complicating efficient op eration. While the Europ ean Hydrogen Backbone aims to interconnect these clusters o ver time, the transition perio d poses the challenge of net works op erating in isolation. Finally , limite d linep ack flexibility amplifies the three challenges described ab ov e. Linepack capacit y dep ends on b oth the gas energy conten t and the pressure range a v ailable in the pip eline. Hydrogen has a v olumetric energy density approximately a fourth that of natural gas, meaning the same pip eline v olume stores substan tially less energy . Combined with the limited pip eline volumes exp ected in the early stages of hydrogen netw ork dev elopment, this lea v es little buffer to absorb supply fluctuations, hence increasing reliance on demand resp onse, dedicated lo cal storage, or in the w orst case, curtailment. R e gulatory unc ertainty is rated among the most pressing challenges. Mark et participants must commit to long-term infrastructure inv estments without finalised Netw ork Co des for hydrogen and without completed EU-lev el transp osition of the Hydrogen and Decarb onised Gas Mark et P ack- age. This uncertaint y directly negatively impacts the bank abilit y of h ydrogen pro jects and ma y defer inv estmen t at a critical stage of mark et developmen t. A further challenge concerns hydr o gen quality standar ds . TSOs require h ydrogen to comply with stringen t purit y sp ecifications. Once h ydrogen with a non-compliant comp osition enters a shared netw ork, its comp osition cannot b e corrected do wnstream: it propagates through the system and may affect end users and inter- connected net works in neighbouring countries. The absence of harmonised cross-b order qualit y standards, therefore, introduces significant op erational challenges across op erating areas and tec h- nical barriers to trade. Finally , cr oss-b or der c o or dination is closely linked to the t wo preceding c hallenges. In the absence of agreed netw ork co des, TSOs are currently adopting ad ho c measures co vering e.g. balancing regimes, nomination pro cedures, capacity allo cation mec hanisms. While suc h arrangements enable early net work op eration ahead of EU regulation, divergen t approac hes 14 risk creating friction up on interconnection, when misaligned regulatory timelines and inconsistent op erational pro cedures ma y imp ede cross-b order flows. EU-lev el harmonisation of netw ork co des, therefore, remains essential to supp ort infrastructure developmen t at the scale required to meet 2030 and 2040 h ydrogen targets. 5. Discussion 5.1. Conclusions This study examined how the foundational elements of h ydrogen mark et design should be structured, and the challenges they m ust address, with the explicit aim of informing ENNOH’s dev elopment of h ydrogen Net w ork Co des. Through structured consultation with seven Europ ean gas TSOs represen ting six coun tries, tw o outputs w ere pro duced: a mapping of how existing gas mark et design comp onents could b e adapted across fiv e regulatory areas (Figure 3 ), and an iden tification of challenges that early hydrogen mark et design must account for (Figure 7 ). Regarding transferability from natural gas markets, foundational market principles and the trading framework are found to b e broadly transferable (Figure 3 , columns 1 and 2). Entry-exit systems and virtual trading p oin ts, as established under Regulation 2024/1789, attracted consen- sus for direct adoption. T rading is exp ected to evolv e from bilateral ov er-the-coun ter contracts to organised exc hange trading as liquidit y matures. One minor c hange is noted: aligning the hydrogen trading day and gas year with the calendar year to impro ve co ordination with sp ot electricity mar- k ets and facilitate h ydrogen coupling with renew able generation. The transferability of the three net work co des examined v aries substantially . Survey topics in NC CAM are considered replicable with limited mo dification, though capacit y pro ducts are exp ected to shift from auctions tow ard first-come, first-served allo cation dep ending on country-specific market conditions. Gate closure times are also lik ely to b e revised to impro ve alignmen t with electricit y spot mark et sc heduling. F or the section on NC T AR, it is required a more fundamen tal reform: intertemporal cost allo cation, where infrastructure costs are spread ov er time to a void concen trating financial exp osure on early adopters, is exp ected to replace con ven tional tariff-setting, a direction endorsed by A CER. Finally , the survey section on NC BAL presen ted a ma jor deviation: with the hydrogen