Voluntary Renewable Programs: Optimal Pricing and Revenue Allocation

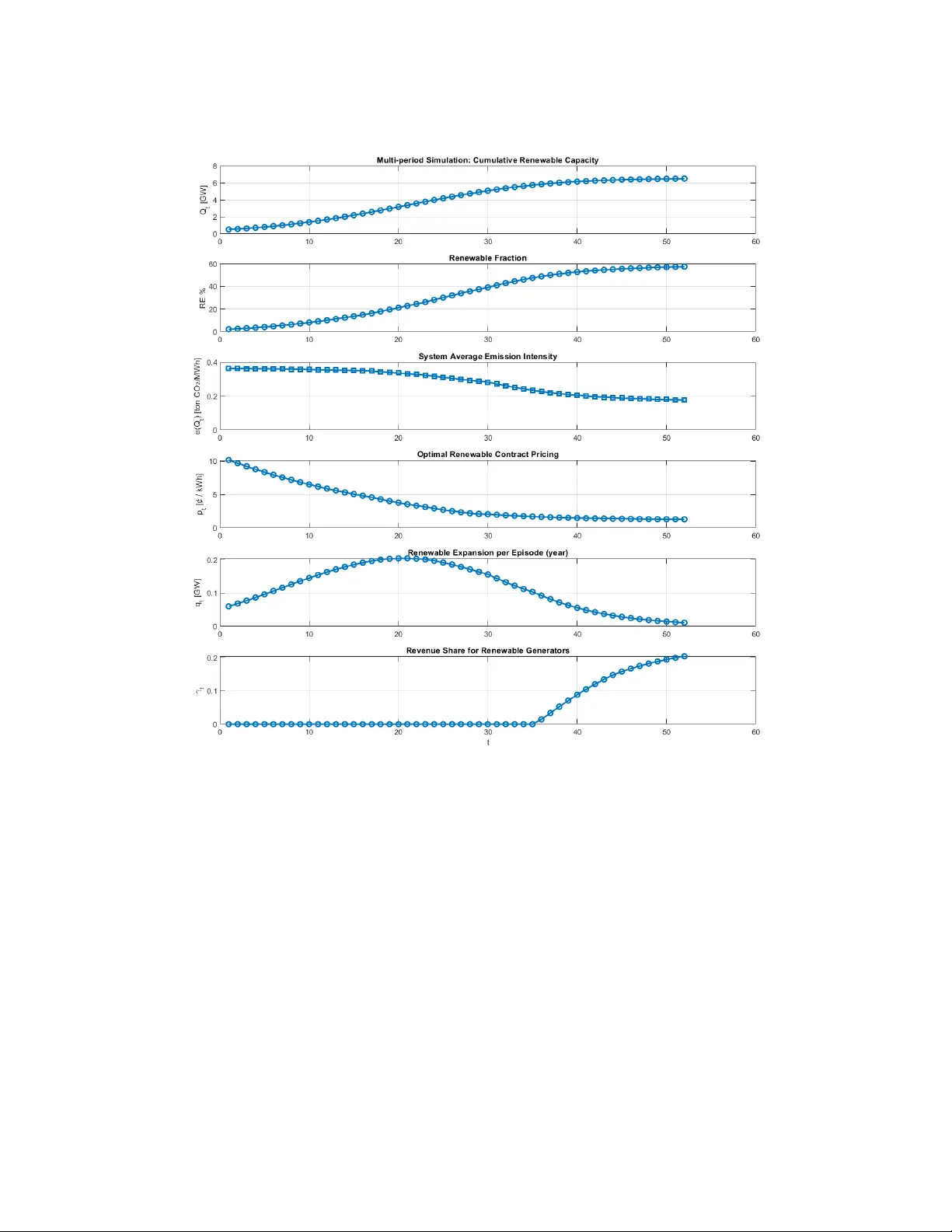

This paper develops a multi-period optimization framework to design a voluntary renewable program (VRP) for an electric utility company, aiming to maximize total renewable energy deployments. In the business model of VRP, the utility must ensure it g…

Authors: Zhiyuan Fan, Tianyi Lin, Bolun Xu