Is an investor stolen their profits by mimic investors? Investigated by an agent-based model

Some investors say increasing investors with the same strategy decreasing their profits per an investor. On the other hand, some investors using technical analysis used to use same strategy and parameters with other investors, and say that it is better. Those argues are conflicted each other because one argues using with same strategy decreases profits but another argues it increase profits. However, those arguments have not been investigated yet. In this study, the agent-based artificial financial market model(ABAFMM) was built by adding “additional agents”(AAs) that includes additional fundamental agents (AFAs) and additional technical agents (ATAs) to the prior model. The AFAs(ATAs) trade obeying simple fundamental(technical) strategy having only the one parameter. We investigated earnings of AAs when AAs increased. We found that in the case with increasing AFAs, market prices are made stable that leads to decrease their profits. In the case with increasing ATAs, market prices are made unstable that leads to gain their profits more.

💡 Research Summary

The paper tackles a long‑standing debate in finance: does the proliferation of investors using the same trading strategy erode individual profits, or can it actually enhance them? To answer this question in a controlled setting, the authors extend a previously published agent‑based artificial financial market model (ABAFMM) by introducing “additional agents” (AAs). Two subclasses of AAs are defined: Additional Fundamental Agents (AFAs) that trade solely on a fundamental price gap, and Additional Technical Agents (ATAs) that trade based solely on a single technical parameter (the look‑back period ta). Both types of AAs are deliberately simple – each follows a one‑parameter rule and limits its position to at most one share (or a short of one share), mimicking the behavior of investors who adopt identical strategies and become saturated in their holdings.

The market mechanism is a continuous double auction with a minimum price tick δP. Normal agents (NAs) – 1,000 in number – generate orders by combining three components: a fundamental term, a technical term based on recent returns, and a stochastic noise term. Their weights are drawn uniformly at the start of each simulation, and order prices are scattered uniformly around an expected price to emulate a realistic order book. The simulation parameters (δP=0.01, fundamental price Pf=10,000, weight limits, τmax, σϵ, Pd, etc.) are kept identical to the baseline model of Mizuta and Yagi (2025) to ensure comparability.