balancing co de y et to b e published, TSOs are developing country-specific ad ho c strategies. A structural differ- ence is already emerging b et w een those adopting a DLF approac h and those op erating without it, reflecting differences in net work top ology , maturity , and regulatory context. The c hallenges iden tified through the surv ey fall into tw o categories: op erational and regulatory (Figure 7 ). Among op erational c hallenges, the most critical concerns the structural inv ersion of the supply-demand relationship relativ e to gas. In natural gas systems, a largely dispatchable supply resp onds to predictable, seasonally driven demand. In contrast, hydrogen systems are c haracterised b y a more v ariable supply , dep endent on the renewable energy pro duction, while industrial demand is exp ected to b e relatively stable. Pip eline linepack alone is probably insufficien t to bridge this gap, emphasising the imp ortance of storage infrastructure for maintaining op erational stabilit y . Net work fragmen tation amplifies this risk: early infrastructure is exp ected to develop as isolated regional clusters with limited interconnection, thin liquidit y , and few participan ts. As these clusters in terconnect, market depth will impro v e, but the transition p erio d will require careful regulatory o versigh t. Among regulatory challenges, large uncertaint y is the dominant concern: without comprehensiv e framew orks, it is difficult for market participants to commit to long-term in vestmen ts under incomplete rules ahead of the publication of the official Hydrogen Netw ork Co des. T ak en together, these findings indicate that hydrogen mark et design cannot simply replicate the natural gas one. Selective and targeted adaptation is both necessary and feasible, but success dep ends on addressing future op erational and regulatory challenges b efore early markets reach 15 op erational scale. The timing of these c hoices is relev an t with a historical p ersp ective. Euro- p ean natural gas markets initially evolv ed under vertically integrated structures, with comp etitiv e framew orks emerging only after successive EU lib eralisation pack ages. By con trast, the EU Gas and Hydrogen Pac k age establishes a regulatory framew ork for h ydrogen from day one. As h ydrogen mark ets will therefore b e regulated from the start, this study aims to inform these early design decisions. 5.2. Limitations and F urther Work The findings of this study should b e interpreted with consideration of the follo wing limitations. The main limitation is that the survey captures only the TSO p ersp ectives. Although TSOs pro vide essential infrastructure and op erational insigh t, final authorit y o ver h ydrogen net work codes lies with ENNOH under ACER supervision, and TSOs represen t only one stakeholder group across the hydrogen supply chain. A more complete assessment would incorp orate p ersp ectiv es from h ydrogen pro ducers, traders, industrial consumers, and national regulatory authorities. F uture w ork could therefore extend stak eholder engagement to these groups to provide a broader basis for net w ork co de developmen t. Second, although resp onden ts accoun t for appro ximately 45% of the planned Europ ean hydrogen pip eline length, only 7 of 43 TSOs participated, resulting in a 16% resp onse rate concen trated in W estern, Northern, and Central Europ e. Southern and Eastern Europ ean p erspectives are absen t, introducing geographic and regulatory bias. Broadening the TSO sample in future work would improv e the representativ eness and robustness of the findings. Finally , the analysis necessarily fo cuses on market design mechanisms for a hydrogen netw ork that remains largely undev elop ed. The findings therefore rely on assumptions about how infrastructure, liquidit y , and regulatory framew orks will evolv e. As h ydrogen pipelines are commissioned and early trading activity emerges, these design choices will become empirically testable and can b e refined accordingly . 