Adapting Altman's bankruptcy prediction model to the compositional data methodology

Using standard financial ratios as variables in statistical analyses has been related to several serious problems, such as extreme outliers, asymmetry, non-normality, and non-linearity. The compositional-data methodology has been successfully applied…

Authors: Fatemeh Keivani, Germà Coenders, Geòrgia Escaramís

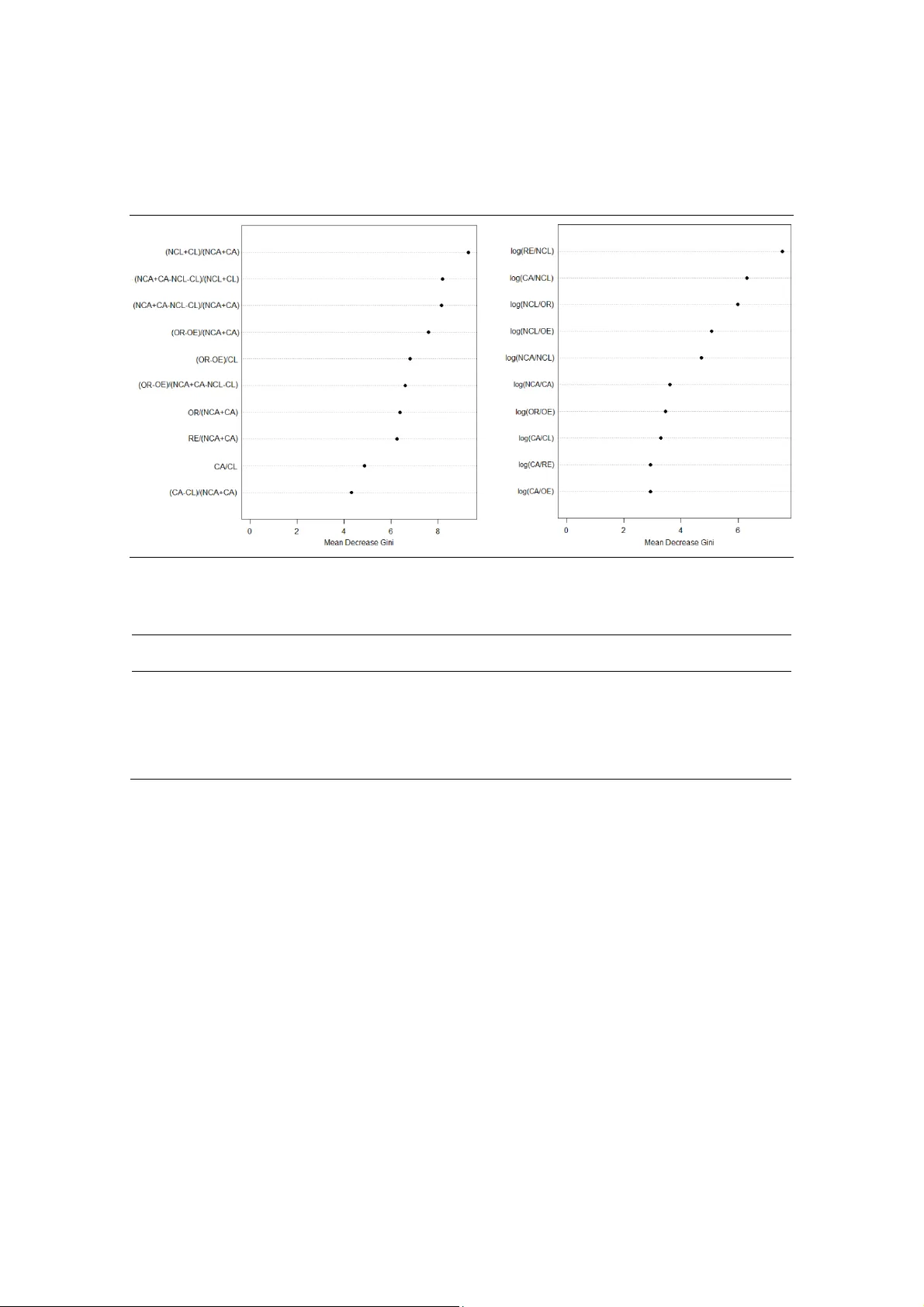

Adapti ng A ltman’ s bankruptcy pre dictio n model to the co mp os it i on a l d at a met h odo log y Fatemeh Keivani , Germ à C o enders * , Ge ò rgia Escaram ís Univer sitat de Gir ona, department of economics, Girona, Spa in March 2026 Abstract : Using standar d financial rati os as vari ab les in stati stical analy ses has been relat ed to several serious problems , suc h as extreme outliers, asymmetry , non - normali ty , and non- linearity . The compositional - data method ology has been successfully applied to solve thes e problems and has always yielded substantially different results when compar ed to standard finan cial rat ios. An under - researched area i s the use of fin ancial log- ratios computed with the compositional - data methodology to predict bankruptcy or the related terms o f bus iness de f ault, insolvenc y or failur e. Anothe r under - r esearched area is the use of machine learning methods i n combination with c ompositional log- ratios. The present art icle adapt s t he cla ssical Altma n bankruptcy pr ediction model and some of its extensions to the compos itional methodology with pairwis e log - ratios and thr ee common statis tical and machin e learning too ls : logistic r eg ression mode ls , k- nearest neighbours , and random forests , and compa res the results wit h standard financial ratios . Data f rom the sector in the Spanish e conomy with the larges t number of bankrupt fi rms according to the first two d igits of the NACE code (46XX “wholes ale tr ade, except of m otor vehicle s and mot orcycl es”) were o btained f ro m the I berian Balance sh eet Anal ysis System . The sample s ize (31,131 f irms, of w hich 9 7 were bankr upt) was d ivided into a training and a validation d atas et. The training data se t was downs ampled to one healthy fir m to each bankrupt fir m . No outliers were removed. Focusing on predictive performance, t he resu lt s show that compos itional methods are better than standard ratios in te rms of se nsitivity , with mixed res ul ts regarding specificity , compos itional random for ests a nd compositional logistic regression beha ving the best. Keyword s : Artificia l in telligenc e, da ta mining, big data, accounting ratios, log it mo dels, credit scoring, CoDa , SABI. JEL codes: C25, C45, C46, G32, G33, M41 . MSC cod es: 62H30, 62J12, 62P05 , 68 T 99. * Corresponding author: ge rma.coenders@udg.edu Keiv ani el al. ( 2026 ) , arX iv . 2 Intr oduction Using s tandard financial ratios as variables in statistic al models h as been relat ed to sever e violations of the models’ assumptions , such as extr em e outli ers , asymmet ry , connect ed to it sever e non -normality of the distributions, non- li nearity of the relationships, and even dependence of the results on the arbitrary decisio n regarding which accounting figure appears in the nu merator and which in the deno minator of the ratio ( Carre ras - Simó & Coenders, 2021; Coenders & Arimany - Se rrat, in press ; Durana et al . , 2025; I otti et al., 2024; L inar es - Mustarós e t al., 2018; 2022; Magrini , 2025 ) . The results of many sta tistical and machine learning analyses are in valid when all or some of these problems occur and the r esults and conclusions of said analyses can be affected to a great extent. T h e well - known Compositional Data ( CoDa) methodol ogy using log - ratio tr ans f ormations (Aitchison, 198 2 ; 1986; Coenders et al., 2023 a ; Gre en acre et al., 2023 ; Pawlowsky -Glahn et al., 2015 ) has been successf ul ly applied in connection with financial ratios over the l ast 10 years, to solve these problems ( Coenders, 2025; Coe nders & Arimany - Serrat, 2025; i n pr ess). This methodology was developed to deal with fixed - sum data in chemical and geological analys is, but the fixed sum is by no m eans ess ential. CoDa are contemp orar ily defined as arrays o f strictly positive numbers for which ratios between them a re considered to be relevant ( E gozcue & Pawlowsky - G lahn, 2019) , which pe r fectly fits the notion of f inancia l state ment analysis . Far from be ing a statistical re finement, the CoDa methodology leads to very subs tantial differ ences in the analysis resul ts whenever it has been compar ed wit h s t andard fin ancial ratios (Arimany - S errat et al., 2022; Carrer as - S im ó & Coenders, 2021; Coende rs & Arimany - Serrat, 2025 ; i n pre ss; Coenders et al ., 2023b; Creixans - T enas et al . , 2019; Dao et al., 2024; Escar amís & Arbussà , 2025; Her nandez - Romero & Coende r s, in press; Jo fre - Campuzano & Coenders, 2022; L inares - Must arós et al. , 2018; 2022; Magrini, 2025 ; Mola s - Colomer et al., 2024 ). An under - researched ar ea is that of the use of f inanci al - statement ratio s to predict outcom e variab les (Coenders & Ar imany - Serrat, 2 025 ; Molas - Colomer et al. , 2026 ) such as bankruptcy or the related terms of business defaul t , insolven cy or failur e . The only known ins tance of application o f the C oDa methodology here is that by Ma gr ini (2025 ) both using logistic r egr ession models , LASSO r egularization , an d random fo r ests . Magrini’ s work is also the first to c ombine a f inancial application of the CoDa methodology with machine learning . In bankruptc y prediction studies, p redictive accuracy bec omes a key pa rameter , beside s fulfilment or violation of the as sumptions. Magrini did not find subs tantial differences in a ccuracy betwee n standard and compositional methods. Since the seminal work by Altman (1968) , the proble m of using financial ratios to p redict bankruptcy has never ceased to attract interest ( Hanun & F erdiani, 2025; Insani et al. , 2024; Magrini, 2025; Martin - Melero et al ., 2025; Nugroho & Dewa yanto, 2025; Soukal et al., 2024 ; Staňková & Hampel, 2023; T aoushianis , 2025; V eganzones & S é verin , 2021 ; W iller do Prado et al. , 2016 ). The o riginal Altman’ s model and s ome popular vari ants Keiv ani el al. ( 2026 ) , arX iv . 