Introducing the b-value: combining unbiased and biased estimators from a sensitivity analysis perspective

In empirical research, when we have multiple estimators for the same parameter of interest, a central question arises: how do we combine unbiased but less precise estimators with biased but more precise ones to improve the inference? Under this setti…

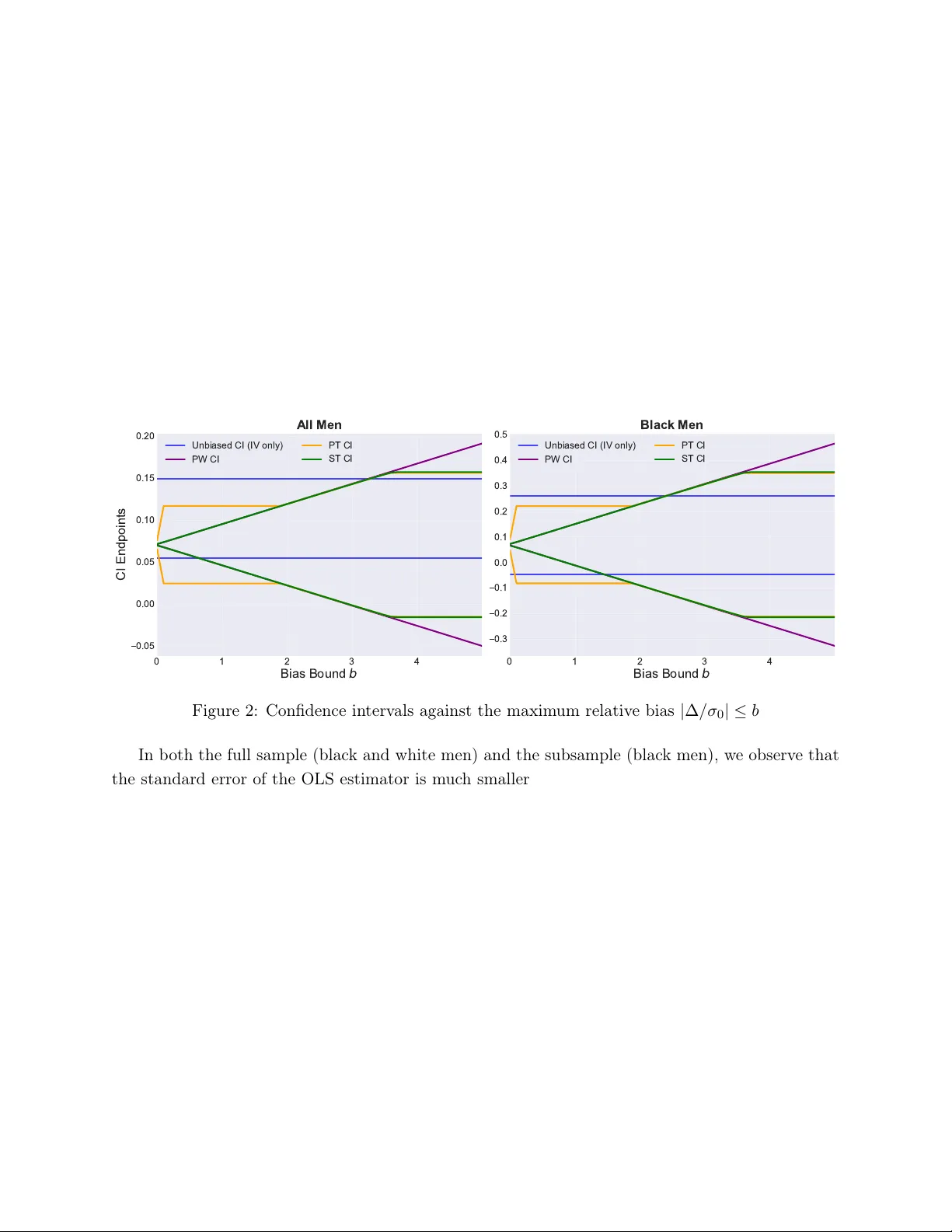

Authors: ** - **Zhe Xiaolin** (주 저자) - (논문에 명시된 다른 공동 저자들이 있다면 여기서 나열) *※ 논문에 정확한 저자 명단이 제공되지 않아, 저자 정보를 확인 후 추가하시기 바랍니다.* --- **