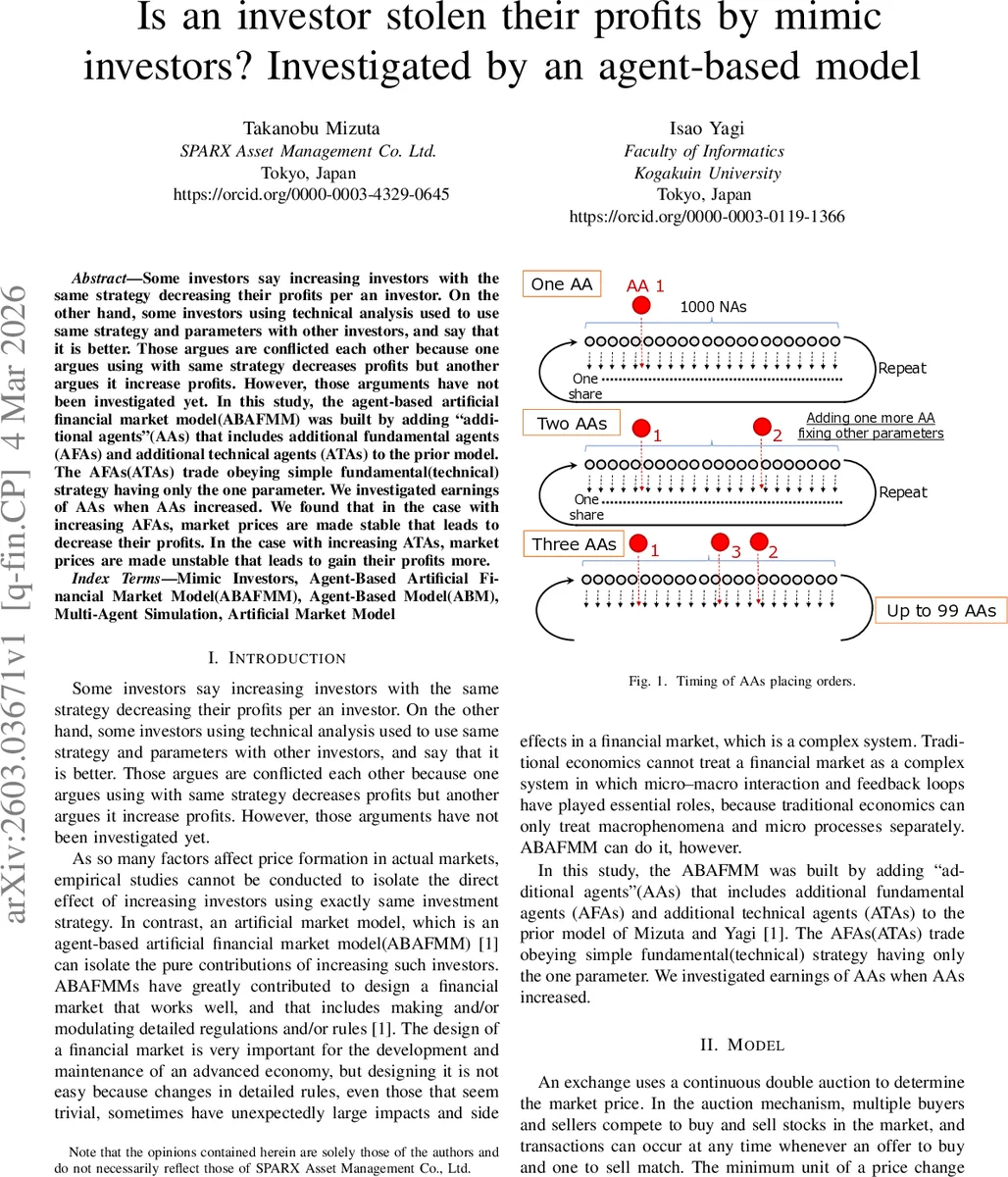

The experiments vary the number of AAs (na) from 0 up to 99 for each subclass while keeping all other settings fixed. Each run proceeds for 20 million time steps, with an initial “warm‑up” phase (tc=10,000 steps) to populate the order book. The authors record three primary outcomes: (1) the time series of the market mid‑price Pt, (2) the average final profit of the AAs, and (3) the total number of trades executed by the AAs.

Results for AFAs: As the number of AFAs increases, the market price rapidly converges toward the fundamental price Pf, indicating strong price stabilization. The mechanism is a negative‑feedback loop: when the price falls below Pf, AFAs buy, pushing the price up; when the price rises above Pf, they sell, pulling it down. Because each AFA’s profit derives from the price gap between market and fundamental, the very act of narrowing this gap reduces future profit opportunities. Consequently, the average profit per AFA declines as more AFAs are added, even though market volatility diminishes.

Results for ATAs: In contrast, adding ATAs amplifies price fluctuations. ATAs buy when the current price exceeds the price ta steps ago and sell when it is lower, creating a positive‑feedback loop. Their trades reinforce the direction of price movement, leading to larger swings and higher volatility. As volatility grows, ATAs capture larger price differentials, and their average profit rises with the number of ATAs. The number of trades initially drops sharply for na < 20 (reflecting early market adjustment) but stabilizes for larger na, indicating that once a critical mass is reached, ATAs continue to trade actively in the volatile environment they help generate.

The paper visualizes these dynamics with price‑time plots (showing stable versus unstable trajectories) and schematic diagrams that illustrate the negative‑feedback (AFAs) and positive‑feedback (ATAs) processes.

From a methodological standpoint, the study demonstrates the utility of agent‑based simulation for isolating the pure effect of strategy homogeneity, something infeasible in empirical market data due to confounding factors. However, the authors acknowledge several limitations. The one‑parameter strategies of AFAs and ATAs are highly stylized and do not capture the multi‑factor decision rules used by real traders. The model omits important market microstructure elements such as order‑book depth, slippage, liquidity provision, and transaction costs beyond the simple tick size, which may affect the magnitude of the observed effects. Sensitivity analyses with respect to initial conditions, parameter choices (e.g., ta, weight distributions), and alternative auction rules are not presented.

Future research directions suggested include (i) enriching agent strategies with multiple parameters and adaptive learning, (ii) incorporating realistic order‑book dynamics and market impact functions, and (iii) calibrating the model against real‑world high‑frequency data to validate the qualitative findings. Such extensions would enhance the external validity of the conclusions and could inform regulators about the systemic implications of large groups of homogeneous traders, whether they are fundamentalists or technical chartists.

In summary, the paper provides clear evidence that the collective behavior of investors employing identical strategies can have opposite effects on market stability and individual profitability, depending on whether the shared strategy is fundamentally anchored or purely technical. This insight contributes to the broader discourse on market design, the role of herd behavior, and the potential unintended consequences of encouraging homogeneous trading practices.

Comments & Academic Discussion

Loading comments...

Leave a Comment