3 continue to be used a nd a dapted to new machine le arning tools , a. k.a . statis tical learning , data mining , a n d artific ial intelligen ce tools (M arti n - Meler o et al., 202 5). T he literature on bankruptcy prediction with machine learning methods is growing apace ( Akusta & Gün, 2025; Antar et al., 2025; Anta r & T aya chi, 2025; Asif et al., 2025; Bal zano & Magrini, 2025; Chan et al . , 2025; Chen et a l., 20 25; Chohan et al., 2026; Cojocaru, & Ionescu, 2025; Dam & Nghiem, 2026; Dumitresc u et al., 2025; Gabrielli e t al., 2026; Gajdosikova et a l., 2026; Gnip et al., 2025; Gwalani et al . , 2025; Hussain et al., 2026; Kanojia & Arora , 2025; Khotimah & W anti W idodo, 2026; Kristanti et al., 2025; Lin et al., 2025; Liu , 2025 a ; L i u et al., 2025; L iu, 202 5b ; Martin - Melero et al., 2025 ; Mat suma ru & Katagiri, 2025; T anaka e t a l., 2025a; 2025b ; T hot a et al., 2026 ; V eganzones et al ., 2026; W ang et al., 2026; X u, 2026; Yu a n , 2025; Zhao, 2025. Zhu et al., 2026 ) . O f ten , eliminating a vast amount o f outliers ( Balza no & Magrini, 202 5 ; Magr i ni, 2025 ) , ev en in t he r ange o f one third o f the or iginal s ample (Martin - Melero et al., 2025) , is the p rice to be paid for using standa rd financial ratios , as some machine learning methods a r e relative ly immune to outliers, but no t all o f them . Machine lear ning t ools can be adapted to the CoDa methodology ( T olosana- Delgad o et al., 2019; T r an, 2025). The present ar ticle compares Altman’ s classical bankruptcy prediction model and some of its extensions with the CoDa methodology an d three common s tatistic al and machine le arning tools : lo gistic reg ress ion models , random fores ts , and k- near est neighbours . Ra ther than focus ing on the violation of the ass umptions, we focus on comparing predictive performance. Our approach complements that of Magrini (2025) , firstly , by using the full s ample without tri mming outlie rs, which is poss i ble in the Co Da methodology , as i t tends t o produce few or no outliers ( L in ar e s - Mustarós et al., 2018 ) . Random forests are relative immune to outliers (Hia et al ., 2023), but logistic regression , being a parametric s tatistical mode l, and k - nearest neighbours , being a distance - based method, are no t . Secondly , by downsampling of healthy firm s , which is known to improve pr edicti ve performance when ther e are f ew bankrupt fir ms ( Antar & T ayachi, 2025; Cojoca ru & I onesc u, 2025; Gabrielli et al . , 2026; Gnip et al., 2025; Kanojia & Aror a, 2025; Liu et al., 2025; Ma rtin - Meler o et al., 2025; T anaka et al., 2025a ; 2025b; V eganzones et al., 2026). T o this end , we randomly select one healthy firm for each bankrupt fi r m in the training sample. T hird l y , by using an alternative log - ratio transformation te rme d pairwis e log -ratios (henceforth plr ; Greenacre, 201 9 ). Materi als and m ethods Standar d and CoDa r epr esentation of Alt man’ s mo del for bankruptcy pr ediction According to Altman (1968 ), the following five s tandard f inancial ratios are good predictors of bankruptcy: working capital ratio: (CA - CL)/ (N CA+CA) , retai ned earni ngs over assets: RE/( NCA+CA), re tur n o n assets: ( OR - OE)/( NCA+CA), (1) net worth ove r liab ilitie s: (NCA+CA - NCL - CL )/( NCL+CL ), turnover: O R /(NCA+CA), Keiv ani el al. ( 2026 ) , arX iv . 4 where NCA stands for non - cur ren t assets, CA f or cur rent assets, RE f or retained earnin gs, NCL for non - current liabilities , CL for current l iabilities, OR f or operating revenue and OE for operating expenses . In the origin al Altman’ s model, the c ompany marke t value is used inste ad of the book value of net worth ( NCA+CA - NCL - CL). The book value is used in this article as commonly d one, being available f or all c om panies, be they traded in the stock excha nge or not. Altman’ s model has been re for mulated m any times. T he mos t popul ar s uch reformul ations are arguably those by Amat el al. (2008) ; G r over and Lavin (2001); Springate (1978) ; and Zmijewski (1983). These formulations add or substitute five more standard finan cial ratios: p rofit ove r curren t liabili ties: (O R- OE) /CL , c urrent ratio: CA/CL, i nver ted lever age ratio : (NCA +CA - NCL - CL)/(NC A+CA), (2) return on equity : (O R- OE )/( NCA+CA - N CL - CL) , indebtedness : ( NCL +CL) /( NCA+CA ). The starting point of the CoDa methodology is not the ratios , but a composition of the D positive accountin g fig ures needed to compute them, which are call ed par ts or components. Positiveness is ess ential. For instanc e, one cannot use operating pro fit (O R- OE) which may be nega t ive, but the always positive operating revenue (O R ) and operat ing exp enses (OE) separatel y (Cr eixans - T enas et al., 2019). In o ur case the D =7 parts in the composition are NCA, CA, RE , NCL, CL , O R and OE. The D p art s ar e then subject to log - r atio transformatio ns that c ontain all the rel ative information among the m (L inar es - Mustarós e t al., 2018; Coenders & Arim any - Serr at, in pr ess). The simples t approach to the C oDa methodology in financial an alysis is transforming the accounting figures by means of plr ( Creix ans - T en as et al., 2019; Coenders & Arimany - Serr at, in press; Farre ras - Nogu er et al . , i n p r e ss ; Greenacre, 20 19 ; Mulet - Fort eza et al., in pr ess ) . This involves d efining D - 1 l o g - ratios be tween only two accounting figures, so that each acc ount ing figure can be connected to any ot her (exhaustiveness) in only one way (non- r edundancy) thr ough the log - ratios. The D - 1=6 plr below follow both rules and can be interpreted according to c ommon financial concepts: ass et tangibility: log(NCA/C A), curr ent - asset turnover: log(O R /CA), margin: log(O R /OE) , current ratio: log(CA/CL), (3) debt maturity: log(NCL/CL), retained earnings over non - c ur rent liabilities: log (RE/NCL ). As recommended by Greena cre (2019), if we d raw a graph in which the accounting figures are the ve rtices (nodes) and the pl r a re the c onnections (edges), it is eas y to see that a n y accounting figure can be joined to any o ther through the plr in only one way , so that t he graph is connected and acyclic. For instance, NCA and O R are connected to each Keiv ani el al. ( 2026 ) , arX iv . 