16 CRediT authorship con tribution statement Marco Saretta : Conceptualization, Metho dology , Inv estigation, Data curation, F ormal anal- ysis, Visualization, Softw are, Pro ject administration, W riting - original draft. Enrica Raheli : Sup ervision, W riting – review and editing. Jalal Kazemp our : Sup ervision, W riting – review and editing. Declaration of comp eting interest The authors declare that they ha ve no known comp eting financial in terests or p ersonal rela- tionships that could ha ve app eared to influence the w ork rep orted in this pap er. Ac kno wledgmen ts This work is conducted as part of the Industrial PhD programme “Commo ditizing green hy- drogen in Europ e: from efficien t mark et design to optimal contracting and inv estment”, funded by Inno v ation F und Denmark, Ram b oll F onden, and Ramboll Denmark A/S. The authors express their gratitude to all EU gas TSOs that participated in this initiative and the surv ey . Sp ecial thanks to Christian Rutherford from the Danish TSO for his thorough discussions, constructiv e feedback, and final review of the manuscript. F urthermore, the authors ac knowledge the feedback pro vided at the Lo yola Autumn Research Sc ho ol 2025, organised b y the Florence Sc ho ol of Regulation, for its role in reviewing and enhancing this pap er, significantly refining the p olicy messages. Sincere thanks also go to Alexandra L ¨ uth and Andrea Saretta from Ramboll Denmark for feedbac k and help with reviewing the draft; to Miguel Martinez Ro driguez from ACER for his significan t contributions in reviewing and providing v aluable feedbac k on this w ork; and to Mirco Dain for help with soft ware curation and data collection. Data av ailabilit y The survey data that supp ort the findings of this study are av ailable from the corresp onding author upon request. Co de and supplementary material are publicly a v ailable at Marco Saretta ( 2025 ). Declaration of generativ e AI and AI-assisted tec hnologies in the writing pro cess During the preparation of this work the authors used generativ e AI mo dels by Op enAI and An thropic for translation of original sources and for grammatical revisions. After using this to ol, the authors thoroughly reviewed and edited all outputs and take full resp onsibilit y for the presen ted con tent of the published article. 17 References A CER, 2025a. ACER Public consultation on inter-temporal cost allo cation mechanisms for financing hydrogen infrastructure. T ec hnical Rep ort. URL: https://www.acer.europa.eu/documents/public- consultations/ pc2025g01- public- consultation- inter- temporal- cost- allocation- mechanisms- financing- hydrogen- infrastructure . A CER, 2025b. ACER Recommendation on in ter-temp oral cost-allocation. T ec hnical Rep ort. Bundesnetzagen tur, 2024a. Grand Ruling Chamber for Energy on decision [GBK-24-01-2#1] (W AND A) . Bundesnetzagen tur, 2024b. Second consultation in the determination proceedings for a basic compensation and balancing mo del for hydrogen (“W asABi”) . Bundesnetzagen tur, 2024c. Second consultation in the determination pro ceedings on a basic mo del for hydrogen capacit y and managing netw ork access (”W aKandA”) . EEX, 2026. HYDRIX: First market-based index for hydrogen. URL: https://www.eex.com/en/markets/hydrogen . Energinet, 2024. Proposal on balancing the Danish h ydrogen transmission net work. T echnical Report. URL: https:// energinet.dk/media/a4gdh34h/proposal- on- balancing- the- danish- hydrogen- transmission- network.pdf . ENTSOE, 2023. Pro cess for developing netw ork co des and amendmen ts to net work co des and guidelines. T ec hnical Rep ort. URL: www.entsoe.eu . ENTSOG, 2017. Capacity Allo cation Mechanisms Netw ork Co de. T ec hnical Rep ort. ENTSOG, 2018a. Balancing Netw ork Code – An Overview. T echnical Rep ort. ENTSOG, 2018b. T ariff Netw ork Co de – An Overview. T ec hnical Rep ort. ENTSOG, GIE, EUROGAS, GEODE, GD4S, CEDEC, . Hydrogen Infrastructure Map. URL: https://www. h2inframap.eu/#map . Europ ean Commission, 2025. Hydrogen and decarb onised gas market. URL: https://energy.ec.europa.eu/ topics/markets- and- consumers/hydrogen- and- decarbonised- gas- market_en . Europ ean Hydrogen Backbone, 2024. European Hydrogen Backbone: Bo osting EU Resilience and Comp etitiv eness. Europ ean Hydrogen Backbone: Boosting EU Resilience and Comp etitiveness. T ec hnical Rep ort. Europ ean Hydrogen Observ atory , 2025. EU Hydrogen Strategy under the EU Green Deal. URL: https: //observatory.clean- hydrogen.europa.eu/eu- policy/eu- hydrogen- strategy- under- eu- green- deal#: ~ : text=The%20target%20is%2040%20GW . Europ ean Parliamen t, 2023. Delegated Regulation (EU) 2023/1184 of 10 F ebruary 2023 supplementing Directive (EU) 2018/2001 of the Europ ean Parliamen t and of the Council b y establishing a Union metho dology setting out detailed rules for the pro duction of renew able liquid and gaseous transp ort fuels of non-biological origin. T echnical Rep ort. URL: https://eur- lex.europa.eu/eli/reg_del/2023/1184/oj/eng . Europ ean P arliament, 2024. Regulation on the internal mark ets for renewable gas, natural gas and hydrogen, . URL: https://eur- lex.europa.eu/legal- content/EN/TXT/?uri=CELEX%3A32024R1789 . F raile, D., Muron, M., Pa