An operator-level ARCH Model

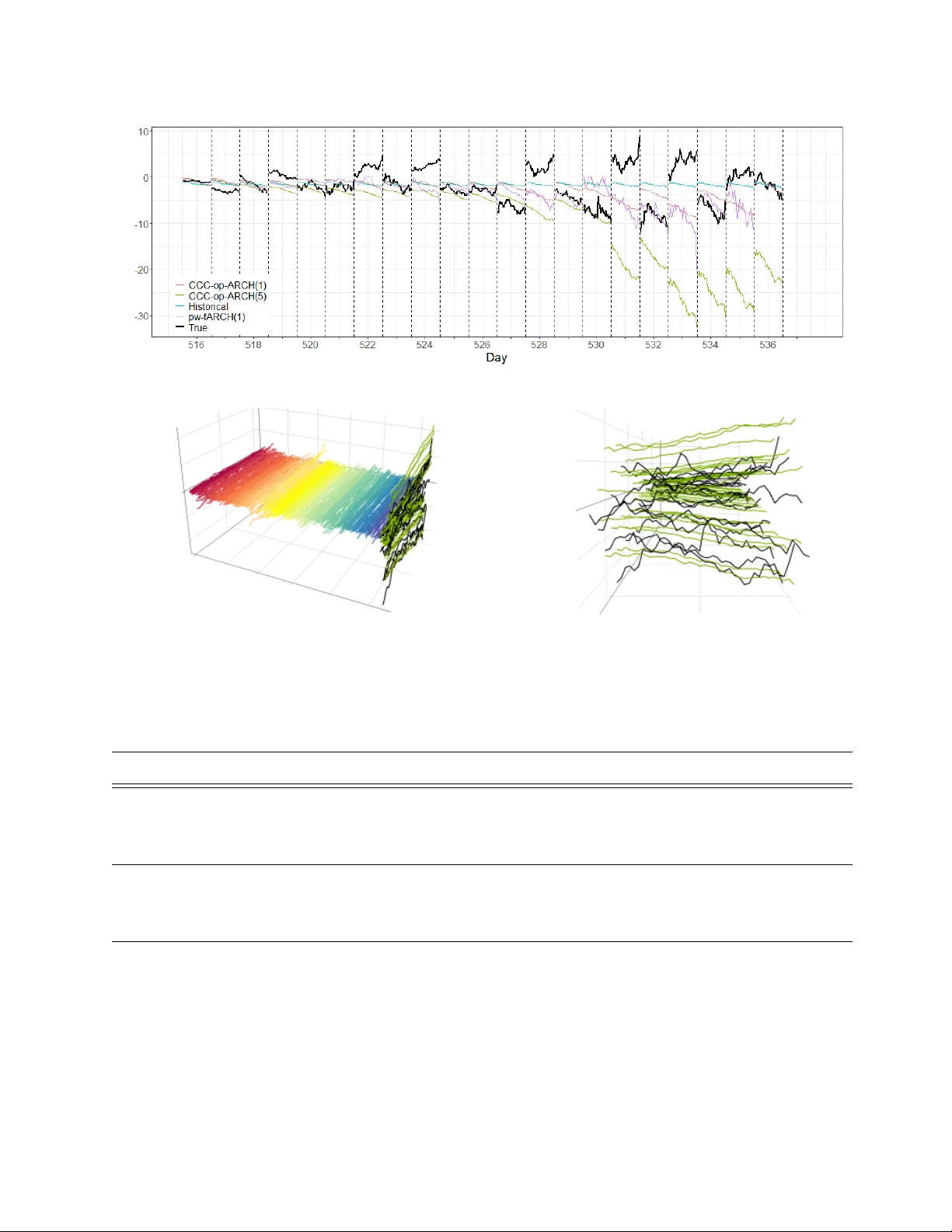

AutoRegressive Conditional Heteroscedasticity (ARCH) models are standard for modeling time series exhibiting volatility, with a rich literature in univariate and multivariate settings. In recent years, these models have been extended to function spac…

Authors: Alex, er Aue, Sebastian Kühnert