5 other only through the log ( NCA/CA) and log ( OR /CA ) p l r. Edges can be drawn as a rr ows without affecting the graph pr operties, the arrows pointing at the numerator of the plr for clarification purposes. Figure 1. Connected a cyclic graph among the D =7 acc ounting figures D - 1 plr can routinely be us ed as a se t of predicto rs in s tatistical model s , including logistic regression models (Coe nders & Greenacre, 2023; Coenders & Pawlows ky - Glahn, 2020). Furthermor e , the predictions are invar iant to the particu lar cho ice of D - 1 plr , as long as each acc ount ing figure can be c onnected to any other in only one way (Coenders & Pawlowsky - Glahn, 2020). More th an D -1 pl r would le ad to pe r fect collinearity . The distances among companies do depend on the plr choice. Rather th an selecting D - 1 plr , using all the possible D ( D -1)/2 plr is a better option for methods base d on di stance s, such as the k - nearest - neighbour method, because Euclidean distances computed on all the possible D ( D - 1)/2 plr ar e equivalent t o the stan dard d istance measur e for CoDa, term ed Aitchison’s distanc e ( Aitchison, 1983; Aitchis on et al., 2000) . M e thods which have the ability to s elect th e best predictors from a large ava ilable set , such as random forests , will also benefit from us ing all the pos sible D ( D - 1)/2 plr. Besi des, with random forests a nd k - nearest neighbours , t he predictions depend on the plr choice when using only of D - 1 of them , which makes results arbitrary and non - r eplicab le. Which accounting figure goes to the n umerator or the denominator of the plr does not change th e results. In our case, the set of D ( D -1)/2 =21 possible plr is: NCL OR CA NCA log( NCA/CA) RE OE CL log( RE / NCL ) log( NCL / CL ) log( CA / CL ) log(OR/ OE ) log( OR / CA ) Keiv ani el al. ( 2026 ) , arX iv . 6 log(NCA/CA), log (NCA /RE ), log(NCA/NCL ), log (NCA /CL ), log(NCA/O R ), log(NCA/OE ), log (CA/ RE) , log (CA/ NCL ), log (CA/ CL) , log(OR/ CA ), log(CA/OE ), (4) log (RE /NCL ), log( RE /CL ), log(RE/OR ), log(RE/OE), log (NCL /CL ), log(NCL/OR ), log( NCL/OE ), log(CL/OR ), log(CL/OE), log(OR /OE) . Thus, the 10 predictors in Equation s ( 1) and (2) w e re used for the standard - ratio approach under all three prediction methods. The predictors in Equation ( 3) w er e used for logistic regression under the compositional approac h, an d the predictors in Equation (4) were used for random fo r ests and k - nearest neighbours under the compositional approach. Statistic al analys is The logistic regres sion model was fi tted with the gl m function in t he basi s R sof twa re (R core team, 2025). The k - n earest - neighbour class ification was carried out with the knn function, which is part of the class R library ( V enables & Ripley , 2002) by tuning the best k value. T h e r andom- for est classificat ion used t he randomForest function in the homonymous R l ibrary (Breiman, 2001), by gener ating 100 trees a nd randomly selecting 4 predictors in the standard - ratio approac h and 7 in the compositional approach, which is about one third of the 10 standa rd and 21 compos it ional ratios. T he sampl e was randomly divided into a training subset ( 70 % of the sample) and a validation subset to as sess predictive q uality (30 % of the sample) . The training subse t was downs ampled and one hea lthy firm wa s randomly selecte d for each bankrupt firm. The validation subset wa s kept entirel y . Thr ee commo n precision measur es computed from the validation subset are: 1. p r ed ictive accu racy (over all per centage o f correct predi ctions) , 2. sens itivity ( percent age of t r ue bankr upt companies predicted as so), 3. spec ificity ( percen tage of tr ue heal thy com panies predicted as so) , 4. balanced accur acy (arit hmeti c average of sensitiv ity and s pecificity) . Keiv ani el al. ( 2026 ) , arX iv . 7 Data collection and p re -pr ocessing W e def in ed a company as being bankrupt if under cr edit ors’ meeting ( “concurso de acreedor es” in Sp ain). To predict i f a company was bankr upt in the last av ailable y ear , the standard and compos itional ratio values of the year immediat ely before wer e u sed . Data gathering and p r e -processing were as follows : 1. Data fr om the sector in the Spanish economy w ith t he largest number of firms under creditors’ meetings in 2024 accordin g to t he first two digits o f the NACE code (4 6 XX “w holesale t rade, except of mot or vehicles and m otor cycles ” ) were selected. Filt ers incl uded having 5 or more empl oyees and data availabl e until at least 2023 . The data w ere obtained on 6/10/2025 fr o m t h e Iberian Balance sheet Ana lysi s Sy stem ( SA BI , access i ble at ht tps://sabi. bvdinf o. com/) database, developed by INFORMA D&B in collaboration wi th Bureau V an Dijk. 2. The sample size was 31,131 f irms, of which 97 we r e bankrupt. 3. No outliers w ere be remov ed, only inactiv e f ir ms having either zero total assets (NCA+CA) , zer o OR , an d zero OE duri ng the last available year or t he year befor e the last . 4. The r emaini ng zero s w ere imputed with the l og - ratio EM method ( Palar ea - Albalade jo & Martín - Fer nández, 2008) avai lable in the freewar e Co DaPack (Co mas - Cufí and Th ió - Henestrosa, 2 011; downloa dable at https://ima.udg. edu/codapac k/ ). The per centages of zero s were 1. 38 % for NCA , 0.01 % for CA , 5.54 % for RE, 22.58 % for NCL, and 0.05 % f or CL . 5. The sample was randomly divided into a training set (70 % of cases ) and a validation set (30 % of cas es). The tr aining set had 21,791 fi rms, of which 69 wer e bankrupt. T he validation s et had 9, 340 firms, of which 2 8 were bankrupt. T he downsampled training set thus contained 69 healthy and 69 bankrupt firms, and the validation set 9,312 healthy and 28 bankrupt fi r ms. Th e same s et s were used for all three methods bo t h for the stand ard and co mpositional approaches. T able 1 shows the sk ewness and ku rto sis statistics of the s tandard ratios in Equations (1) and (2) , and the plr in Equation (4) f or the full samp le. Sk ewness serves as a measure of asymmetry , and kurtosis as a mea sure of heavy distribution tails, in other words , out liers. A normal distribution uncontaminated by outliers has z ero skewnes s and kurtosis. All standard ratios but one have ve r y high s kewness and extr eme kurtosis , making them o n the paper unfit fo r statis tical modelling and non - robus t machine learning m ethods except after pruning outliers . Pr un ing outliers following the standard criterion ( e. g. , Ma rtin - Melero et al., 2025) of values above the thir d quar tile plus 1.5×( inter quartile range ) or below the firs t quartile minus 1.5×( inte rquartile r ange ) would r esult in dropping 9,544 cas es from the full s ample, which is 3 0. 7 % of the companies , thus s er iously impai ring the sampl e repr esentativen ess. In t he case of p lr , only the margin r atio log(OR /O E) has high kurtosis, but to a much l esse r extent than the standard ratios. The rest of the plr behave w ell. In contrast wi th Magrini (2025), w e analyse the full s ample without pruning outliers. Keiv ani el al. ( 2026 ) , arX iv . 