w elec, G., Santos, S., Staudenma yer, O., 2025. Clean Hydrogen Monitor 2025. T ec hnical Rep ort. Hydrogen Europ e. URL: https://hydrogeneurope.eu/wp- content/uploads/2025/09/Clean_Hydrogen_ Monitor_09- 2025_DIGITAL.pdf . Gasunie Netherlands, 2026. Hynetw ork T erms and Conditions. URL: https://www.hynetwork.nl/zakelijk/ klant- worden/contracten . Johnson, N., Liebreich, M., Kammen, D.M., Ekins, P ., McKenna, R., Staffell, I., 2025. Realistic roles for hydrogen in the future energy transition. Nature Reviews Clean T echnology 2025 1:5 1, 351–371. URL: https://www.nature. com/articles/s44359- 025- 00050- 4 , doi: 10.1038/s44359- 025- 00050- 4 . Klima Energi og F orsyningsministeriet, 2025. Brintinfrastruktur til tyskland: muliggørelse af syvtallet. T echnical Rep ort. URL: https://www.kefm.dk/Media/638744580036601360/Aftale%20om%20brintinfrastruktur%20til% 20Tyskland_muligg%C3%B8relse%20af%20Syvtallet.pdf . Lagioia, G., Spinelli, M.P ., Amicarelli, V., 2023. Blue and green hydrogen energy to meet Europ ean Union decarb on- isation ob jectiv es. An ov erview of p ersp ectiv es and the current state of affairs. International Journal of Hydrogen Energy 48, 1304–1322. URL: https://www.sciencedirect.com/science/article/abs/pii/S0360319922046675 , doi: 10.1016/J.IJHYDENE.2022.10.044 . Marco Saretta, 2025. Designing Europ ean Hydrogen Markets. GitHub rep ository. URL: https://github.com/ marco- saretta/hydrogen- market- design . Martinez-Ro driguez, M., Chy ong, C.K., Fitzgerald, T., V azquez, M., Hidalgo, A., 2026. Pip eline regulation for h ydro- gen: c ho osing b etw een paths and netw orks. Energy Policy 208, 114846. URL: https://www.sciencedirect.com/ science/article/pii/S0301421525003532?ref=pdf_download&fr=RR- 2&rr=9ba3ed790885ed4f , doi: 10.1016/J. ENPOL.2025.114846 . Neumann, F., Zeyen, E., Victoria, M., Brown, T., 2023. The p otential role of a hydrogen netw ork in Europ e. Joule 7, 1793–1817. URL: https://www.cell.com/action/showFullText?pii=S2542435123002660https://www.cell. com/action/showAbstract?pii=S2542435123002660https://www.cell.com/joule/abstract/S2542- 4351(23) 00266- 0 , doi: 10.1016/J.JOULE.2023.06.016/ASSET/66A7C216- C041- 4A9B- B0CC- DB2B9414FD73/MAIN.ASSETS/ GR5.JPG . Niedrig, N.., Giehl, J.., Jahnke, P .., M ¨ uller-Kirc henbauer, J., 2024. Mark et Design Options for a Hydrogen Market . 18 Sargen t, P ., Sargent, M., 2025. Linepac k flexibilit y for hydrogen and natural gas pip es: A new flexibility metric for energy systems mo delling. International Journal of Hydrogen Energy 132, 139–142. URL: https://www. sciencedirect.com/science/article/abs/pii/S0360319925018543 , doi: 10.1016/J.IJHYDENE.2025.04.197 . Shen, J., Zhang, Q., Tian, S., Li, X., Liu, J., Tian, J., 2024. The role of hydrogen in iron and steel pro duction: Dev elopment trends, decarbonization potentials, and economic impacts. In ternational Journal of Hydrogen Energy 92, 1409–1422. URL: https://www.sciencedirect.com/science/article/abs/pii/S0360319924045798 , doi: 10. 1016/J.IJHYDENE.2024.10.368 . Stein bach, S.A., Bunk, N., 2024. The future Europ ean h ydrogen market: Market design and policy recommendations to supp ort market developmen t and commodity trading. International Journal of Hydrogen Energy 70, 29–38. doi: 10.1016/j.ijhydene.2024.05.107 . 19 App endix A. TSO Hydrogen Survey App endix A.1. Survey administr ation The 37-question surv ey w as structured around fiv e comp onen ts derived from EU gas mark et regulation: (A) market and regulatory design principles from Regulation 2024/1789, (B) trading framew ork, (C) Netw ork Co de on Capacit y Allo cation Mec hanisms (NC CAM), (D) Net w ork Co de on T ariffs (NC T AR), and (E) Netw ork Co de on Balancing (NC BAL). Questions used a mix of op en-ended and y es/no formats to capture detailed qualitativ e reasoning. The survey w as pilot- tested with the Danish TSO under agreement, in August 2024 and administered b et w een September 2024 and Jan uary 2025. All Europ ean gas TSOs were iden tified through the ENTSOG member directory . F rom this set, priority was given to op erators in coun tries with national h ydrogen strategies or announced h ydrogen infrastructure plans, to capture p ersp ectiv es from TSOs actively engaged in hydrogen net work developmen t. These TSOs were then con tacted b etw een Septem b er 2024 and Jan uary 2025. Initial contact was primarily established via official email addresses listed on TSO websites or through institutional contact p ortals. In some cases, contact details w ere obtained through professional referrals from colleagues at other TSOs. The surv ey was distributed in Excel format with an