Bid--Ask Martingale Optimal Transport

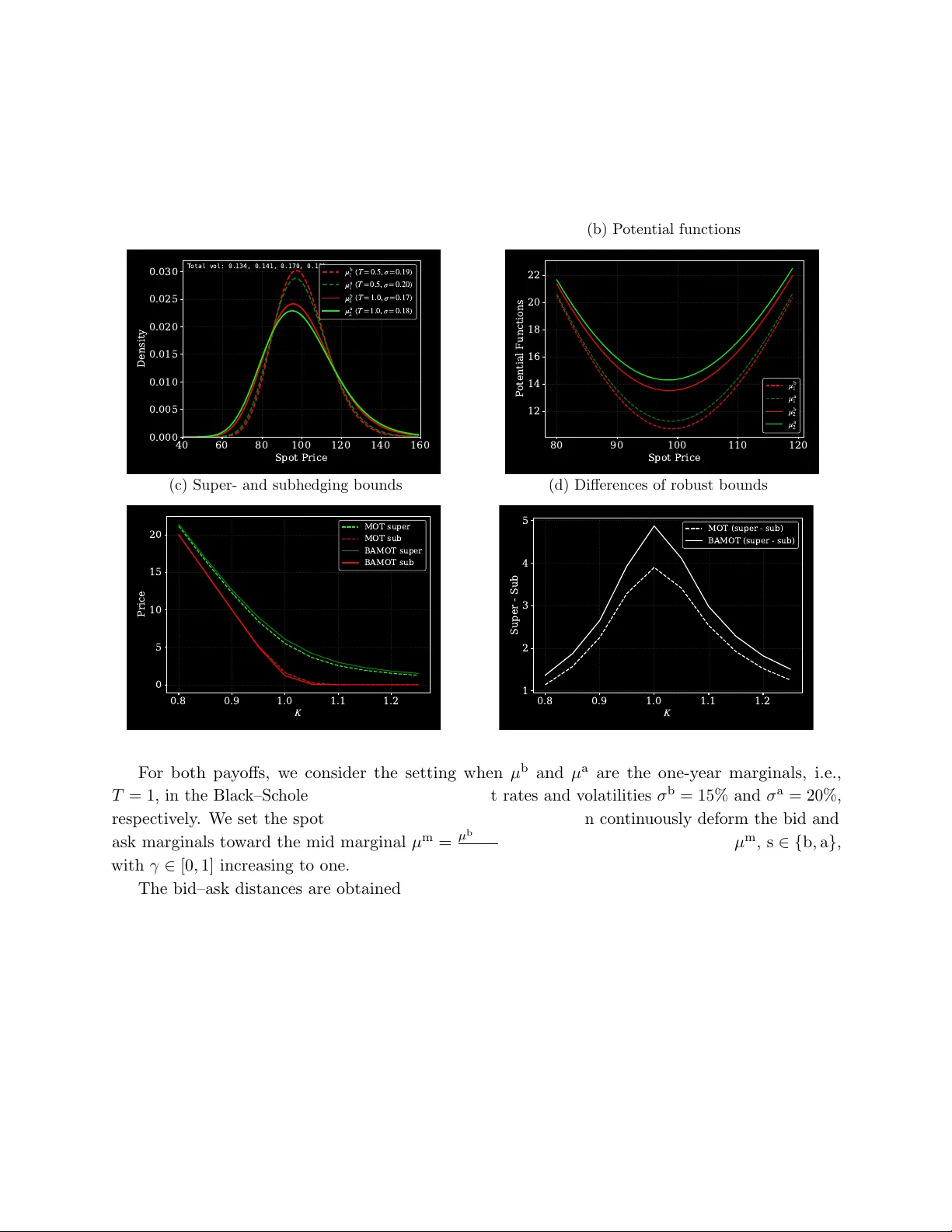

Martingale Optimal Transport (MOT) provides a framework for robust pricing and hedging of illiquid derivatives. Classical MOT enforces exact calibration of model marginals to the mid-prices of vanilla options. Motivated by the industry practice of fi…

Authors: Bryan Liang, Marcel Nutz, Shunan Sheng