8 T able 1. Skewness and kurt osis of sta ndard ratios and plr in the full sample Sk ewne ss Kurtosis (CA - CL) /( NCA+CA ) -30.3 2220.3 RE/ (NCA +CA) 1.3 4.9 (O R- OE)/( NCA+CA) -23.9 1843.6 (NCA +CA - NCL - CL ) /(N CL+CL ) 129.9 19809.4 OR /(NCA+CA) 63.9 621 1.5 (O R- OE) /CL -167.6 29201.4 CA/CL 167.5 28935.9 (NCA +CA - NCL - CL ) /(N CA+CA) -44.7 3617.9 (O R- OE)/( NCA+CA - NCL - CL) -161.2 27301.5 (NCL +CL )/ (NCA +CA) 44.7 3617.9 log(NCA/CA) -0.9 2.8 log (NCA /RE ) 0.8 2.8 log(NCA/NCL ) 0.7 0.2 log (NCA /CL ) -0.9 2.9 log(NCA/O R) -0.9 3.0 log(NCA/OE ) -0.9 3.1 log( CA/ RE) 1.8 3.4 log (CA/ NCL ) 0.8 -0.4 log (CA/ CL) 0.9 6.3 log(OR/ CA ) -0.2 5.7 log(CA/OE ) 0.1 4.7 log (RE /NCL ) 0.3 0.1 log( RE /CL ) -1.2 2.0 log(RE/OR) -1.4 2.5 log(RE/OE) -1.4 2.5 log (NCL /CL ) -0.8 -0.3 log(NCL/OR) -0.8 -0.3 log(NCL /OE) -0.8 -0.3 log(CL/OR) -0.2 5.2 log(CL/OE) -0.3 6.1 log(OR /OE) -3.8 277.2 R esul ts According to the logistic r egression model with standard ratios , the relevan t predictor s (5% signi ficance) are ( NCA+CA - NCL - CL)/ (NCL +CL), (O R- OE) /C L , and CA/CL but, due to outliers , some p redicted probabilities are numer ically equal to 0 and 1, whic h af fects the r eliability o f pr ecisely the si gnif icance measures . W ith compositio nal ratios , no such problems are enc ount ered, and the rele vant predictors are l o g( OR/ CA) and log (RE /NCL ). T he k - nearest - neighbour method do es not produce any mea sure of variable impor tance. 5 nearest neighbours yie ld the highe st accuracy . The random - fo rest method can assess the im port ance of a predict or by th e mean decrease of Gini’ s impurity if the predictor is removed. The be st standard ratio s are (NCL+ CL)/(N CA+C A), (NCA+CA - NCL - CL) /( NCL +CL) , an d (NCA +CA - NCL - CL) /( NCA+CA), all connected to the br oad concept of long - ter m indeb tedness and lever age, and the best c ompositional ratios are Keiv ani el al. ( 2026 ) , arX iv . 9 log (RE /NCL ), log(CA/NCL ) , and log(NCL/O R) , a l so connec t ed to non - current liabilities and thus to long - term indebtedness. Figure 2. Te n most important predictor s for the random - forest method with standa r d (le ft) and compositional (right) r atios T able 2 . Pr ecision mea sures of the logistic regress i on model, 5- nearest ne ighbours, and the r andom forests with standard and compositional ratios Prediction method Accu r acy Sens itivi ty Spe c if ici ty Bal anced ac cura cy Logistic regressi on (sta ndard ) 66 % 82 % 66 % 74 % Logistic regressi on (c omposi ti o nal) 67 % 86 % 67 % 76 % k- nearest n eighbours (s ta n dard) 70 % 75 % 70 % 73 % k- nearest n eighbours ( c o mpositional ) 58 % 89 % 58 % 74 % Random fores t s (standard) 62 % 75 % 62 % 68 % Random fores t s (composit i on al) 65 % 89 % 65 % 77 % T able 2 contains the precision meas ur es for all app roaches computed from the va l idation set. Compositional methods a lways have highe r sensitivity that thei r standard counterpa rts. Random forests be at them also in spe cificity . Compos itional and standard logistic regression ha ve about the same specificity . Compos itional k - nearest neighbours perform worst in terms of s pecificity . T he overall a ss essment by the balanced accu racy i s that compositional random forests and compositional logistic regres sion perform b est. Disc ussi on Bankruptcy prediction is one of t he most commo n uses of financial ratios and yet a n under- researched area in the CoDa me thodology . This article adapt s Altman’ s prediction model and some of its adaptations to this methodology w ith t hr ee common pr ediction methods, one being a statis t ical model and the remaining two machine - learning method s, and compares the performance of standard and co mpositional financial ratios, computed a s p l r. Keiv ani el al. ( 2026 ) , arX iv . 10 As reported in the literature, the C oDa methodology improves on the skewness and kurtosis of the analysis var iables and outlier pruning, which can improve the fulfilment of statis tical ass umptions bu t can al so affect th e sample rep resentati vity , i s avoided . Unlik e research d one so far with compositional bankruptcy prediction ( Magrini , 2025) , we have us ed the full s ample . The results show that be yond the fu lfilment o r not of sta tistical ass umptions, the comparison between the standard and compositional approach is also a matter of predi ctive per forman ce. C ompos itional methods a r e better in terms of sens itivity , with mixed results regarding specificity , compositiona l random forests and compositional logistic regression beha ving the best. Magrini ( 2025) did not f ind any substa ntial difference betwe en standard and compos itional rat ios for logistic r egression and random fo rest s, but this a uthor pruned the extreme outliers. In spite of their known sens i tivity to outli er s, when it comes to predi ctive per formance, log istic r egression and k nearest neighbours are just mar gi nally wor se fo r the outlier - r ich standard r atios. In spite of their known robustness t o outliers, when it comes to predictive performance, random fo r ests be have much worse for standard ratios. W e ar e of course awar e that th ese findi ngs are no t generalizable beyond this pa r ticular sector of the Spanis h economy an d the par ticul ar accounting figures and r atios chos en . The possibility o f using other log - r atio trans formations than plr deserves a comment . Centred log - ratios a.k.a. clr (Aitchison, 1983) a re coherent with Aitchison’ s distances and therefore can be used f or t h e k - near est - neighbour method with identica l results as the D ( D - 1)/2 plr . The family o f isometric log - rati o transfor matio ns a.k. a. ilr (Egozcue et al., 2003) has the same property : a ny ilr trans formation can be used for the k - n earest - neighbour method with identical res ults as the clr and the D ( D - 1)/2 plr . Any ilr transformation can also be used as p redictor in a lo gistic regres sion model with iden tical for ecasts as the D - 1 plr ( Coenders & Pawlows ky - Glahn, 2020). Tr e e - based methods in general and r andom forests in particula r cons tit ute another story . While t h e i lr family of transformations is a respect able choice (Magrini, 2025) , it m ust be borne in mind that the forecasts depe nd on the particular ilr selected within the fam ily ( T empl & Gonzalez - Rodriguez, 2024 ) , and that any of these forecasts als o differ from those obtained with the D ( D - 1)/2 plr . T he main advantage of plr i s th at t her e is only one way o f selecting all possible D ( D - 1)/2 plr , which makes t he r esults le ss a rbitrar y and always repl icable ( E ngle & Chaput, 2021 ; T olosana- Delgado et al., 2019 ) . O n the contrary , using all possible ilr is generally u nfeasib le. W ith ju st D =7 accou nting fig ures ther e are 1 . 141 distinct balanc es for the ilr transformation and it is easy to imagine what can happen when D is lar ge. clr have also be en used for random forests ( Nathwani et al., 2022), being als o r eplicable, but they yield different r esults from both ilr and plr . T olos ana- Delgado et al. ( 2019) reported su peri or perfo rmanc e of p lr ove r ilr o r clr . Fur ther r esearch can include adapting other machine - learning methods li ke neural networks and deep learning , naï ve B ayes classifi er , partial- lea st - squar es disc riminant analysis (PLS - DA) , s upport vector machines (S VM) , natural gr adi ent boosting (NGBoost), adaptative boosting ( AdaBoos t), cate gorical boosting (CatB oostc lassifier), Keiv ani el al. ( 2026 ) , arX iv . 11 light gradient boosting (lightGBM ) , and extreme gradient boosting (XGBoost) . Th e so - called hybrid models , ens emble methods , or m eta models combine more than one machine - learning approach and are also worth explori ng (Akusta & Gün , 2025; A si f et al., 2025 ; Choha n et al . , 2026; Huss ain et al., 2026 ; Liu , 202 5b ; V eganzones e t al., 2026 ). Each m achine lear ning method can have a differ ent set of compa ti bl e log - ratio transformations within the CoDa methodology an d t his has to be e xpl o r ed in the first place. Besides , each machine lea rning method may be robust to outliers to a dif f erent extent, if at all . Additional metrics to compare and int erpret the re sults of the methods can also be used (Antar et al., 2025; Chan et al., 2025 ; Thota et al., 2026 ) , like the positive and negative pr edicti ve values , Cohen’ s kappa , th e F 1 s c o re , and the ar ea under the r eceiver operating ch ara cteri stic (RO C) curve . The ch oice of the bes t method may be based not only on predictive quality but also on convenience and interpretability ( Antar et al., 20 25; Chan et al., 2025; Gwalani et al., 2025 ; Hussain et al., 2026; L in e t al., 2025; Molnar , 2020; 2025 ) . Some methods provide an explic it an d interpr etable decision rule and s ome do not, some methods make it possible to s elect the be st predictor subset a nd some do not, some are we ll known to a wide pr actiti oner au dience and som e are not , or not to th e same extent. When machin e learning methods are not inte r pretable ante - hoc, i nterpreta bility of machine learning result s can be enhanced post-hoc by means of the so - call ed explaina ble artific ial intelligenc e (X AI) methods, Shapley additive expl anations - SHAP - ( Antar et al., 2025; Chan et al. , 2026; Hus sain et al., 2026 ; Lin e t al. , 2025 ) an d l ocal in t erpr etable model - agnostic explanations - LI ME - (Antar et al., 2025; Lin et al., 2025) being the most popular . A strong limitation of our s tudy is that o ur sample had a very small number of bankrupt firms. Using a larger portion of the country’ s economy than the 2 - digit NACE clas sificatio n is a po ssibility , although predictio n s m ay be industry - specific ( Balzano & Magrini, 2025). Acknow ledgments This work was supported by the Spanish Ministry o f Science, Innovation a nd Universities MCIN/AEI/10.13039/501 10001 1033 and ERDF - a wa y of making Europe (grant number PID2021-123833OB- I 00); the Spanish Ministry of Health ( grant number CIBERCB06/02/1002); and AGAUR and the Dep ar tment of C limate Action, Food a nd Rural Agenda of Generalitat de Catalunya (grant number 2023 - CLI MA - 00037). Conf lict s of interest The au thors decl are no confl ict of interest. Data availability The cu rated dat a are available fro m the correspond ing author upon reas onable request. Keiv ani el al. ( 2026 ) , arX iv . 12 References Aitchison, J. ( 1982). T he statistica l analysis of compos itional data (with discuss ion). Journal of the R oyal Sta tistical Society Ser i es B ( Statistical Methodology ), 4 4(2 ), 139-177. https ://doi.org/10.1 1 1 1/j. 2517 -6161.1982.tb01 195. x Aitchison, J. (1983). Principal component analysis of compositional data. Biometrik a , 70(1), 57 - 6 5. ht tps://doi .org/10.1093/biomet/70 . 1.57 Aitchison, J. (1986). T he statistical analysis of compositional data. Monographs on statistics and applied pr obabili ty . London, UK : Ch apman and Hall. Aitchi son, J. , Bar celó - V idal, C., Martín - Fernán dez, J. A., & Pawlowsky - Glahn V . (2000). Logratio analysis and compositional dista nces. Mathe matical Geology , 32(3 ), 271 - 275. ht tps://doi .org/10 .1023/A:1007529726302 Akusta, A., & Gün, M. (2025). Predicting f inan cial distress in the textile industry: a comparative analysis o f meta models and s ingle cla ss ifiers. International Journal of Economics, Business and Politics , 9(1), 20 -36. https://doi.org/10.29216/ueip.1599431 Altman, E. I. (1968). Financial ratios, discrimina nt analysis and the prediction of corporate bankruptcy . The Journal of Finance , 23 ( 4), 589 - 609. https://doi.org/10.2307/2978933 Ama t, J. M ., M artín ez, J . I. & R oure , J. (2008). T ransformarse o de sapare cer: estrategias de la empr esa familiar para c ompetir en el s igl o XXI . Barcel ona, ES: Ediciones Deusto. Antar , M., Hassan, R., & B arka, D. (2025). From black box to clarity: m achine learning and agnostic techniques in cr edit r isk management. Journal of Corpor at e Accounting & Finance . Epub ahe ad of p rint. https: //doi.org/10.1002/jcaf.70020 Antar, M., & T ayachi , T . (2 025). Parti al depen dence analy sis of fi nancial rati os in predicting company defaults : r andom forest vs XGBoost models. Digital Finance , 7, 997 -1012 . https://doi.org/10 . 1007/s42521-025-00135-6 Arimany - Serr at, N., Farr eras -Noguer , M. À ., & Coenders, G. (2022). New developments in financial s tatement analy sis . Liquidity in the winery sec tor . Accounting , 8(3), 355-366. https ://doi.org/10.5267/j.ac.2021.10.002 Asif, S., Hemalatha, T ., & V i vekananda R eddy , D. ( 2025). Advancing co r porate bankruptcy forecasting: a multi - model approa ch with enhanced imbalance handling. I nternational Journal for Res earch in A pplied Science & Engineering T echnology ( IJ RASE T ), 13(XII), 183 -793. https://doi.org/10.22214/ijraset.2025.76171 Keiv ani el al. ( 2026 ) , arX iv . 13 Balzano, M., & M agrini, A . (2025). No eas y way out: disse cting firm heterogeneity t o enhance default risk prediction. S INERGI E , 43, 161 -183. https://dx.doi. org /10. 7433/s128.2025 .07 Breiman, L. (2001). Random forests. Machine Lear ni ng , 45(1), 5 - 3 2. https://doi.org/10.1023/A:1010933404324 Carreras Simó, M., & C oenders, G . (2021). T he rela tionship between as set and capital structure: a compositional appr oach wi th panel vector autoregr ess ive models. Quantitative Finance and Econo mics , 5(4), 571 -590. https://doi.org/10.3934/QFE.2021025 Ch an, C . P ., T sai , C. H ., T an g, F . K., & Y ang , J. H. (2 025) . A SHA P - based compar ative analys is of machine lea r ning model inte r pretabili ty in financ ial clas sification tas ks. Journal of A pp lied Economic Sc iences , 3(89), 385 – 400. https://doi.org/10.57017/jaes .v20. 