estimated completion time of 45–90 minutes. Resp onden ts returned completed questionnaires via email. Where resp onses required clarification or additional con text, follow-up discussions were conducted through video call on Microsoft T eams to complemen t the written answers. Sev en TSOs from six countries pro vided complete resp onses: Belgium, Denmark, F rance, Ger- man y , Lithuania, and the Netherlands. Excluding non-resp onses and declined participation, this corresp onds to appro ximately 16% of the identified TSO set. Participating countries accoun t for around 45% of the planned Europ ean hydr ogen pip eline length by 2040 according to European Hy- drogen Backbone data ( ENTSOG et al. ). Respondents held p ositions in op erations management, strategic planning, and regulatory affairs. Anonymit y was granted b oth to the TSO organisations and individual participants, who were anonymised, with results rep orted only at the coun try level. App endix A.2. Survey questions 20 T able A.2: Complete survey distributed for TSO consultations on hydrogen mark et design. ID Question A. Market and Regulatory Design (10 questions) A.1 Who is the regulating authority in your country? A.2 Do y ou hav e a regulation scheme in place? If so, when is it exp ected to b e implemen ted? A.3 Will the en try/exit p oint scheme b e maintained in the hydrogen mark et? A.4 Will the gas day and gas year structure b e kept for hydrogen? A.5 Ho w will the shipp er roles evolv e, esp ecially at early market stages with low er liquidity? A.6 In y our country , how w ould you exp ect the hydrogen generation to b e? Green, blue, or gray? A.7 Ho w will Guarantees of Origin play a role with RFNBO requirements? A.8 What tec hnical and regulatory challenges of the new h ydrogen economy are sp ecific to your TSO’s coun try? A.9 What is the hydrogen strategy for the new hydrogen economy in y our TSO’s country? A.10 What are the expectations regarding interaction with TSOs within the same coun try and neighbouring coun tries? A.11 Which role will DSOs pla y at the early market stage, giv en the large industrial nature of H 2 off-tak ers? A.12 What in your opinion has the most urgent requirement to b e developed? A.13 If you had time to do research, what would b e some challenges that you wish y ou could solve for future h ydrogen markets? B. T rading F ramew ork (7 questions) B.1 Should w e exp ect an exchange for H 2 (lik e ICE)? B.2 Should w e exp ect a virtual trading hub for H 2 (lik e TTF)? B.3 Should w e exp ect H 2 to b e traded at exchanges, via OTC trades, or b oth, as in natural gas? B.4 Ho w will the price formation mechanism function? B.5 Ho w correlated will hydrogen prices and electricity prices b e? B.6 Whic h role will deriv ative contracts (futures, forwards, PP As) play in electricit y provision and hydrogen in take? B.7 What will b e the impact of CO 2 quotas? C. Netw ork Co de on Capacity Allo cation Mechanisms (NC CAM) (7 questions) C.1 Will the scheme of nominations, re-nomination, and allocations b e kept for hydrogen net works? C.2 Ho w will the gate closure time for nomination submissions in the gas day b e affected? C.3 Will the capacity products differ from natural gas mark ets (e.g., yearly , quarterly , monthly , daily , in traday)? C.4 What is the reasoning b ehind the capacity pro ducts you offer? C.5 Ho w muc h capacity is expected to b e av ailable in the early stages? C.6 Ho w and when are you scheduled to go live with the capacit y? C.7 Will the TSO assign capacity with mec hanisms different from ascending clo ck auctions? D. Netw ork Co de on T ariffs (NC T AR) (2 questions) D.1 Ho w will the capacity base price and premium b e decided? (System tariffs) D.2 Will the current congestion managemen t system need adjustments for hydrogen? E. Netw ork Co de on Balancing (NC BAL) (8 questions) E.1 Do y ou hav e a netw ork co de on balancing which will gov ern the framework for the balancing mo del? E.2 Ho w will the hydrogen target balancing mo del differ from the natural gas one? E.3 What is the exp ected role of linepack in h ydrogen markets? Can y ou quantify it? E.4 Will the determination metho dology for green, yello w, and red zones b e adjusted in the future H 2 mark et? E.5 Ho w will contin uous balancing work for hydrogen markets? E.6 Ho w can the duality b etw een storage needs and the lack of av ailability at early market stages be addressed? E.7 Ho w will shipp ers b e incentivized to main tain an optimal balance in the netw ork? E.8 Ho w will shipp ers deal with v ariable supply and constant offtak e? 21

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment