On Utility Maximization under Multivariate Fake Stationary Affine Volterra Models

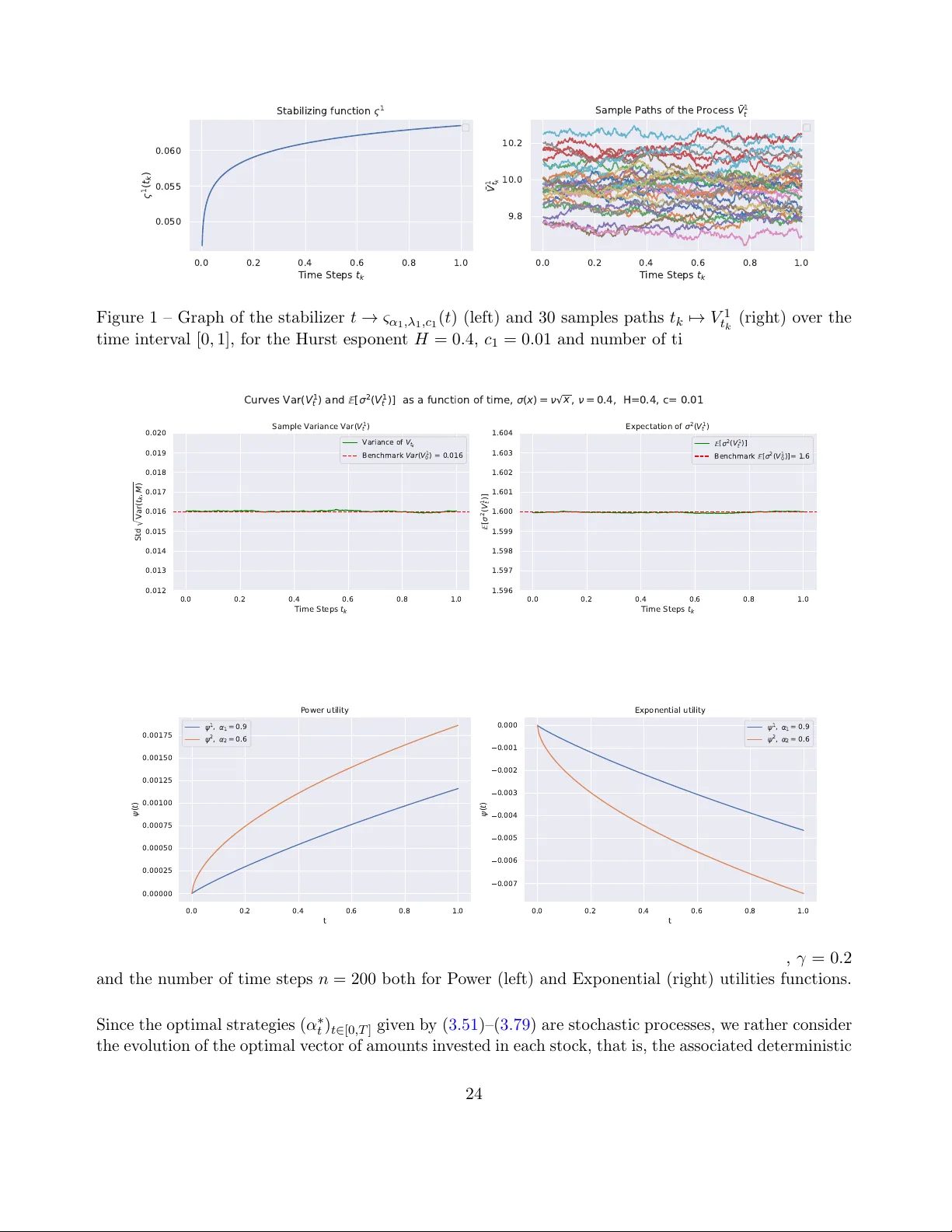

This paper is concerned with Merton's portfolio optimization problem in a Volterra stochastic environment described by a multivariate fake stationary Volterra--Heston model. Due to the non-Markovianity and non-semimartingality of the underlying proce…

Authors: Emmanuel Gnabeyeu