3(89).03 Chen, Y ., L i, R., & W ang, X. (2025). Ear ly warning of financial distress in listed compani es: a machine l earni ng appr oach . Fr ontiers in Busines s and Finance, 2 (2), 229-244. https ://doi.org/10.71465/fbf378 Chohan, M. A., Li , T . , Abr ar , M., & Butt, S. ( 2026). Deep hybrid CNN - LS TM - GRU model fo r a financia l ris k early wa rning sys tem. Ri sks , 14( 1), 14 . https://doi.org/10.3390/risks14010014 Coenders, G. (2025). Application aux ratios finan ciers. I n F. Bertrand , A. Gégout- Petit, & C. Thomas- Agnan (Eds.), Données de composition , (pp. 227 - 244) . Pa ri s, FR: Éditions TECHNIP . Coenders, G., & A r imany - Serrat, N. (2025). An álisis es tadístico de la info rmac ión financiera. Metodología composicional . Girona, ES: Documenta Universitaria. https://doi.org/10.331 15/b/ 9788499847016 Coenders, G., & Arimany - Serrat, N. (in p ress). T en years of compositional analysis of financial ratios . Review , guidelines and f uture dir ections. Europe an A ccounting and Management Review . Coenders, G., E gozcue, J. J., Fačevicov á, K., Navar ro - Ló pez, C., Palar ea - Albal adejo, J., Pawlowsky - Glahn, V ., & T olosana - Delgado, R. (2023a). 40 years after Aitchison’ s arti cle “The st atistical analysi s of com positi onal data”. Wher e we are and w here we are headi ng. SORT . Statistics and Operations Rese arch T rans actions , 47(2), 207 - 228. ht tps://doi .org/10 .57645/20. 8080 .02.6 Coenders, G., & Gr eenacre, M. (2023) . Three approaches to supervised learning for compos itional data with pai rwise logratios . Journ al of Applied S tatistics , 5 0 (16 ), 3272-3293. https ://doi.org/10.1080/02664763 .2022.2108007 Keiv ani el al. ( 2026 ) , arX iv . 14 Coenders, G., & Pawlowsky - Glahn, V . (2020). On interpretations of tests and ef fect sizes in regression models with a c ompositional predictor . SORT . Statistic s and Operations Res earch T ransactions , 44( 1), 201 -220. https://doi.org/10.2436/20.8080.02.100 Coenders, G., Sgo r la, A. F ., Arimany - Serrat, N., Li nares - Must arós, S ., & Farre ras - Noguer , M. À. (2023b) . Nuevos m étodos es tadísticos composicionales para el anális is d e ratio s contables. Revista de Comptabilit at i Di rec ció , 35 , 135 -148. Cojocaru, C., & Iones cu, S. ( 2025). Mapping m achine learning rese arch networks in financial ris k p r ediction. B usiness Excell ence , 19(1), 1248 -1259. https://doi.org/10.2478/picbe-2025-0099 Comas - Cufí, M. , & T hió - Henestrosa, S. (201 1). CoDaPack 2.0: a stand - alone, multi - platform compositional software. In J. J. E gozcue , R. T olosana - Delgado, & M. I. Ortego (Eds.), CoDaW ork'1 1: 4th international wor kshop on compositional data analysis. Sant Feliu de Guíxols , (pp . 1 - 10). Girona , ES: Universitat de Girona . Creixan s - T ena s, J ., Coe nde rs, G ., & Ari ma ny - Serr at, N. (2019). Corporate social responsibility and f inancial pr ofile o f Spanish p rivate hospitals . Heliyon, 5(10), e02623. https://doi.org/10.1016/j.heliyon.2019.e02 623 Dao, B. T. T ., Coe nders , G ., Lai , P . H., Dam , T . T ., & T ri nh , H. T . (2024). An empirica l examination of financial performance and distres s profiles during Covid - 19: the case of fishery and food production firms in V ietnam. Journal of Financial Reporting and Accounting . E pub a head of p rint. https://doi.org/10.1 108/JFRA-09- 2023-0509 Dam, T . T . T ., & Nghiem , T . L. (2026). Applying machine learning to predict fina ncial distr ess: a case study of V ietnam ese real estate co mpanies. International Journal of Management Studies and Social Science R esear ch , 8(1), 1 12 - 120 . https://doi.org/10.56293/IJMSSSR.2026.6008 Dumitrescu, D., Bobitan, N. , Popa, A. F . , S ah lian , D . N. , & Stanila , C. A. (2025). Signaling financial distres s through A - scores and corpor ate gov ernance co mplian ce interplay: A r andom fo rest approach. Electronics , 14, 2151. https://doi.org/10.3390/electronics141 12151 Durana, P ., Kova l ova, E., Blazek, R., & B icano vska, K. (2025). Bus iness ef ficiency: Insights from V isegrad four before, during, and aft er the COVID - 19 pandemic. Economies , 13(2), 26. https://doi.org/10 . 3390/econ omies13020026 Egozcue. J. J ., & Pawlowsky - Glahn V . (2019). Co m positional data: the s ample spac e and its s tructure. TEST , 28(3), 599 –638. https://doi .org /10.1007/s1 1749-019- 00670-6 Egozcue, J. J ., Paw lowsky - Glahn, V . , Mateu - F igueras, G., & Barceló - V idal, C. (2003). Isometric log ratio tran sformations for compositional d ata analysis . Mathematical Geology , 35(3), 279 –300. https://doi.org/ 10. 1023/ A:1023818214614 Keiv ani el al. ( 2026 ) , arX iv . 15 Engle, M. A., & Chaput, J. A. (2021). Groundwater origin determination in historic chemical datas et s through supervised compositional data analysis: B r ines of the Per m ian Basi n, US A. In P . Fi lz mos er, K . Hr o n, J. A. Ma rtín - Fernánd ez, & J. Palar ea - Albaladejo (Eds.), Advances in c ompositional data analysis: fes tschrift in honour of V era Pawlowsky -Glahn , (pp. 265 - 283). Cham , CH : Springer . https://doi.org/10.1007/978-3-030-71 175- 7_14 Escaram ís , G., & Arbussà, A. (2025). Considerations on the use o f financial ratios in the study of family businesses . arX iv , 2501.16793. https://doi.org/10.48550/arXiv .2501. 16793 Farr eras - Noguer , M. À., Carreras - Piju an, M., L inares - Must ar ós, S. , & Ar im any - Serrat, N. (in press). Subsidies and financial pe rforman ce in the rural tourism se ctor . Europe an Accounting and Management Review . Gabrielli, G. , Melioli, A ., & Bertini, F . (2026) . Corporate financ ial distress pr ediction: a machine learning approach in the era of big data. Journal of Accounting & Or ganizational Change , 22 ( 7), 31 - 6 5. https://doi.org/10.1 108/JAOC-05-2025- 0166 Gajdosikova, D., V alaskova, K., & Durana, P . (20 26) . Cross - national benchmarking of bankruptcy prediction models across V4 economies. International Journal of Econ omic Scien ces , 15 (1), 158 -176. https://doi.org /10.31 181/ijes1512026223 Gnip, P ., Kanasz, R . , Z oričak, M., & Drotar , P . ( 2025). An e xper ime ntal s ur vey of imbalanced learning algorithms for bankruptcy prediction. Artific ial Inte lligence Review , 58(4), 104. h t tps://doi.org /10. 1007/s10462 -025- 111 0 7 -y Greenacre, M. (2019) . V ariable s election in compositional data analysis using pairwise logratios. Mathemati cal Geosciences , 51(5), 649 -682. https://doi.org/10.1007/s1 1004-018- 9754-x Greenacr e, M. , Grunsky , E., Bacon - Shone, J., Erb, I., & Quinn , T . (2023). Aitchison’ s compositional data ana lysis 40 yea r s on: A reappraisal. Statistical Sc ience , 38(3) , 386-410. https ://doi.org/10.1214/22-STS880 Grover , J., & L avin, A. (2001). Fi nancial ratios, d iscriminant analysis and the pr ediction of corporate bankrup tcy: a service indus t ry e xtension of Altman’ s Z - score model of bankruptcy prediction. W orking Paper . Southern Finance Assoc i ation. Gwalani, M., T eltumbde, G ., & Gw alani, H . (2025). T r ends in pr edict ing co r por ate distres s: a bibliometric and thematic a nalysis . NMIMS M anagement Review . , 33(4), 243-252 . https://doi.org/10 .1 177/0971 1023251360528 Hanun, R. U. , & Ferd iani, C. (2025). L iter ature analysis on finan cial distress and bankruptcy prediction. Fa irne ss , 1(1), 16 -30. https://doi.org/10.70764/gdpu - fr . 2025.1(1)-02 Keiv ani el al. ( 2026 ) , arX iv . 16 Hernan dez - Romer o, M. , & Coenders, G. (in p ress ). Financi al resil ience of agri cultur al and food production companies in S pain: A compositional clus ter analysis of the impact of the Ukraine - Russia wa r (2021 -202 3) . Eur opean Accounting and Mana gement R eview . Hia, S., Kuswanto, H., & Prastyo, D. D. (2023). Robustnes s of support vector r egression and random forest models : a simulation study . In Y . B. W ah, M. W . Berry , A. Mohamed, & D. Al - Jumeily (Eds.), Data sc i ence and em er ging technologies. DASET 2022 . L ectur e notes on data engineer i ng and communications tec hnol ogies, vol 165 , (pp. 465 - 479). Singapore , S G : Springer Natur e. https://doi.org/10.1007/978-981-99-0741-0_33 Hu ss ain , A. B ., Jing chun , S., H uss ain, B ., Sh aiqu e , M., R ehma n, A. U ., & B hat ti, M. K . (2026). Cross - market bankruptcy prediction: an i nterpretable ensemble learning framework using SHAP analysis. Computational Economics . Epub ahead of pri nt . https://doi.org/10.1007/s10614-025-1 1266-8 Insani, F ., P on toh, G. T ., & Said, D . (2024). Corporate bankruptcy prediction model: A sys tematic literature revie w . International Jour nal of Busines s, Economics and Management , 7(3), 143 -159. https://doi.org/10 .21744/ijbem.v7n3.2222 Iot ti, M ., Fe rri, G ., & Bonazzi, F . (2024). Financial ratios, credit risk and business strategy: Application to the PDO Parma ham sect or i n single production and non - single production firms. Journal of A gricultur e and Food Resear ch , 16, 101 122. https://doi.org/10.1016/j.jafr .2024.101 122 Jo fre - Campuza no, P ., & Coe nder s, G . (2022). Co mpositional classification of financial statement prof iles. The w eighted case. Journal of Risk and Financial Management , 15(12), 546. https://doi.or g/10. 3390/jrfm15120546 Kanojia, S., & Arora, A. ( 2025). Machine le arning for credit risk management through cr oss - economy evidence in default prediction. SN B usiness & E conomics , 5 (12 ), 221. ht tps://doi .org/10 .1007/s43546-025-00995- 5 Khotimah, K., & W anti W i dodo , U. P . (2026). A c om parative study of ANN and logistic regression for financial distress prediction in Indones ian manuf acturing firms. Jurnal Ilmu A kuntansi dan B isnis Syar i ah , 8(1), 53 - 7 2. https://doi.org/10.15575/aksy .v8i 1.52046 Kristanti, F . T ., Salim , D. F ., & Ihsan, A . F . (2025). Financia l distress pre diction in emerging markets by using a machine learning approach for f inancial sustainability . Discove r Sustainability , 6(1), 1296. https://doi .org/10.1007/s43621-025-02199-1 Lin, Y . C., Padlians yah, R., Lu, Y . H . , & Liu, W . R. ( 2025 ). Bankruptcy pr ediction: Integration of convolutional ne ural networks and explainable arti ficial intelligence techniques. International Journal of A ccounting In formation Systems , 56 , 100744. https://doi.org/10.1016/j.accinf.2025.100744 Keiv ani el al. ( 2026 ) , arX iv . 17 Lin ares - Mustarós, S., Coenders, G., & V ives - Mestres, M. (2 018). Financi al perfor mance and dis tress pr o f iles. Fr om classifica tion according to financial ratios to compos itional cla ss ification. Advances in Accounting , 40, 1 - 10. https://doi.org/10.1016/j.adiac.2017.10.003 Lin ares - Mustar ós, S. , Farr eras - Noguer , M. À ., Arimany - Serrat, N., & Coenders, G. (2022). New f inancial ratios based on the compositi onal data methodology . Axioms , 1 1(12), 694. https://doi. o rg/10.3390/ axioms1 1 120694 Liu, F . (2025 a ). Intelligent i denti f ication a nd earl y warning model fo r corporate financial risk based on de ep learning. Resear chSquare . https://doi.org/10 .21203/rs. 3 . rs- 7201319/v1 Liu, J., Li, Y ., & Y u, J. (2025). Predicting financial d istress w ith ESG‐ driven deep learning and risk‐bas ed stratification . International Journal of Finance & E conomics . Epub ahead of print. h t tps://doi.org/10 .1002/ijfe.70077 Liu, S. (2025 b ) . LT R - Net: A deep l earni ng - based approach for financial data prediction and risk evaluation in enterprises. P los one , 20(8), e0328013. https://doi.org/10.1371/journal.pone.0328013 Magrini, A. (2025). B ankruptcy risk p rediction: a new approach based on compositional analys is of financial sta tements. Bi g Dat a R esearch , 41 , 1000537. https://doi.org/10.1016/j.bdr .2025.100537 Martin - Melero, I., Gomez - Mar tinez, R., Medr ano - Garcia, M. L., & Her nández - Pe r lines , F . (2025). Comparison o f corporate ins olvency pr ediction in Spain e mploying fin ancial r atios in analyti cal model s and machine learn ing. Academi a Revista Latinoamericana de Administración , 38( 1), 134 -155. https://doi.org/10.1 108/ARLA- 04-2024-0060 Matsuma ru, M., & Katagiri, H. (2025). A two - stage machine lear ning appro ach to bankruptcy prediction: integrating f ull - feature modeling and optimize d feature selection . Journal of Risk and Financial Manageme nt , 18(12), 662. https://doi.org/10.3390/jrfm18120662 Mola s - Col omer , X., Fe rrer - Comalat, J. C., Carr eras - Pijuan, M., & L ina r es - Mustar ós, S. (2026). Beyond traditional ratios: predicting financial d istress through compos itional data and fuzzy cluste ring in ag r icult ural retail. Journal of Mu lti ple - V alued Logic and Soft C omputing . Mola s - Colom er , X., Li nares - Mustar ós, S. , F arr eras - Noguer , M. À., & Ferr er - Comala t, J. C. (2024). A new methodologi cal pr oposal for cla ssifying firms a ccording to the similarity of their financ ial structure s bas ed on co mbining compositiona l data with fuzzy cl usteri ng . Journal of Multiple - V alued Logic and Soft Com puting , 43, 73 -100. Molnar , C. (2020) . Interpr etable machine learning. A guide for making black box models explainable . Lulu.com. Keiv ani el al. ( 2026 ) , arX iv . 18 Molnar , C. (2025). Interpr eting machine lear ning models with SHAP: a guide w i th Python examples and theory on Shapley v al ues. Christoph Molnar . Mule t - F ort eza, C., F errer - Ros ell, B. , Martorell - Cunill, O., Linares - Musta ró s, S . (in press). The role of expansion strategies and oper ational attributes on hotel performance: a compositional approach. T ourism Management Perspec tives. https://doi.org/10.48550/arXiv .241 1. 04640 Nat hwa ni , C. L., W ilki nso n, J. J. , Fry , G., Ar mst rong , R. N., Smi th , D. J., & Ihle nf el d, C. (2022). Machine lea rning fo r geochemical explor ation: class if ying metallogenic fertility i n arc magmas and ins ight s into porph yry copper deposit formation. Mineralium Deposita , 57(7), 1 143 -1 166. htt p s://doi. org/10.1007/s 00126- 021- 01086-9 Nugroho, D. S., & De wayanto, T . (2025). Applica tion of statistics and a rtificial intelligenc e for corpo rate financial dis tress prediction mode ls: a sys tematic liter atur e review . Journal of Modelling in Management , 20(6), 1999 -2023 . https://doi.org/10.1 108/JM2-12-2024- 0412 Palar ea - Albaladejo , J., & Ma rtín - Fer nández, J. A . (2008). A modifi ed EM alr - algorith m for r eplacing rounded zeros in compositional da t a sets. Comput ers & Geosci ences , 34(8), 902 -917. https://doi.org/10 . 1016/j.cageo.2007.09.015 Pawlowsky - Glahn, V ., E gozcue, J . J., & T olosana - Delgado, R. (2015). Modeling and analysis of com positional data . Ch iches ter , UK: W iley . R Core T eam (2025). R: A language and envir onment for statis tical computing . V ienna, A T : R Foundation f o r Statistic al Computin g . https ://www .R -pr oject.or g/ . Soukal, I., Mačí, J., T rnková, G., Svobodova, L. , Hedvič áková, M ., Hamplova, E., Maresova, P ., & Lefley , F . (2024). A stat e - of - th e - art appraisal o f bankruptcy prediction models focussing on the field’ s cor e authors: 2010 -2022. Centr al Europe an M anagement Journal , 32( 1), 3 - 3 0. https ://doi.org/10.1 108/ C E MJ-08- 2022-0095 Springate, G. L . (1978). P r edicting t he possibility o f failu re in a C anadian fir m . Burnaby , BC: Simon Fras er Unive rsity . Staňková, M., & Hampel, D. (2023). Optimal th reshold of data envelopment analysis in bankruptcy prediction. SO R T . Statistics and Ope rations Resear ch T ransactions , 47(1), 129 -150. https://doi.org /10.57645/20.8080.02.3 T anaka, K. , Higashide, T ., Kinkyo, T . , & Hamori , S. (2025a). Financial mec hanisms of corpo rate ban krupt cy: ar e they different or similar across cri ses? R i sks , 13 (8), 158. https://doi.org/10.3390/risks13080158 Keiv ani el al. ( 2026 ) , arX iv . 19 T anaka, K., Higashide, T . , Kinkyo , T ., & Hamori , S. (2025 b ). A multi - stage fi nancial distress e ar ly warning s ystem: analyzing corporate insolve ncy with random fo r est. Journal of Risk and Financial Manageme nt, 18 (4), 195. https://doi.org/10.3390/jrfm18040195 T aoushianis, Z. (2025). Bankruptcy prediction with fractional polynomial trans f ormation of financial ratio s. Eur opean Journal of Operatio nal Resear ch , 327(1), 690 -702. https://doi.org/10.1016/j.ejor . 2025.07.036 Te m p l , M., & Gonzalez - Rodriguez, J . (2024). Advancing forensic r esea rch: An examination of compositional data analys i s with an applica tion on petrol fraud detecti on. Science & Ju sti ce , 64(1) , 9 -18. https://doi.org/10.1016/j.scijus.2023.1 1.003 Tho ta , N ., De sa i, G. , Puli , S., Subra hman yam , A. C . V ., & V ishw esw ars as try , V . N . (2026). Predicting bankruptcy in wholesa l e, retail, and motor vehicle repair: An AI - ML per spective. F1000Resear ch , 14, 1251 . https://doi.org/10.12688/f1000research.170279.2 T olosana- Delgado, R., T alebi, H. , Khodadadz adeh, M. , & V an den Boogaart, K . G. (2019). On machine learni ng algor ithms and compositional data. I n J. J . Egozcue, J. Gr aff el m an , & M. I. O rte go (E ds. ), Pr oceedings of the 8th inter national work shop on compositional data analysis , (pp. 172 - 175). Bar celona , ES : Catal an Pol ytechni c University - Barcel onaTE CH. T ran, K . P . (2025). Apprentissage automatique pour l’analyse de données de composition. In F . Bertrand, A. Gégout - Petit, C. Thomas - Agnan (Eds.), Données de compos ition , (pp. 85 - 108). Paris, FR: É ditions T ECHNIP . V egan zones, D. , & S é verin , E. (2021 ). Corporate fa ilur e prediction models in the twenty - fir st centur y: a r eview . E ur opean B usine ss Review , 33(2) , 204 -226. https://doi.org/10.1 108/E BR-12-2018-0209 V eganzones, D., Séverin, E., & Jabeur , S. B. (2026). Forecas ti ng corporate bankruptcy in imbalanced datas et s using a new hybrid machine learning approach. Research in International Business and Fi nance , 81, 103200. https://doi.org/10.1016/j.ribaf.2025.103200 V enab les, W . N ., & R ipley , B . D. (2002). Moder n a pplied statistic s with S, Fourth edition . New Y ork, N Y : Springer . https://doi.org/10.1007 / 9 78-0-387-21706- 2 W ang, Z., Che, W . , J iang, C. , & Zhao, H . (2026). Leveraging multiview data through discrete and regularized deep le arning for dynamic financial risk prediction. Information Systems Res ear ch . https://doi.org/10. 1287/i sre.2024.1417 Keiv ani el al. ( 2026 ) , arX iv . 20 W ill er do Prado, J., de Cas t ro Alcântar a, V ., de Melo Carvalho , F . , Carvalho V iei ra, K., Cruz Machado, L. K . , & Flávio T onelli, D . (2016 ). Multivariate analys is of credit risk and bankr uptcy r esearch data : a bibliometric study involving dif ferent knowledge fields (1968 -2014). Sciento metrics , 106(3), 1007 -1029. https://doi.org/10.1007/s1 1 192- 015-1829-6 Xu, Y . (2026). Big data and mac hine learning methods in financia l risk prediction . Scientific Journal of Economics and Manageme nt Resear ch , 8( 1), 53 -58. https://doi.org/10.54691/9eb6x521 Y uan, S. ( 2025) . Algo rithmic transformation of fina ncial risk identifica tion methods : from traditional mode ls to da ta - intelligent framew orks. Journal of Applied E conomics and Policy Studies , 18(7), 62 - 66. https://doi.org/10 . 54254/2977-5701/2025.25760 Zhao, W . (2025). Mac hine learning for sustainable financial sys tems: ass e ssing corporate resili ence and def ault r isk. Advances in Management and Intelligent T echnologies , 1(6), 1 - 11 . https://doi.org/10 .62177/ amit.v1i6.849 Zhu, X., S un , H., Chang, Y ., & Li, J. ( 2026). Predicting financial distres s using textual risk disclosures i n annual reports: How and what risks ar e disclos ed? The British Accou nting R eview , 101836. https://doi.or g/10. 1016/j.bar .2026.101836 Zmijewski, M. E. ( 1983). Ess ays on corporate bankruptcy . Docto ral thesis . State University of New Y ork at Buf f alo.

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment