A Minimal Incentive-based Demand Response Program With Self Reported Baseline Mechanism

In this paper, we propose a novel incentive based Demand Response (DR) program with a self reported baseline mechanism. The System Operator (SO) managing the DR program recruits consumers or aggregators of DR resources. The recruited consumers are re…

Authors: Deepan Muthirayan, Enrique Baeyens, Pratyush Chakraborty

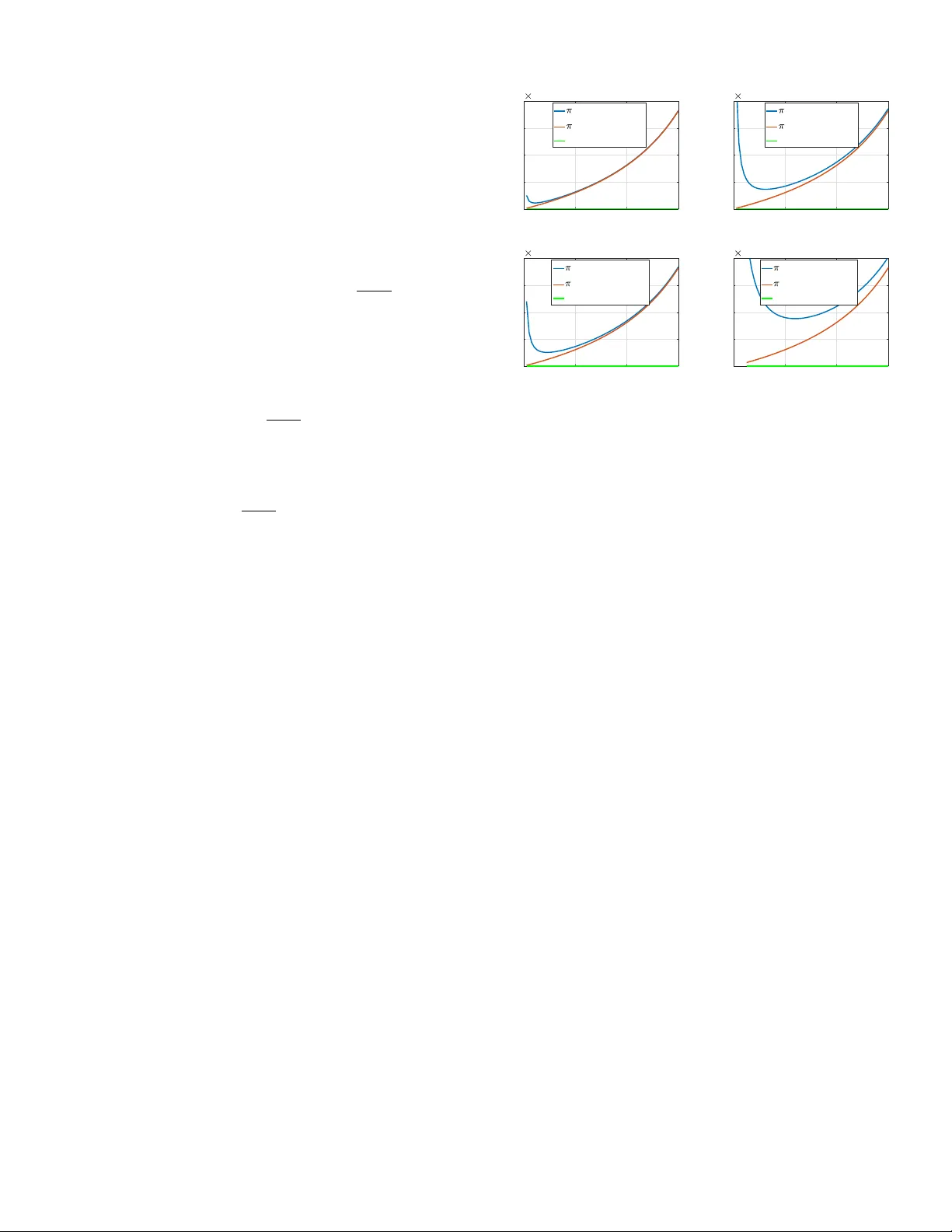

1 A Minimal Incenti v e-based Demand Response Program W ith Self Reported Baseline Mechanism Deepan Muthirayan a , Enrique Baeyens b , Pratyush Chakraborty c , Kameshwar Poolla d and Pramod P . Khargonekar a Abstract —In this paper , we propose a novel incentive based Demand Response (DR) program with a self reported baseline mechanism. The System Operator (SO) managing the DR pro- gram r ecruits consumers or aggregators of DR resour ces. The recruited consumers are required to only report their baseline, which is the minimal information necessary for any DR program. During a DR event, a set of consumers, fr om this pool of recruited consumers, are randomly selected. The consumers are selected such that the required load reduction is deliver ed. The selected consumers, who reduce their load, are rewarded for their services and other r ecruited consumers, who deviate from their reported baseline, are penalized. The randomization in selection and penalty ensure that the baseline inflation is controlled. W e also justify that the selection probability can be simultaneously used to control SO’s cost. This allows the SO to design the mechanism such that its cost is almost optimal when there are no recruitment costs or atleast significantly reduced otherwise. Finally , we also show that the proposed method of self- reported baseline outperforms other baseline estimation methods commonly used in practice. Index T erms —Demand Response, Baseline Estimation, Base- line Inflation. I . I N T R O D U C T I O N Demand Response (DR) programs [1] are potentially pow- erful tools to modulate the demand for electricity in a wide variety of situations. For e xample, at certain times such as mid-afternoons on hot summer days, the supply of additional electric power is scarce and expensi ve. At these times, it is more cost-effecti ve to reduce demand than to increase supply to maintain power balance. Another scenario is a grid with high rene wable penetration. Here, DR promises to be a better alternativ e compared to other expensi ve and polluting reserves to balance the variability in renewable generation. Realizing its potential, the 2005 Energy Policy Act provided the Con- gressional mandate to promote DR in organized wholesale electricity markets. The FERC order 745 [2] met this mandate by prescribing that demand response resource owners should be allowed to offer their demand reduction as if it were a This research is supported by the National Science Foundation under grants EA GER-1549945, CPS-1646612, CNS-1723856 and by the National Research Foundation of Singapore under a grant to the Berkeley Alliance for Research in Singapore a Department of Electrical Engineering and Computer Science, University of California, Irvine, CA, USA b Instituto de las T ecnolog ´ ıas A vanzadas de la Producci ´ on, Univ ersidad de V alladolid, V alladolid, Spain c Department of Physics and Astronomy , Northwestern University , IL, USA d Department of Electrical Engineering and Computer Science, Univ ersity of California, Berkeley , CA, USA supply resource rather than a bid to reduce demand so that the market operates fairly . Dynamic pricing based DR programs [3], [4] can ideally achiev e market efficienc y , but they require more comple x metering and communication infrastructure to achieve this which raises their implementation costs [5], [6]. Furthermore, consumers may not be responsive to dynamic pricing [7]. Alternativ ely , consumers could be signaled to reduce con- sumption and paid for their load reductions. Such schemes are referred to as Incenti ve-based DR programs or Demand Reduction programs. There are three key components of any incentiv e-based DR program: (a) a baseline against which demand reduction is measured, (b) a payment scheme for agents who reduce their consumption from the baseline, and (c) various contractual clauses such as limits on the frequency of DR ev ents or penalties for nonconforming agents. Thus, incentiv e-based DR programs require an established baseline against which consumer’ s load reduction is measured. The baseline is an estimate of the consumption when the consumer is not participating in the DR program. For example, the California Independent System Operator (CAISO) uses the av erage of the consumption on the ten most recent non-ev ent days as the baseline estimate [8]. The CAISO method also uses a morning adjustment factor to account for any variability in consumption pattern during the day of the DR ev ent from the past. Current methods to establish the baseline raise several concerns. One major concern is that the consumers have an incentive to artificially inflate their baseline to increase their profits [9]–[12]. Cases hav e been reported where the participants artificially inflated their baseline for increasing payments [13]. Fairness can also be a concern. Consider, for instance, an agent who happens to be on v acation during a DR event and receives a payment for load reduction without suffering an y hardship. This can be perceived as unfair by other agents who deliberately curtail their consumption and suffer some disutility . A. Our Contribution W e propose a setting where the System Operator (SO) recruits DR providers as an alternate resource to balance supply and demand during high price periods. The providers could be either individual consumers or aggre gators of DR services. W e also assume that the SO has access to market outcomes, which is a reasonable assumption. The objectiv e of the SO is to minimize cost when energy purchase from the wholesale energy market is expensi ve. This usually happens 2 during peak load scenarios, when the market price exceeds a threshold market clearing (TMC) price. The TMC price is the price abov e which it is profitable for the SO to call the recruited DR providers or consumers to provide load reduction. The main aspects of the DR mechanism we propose are: (i) self-reported baseline (ii) randomized selection of con- sumers, and (iii) penalty for uninstructed deviations. In this mechanism, the consumers are required to self-report their baselines and are paid at a pre-determined re ward for ev ery unit of reduction the y provide. A large group of consumers is recruited so that the necessary load reduction is delivered reliably . When a DR ev ent occurs, consumers are selected randomly from this pool of recruited consumers to pro vide the required service. The load reduction is measured by the difference between the self-reported baseline and the measured consumption. The consumers signaled to reduce are paid in proportion to the measured reduction and the prescribed rew ard. The consumers who are not called are penalized for uninstructed de viation from the baseline. This penalty and randomized selection controls baseline inflation. The proposed DR program requires only baseline information from the individual consumers, which makes it minimal in terms of the information it elicits from the consumers. In this paper , we characterize baseline inflation for a quadratic utility function with uncertain consumption and a quadratic penalty function with and without a deadband. The deadband in the penalty function is required to achieve individual rationality . Using this characterization, we show that the proposed mechanism controls baseline inflation. W e also justify that by choosing an appropriate calling probability , which depends on the recruitment cost, the SO can signficantly reduce its costs. Finally , we show that the self-reported base- line establishes a better estimate of the mean baseline when compared to con ventional methods such as the CAISO’ s m/m method [8]. Since the excess payments made to the consumers are proportional to the baseline used in a DR program, this establishes that the self-reported baseline approach is more cost effecti ve than the CAISO approach. T wo concerns can arise with the self-reported baseline idea. One is the fatigue in reporting a baseline and the other is the lack of kno wledge of one’ s o wn baseline. Notwithstanding, self-reported baseline is still a viable method. This is because, firstly , the proposed mechanism is for peak load scenarios which are rare events. Secondly , we expect a energy man- agement system to manage the load consumption pattern of a consumer in the future. Gi ven the consumer’ s preferences, this energy management system should have the capability to estimate the baseline and report it to the operator or the load serving entity . In addition to all of the above aspects, the self-reported baseline DR mechanism can also av oid bias and inflation in its estimate of the baseline. B. Related W ork There exists substantial literature on baseline estimation methods [14]–[18], [18]–[23]. These can be broadly classified into three classes: (a) av eraging, (b) regression, and (c) control group methods. A veraging methods determine baselines by averaging the consumption on past days that are similar ( e.g., in weather conditions) to the e vent day . A detailed comparison of dif ferent av eraging methods is offered in [14], [15], [17]. A veraging methods are simple but they suf fer from estimation biases [17]–[19], and require a significant amount of data, especially for residential DR programs [18]. Re gression methods estimate a load prediction model based on historical data which is then used to predict the baseline [16], [21]. They can potentially overcome biases incurred by av eraging methods [18], [24]. But they often require considerable historical data for acceptable accuracy , and the models may not capture the complex behavior of indi vidual consumers. Contr ol gr oup methods have been suggested to hav e bet- ter accuracy than averaging or regression methods and do not require large amounts of historical data [22]. Ho we ver these methods require the SO to recruit an additional set of consumers and also install additional metering infrastructure for these consumers. In addition, prior data based analysis, to identify the most appropriate control group, might be required depending on the control group method deployed. This raises their costs of implementation [22]. W e also show later that the adverse incenti ves to inflate still persists in this method. Compared to all the above methods, the proposed self-r eported baseline av oids all of these issues, i.e . (i) bias and inflation, (ii) need for historical data, and (iii) high implementation cost. In order to av oid baseline estimation, in a previous work [25], we addressed the DR problem as a mechanism de- sign problem. The setting considered in [23] has an aggregator and an Utility or SO. The Utility determines the required load reduction D kWh that is to be deliv ered by the aggregator based on the system requirements. The aggregator recruits consumers to deliv er the required reduction. The mechanism that we proposed for the aggre gator requires the consumers to report both their marginal utility and their baseline consump- tion. The aggregator uses the marginal utility reports to select consumers such that its ov erall cost is minimized while the load reduction target D is met. A drawback of this mechanism in terms of implementation is that the consumers need not ha ve knowledge of their true marginal utilities. The ne w approach proposed here also av oids baseline es- timation by requiring the consumers to report their baseline consumption, but the individual marginal utility need not be disclosed. The mechanism is minimal in terms of the information it elicits from the consumers because it does not require either historical data or any additional infrastructure. The authors in [26] use a similar problem formulation to ours and propose an incenti ve based DR mechanism, but do not address how the reward price is set, how the consumers are selected so that the DR service is deliv ered reliably and the cost aspect of the mechanism. In addition they also ignore any randomness in the consumption of the consumers. Here, we consider all of the abo ve aspects and the randomness in consumption. W e also pro vide comparison with other baseline estimation methods. While some parallels can be drawn with dynamic pricing based DR mechanisms [27]–[29], the setting we consider 3 T ABLE I N OTA T I O N q Energy consumption of consumer θ Exogenous random variable u Utility of consumer expressed in monetary units π 0 Retail price of energy π 2 Rew ard/kWh awarded to consumer k f Baseline report of consumer π ∗ Threshold Market Clearing Price (TMC) p Probability of consumer being signaled R Rew ard function for load reduction Φ Penalty function for deviation from baseline Π In verse supply function Q 0 Peak load Q ∆ Q ∗ Q 0 Π( Q ) π ∗ Fig. 1. Inverse Supply Curve and Threshold Market Clearing (TMC) Price π ∗ here is dif ferent. These mechanisms essentially influence con- sumers by using time varying prices to alter their energy con- sumption so that system objectiv es are met. On the contrary , the central problem we consider is to recruit DR resources that can deliv er a certain amount of load reduction at certain times of a month which coincides with peak load conditions. This requires the estimation of consumer baseline because measuring load reduction requires a baseline. Hence baseline estimation becomes a primary concern in our setting whereas such a requirement does not arise in the dynamic pricing DR setting. The remainder of this paper is organized as follo ws. In Section II, we introduce the consumer model and the incentiv e- based self-reported DR program. In Section III, we solve for the optimal consumer forecast and characterize baseline inflation for a quadratic utility function and a quadratic penalty with and without deadband. In section IV we discuss SO’ s cost. In Section V, we compare self-reported baseline with other con ventional baseline estimation methods. Finally , we conclude in Section VI. I I . P R O B L E M S E T U P In this section, we describe the market model, the consumer model and the incentiv e-based DR program. A summary of the notations is giv en in T able I. A. Market Model The market model is represented by the wholesale market’ s in verse supply function Π( Q ) which provides the energy price as a function of the net energy transacted in the wholesale market, see Fig. 1. The market in verse supply function is assumed to be con vex with respect to Q and monotone in- creasing, i.e . with positi ve deriv ativ e Π 0 ( Q ) > 0 . The thr eshold market clearing price π ∗ (TMC price), as defined earlier , is the market price above which it is profitable for the SO to call the consumers. Gi ven the in verse supply curve of the market, this price can be computed a priori. In scenarios where the in verse supply function is not av ailable a priori, the SO can estimate it using data from past twelve months. This is typical of many system operators such as the CAISO which publishes threshold market clearing prices for the next tar get month using data from past twelve months. The assumption we make is that this estimate is reflectiv e of the true TMC price. Note that the calculation of the TMC price from the in verse supply function may not be straightforward for a network model. This would require a detailed analysis of how the congestion constraints influence the Locational Marginal Prices (LMPs) of the nodes and is model specific. The main results of this paper will still hold provided π ∗ , i.e. the threshold market clearing price for a node in the network, is determined via the network model. It is beyond the scope of this paper to discuss in detail the determination of this price under such more complicated settings. The main goal of this paper is to illustrate the idea of self-reported baseline and its effecti veness. B. Consumer Model Consider a residential consumer whose consumption is denoted by q . Let θ be a random variable that is drawn from a continuous distribution. The utility of consumption of a consumer depends on this random v ariable. W e assume that the distribution of θ includes ev ery possible source of uncertainty . For example, θ could represent the consumer’ s state where the consumer could either be at home or not. It could also model the randomness induced due to external weather conditions like temperature. Let the priv ate utility function which is expressed in monetary units be u ( q , θ ) , which is assumed to be a strictly concave monotone increasing in q . W e also assume that the random variable θ is realized at the time when consumption is accomplished. Define the marginal utility µ ( q , θ ) as follows: µ ( q , θ ) = ∂ u ( q , θ ) ∂ q . (1) Note that since u ( q , θ ) is monotone increasing and strictly concav e in q , we hav e: ∀ q : µ ( q , θ ) > 0 , ∂ µ ( q , θ ) ∂ q < 0 . C. Incentive-Based Demand Response Pr ogr am The SO signals a DR event when the market price exceeds the TMC price. The no vel DR program that we propose comprises a self-r eported baseline mechanism . The mechanism has two stages which are as follows. Stage 1 (Reporting): In this stage, the consumer self reports its baseline f and the SO announces the following quantities: 1) the probability p of calling a consumer , 2) the reward function R ( π 2 , f , q ) for reducing consump- tion ( f − q ) , 4 3) re ward per unit reduction π 2 which is equal to the TMC price π ∗ , 4) the penalty function Φ( f , q ) for consumers who deviate from their reported baseline when they are not called for DR service. This penalty function Φ is critical to ensure that the consumers do not inflate their baseline report. At the same time, the penalty should not discourage participation by pre venting lack of profitability for the participants. Based on the reward per unit reduction π 2 and the penalty Φ( f , q ) , each consumer submits the baseline report f . Stage 2 (DR Event): In the second stage, a DR event is triggered when the SO expects the market price to shoot abov e the TMC price. The SO then selects randomly from the pool of recruited consumers and the selected consumers are signaled to reduce consumption. The SO observes the aggregated consumption Q of those selected consumers. By the mechanism, the consumers who are signaled and reduce consumption are paid π 2 per unit of reduction. Howe ver , those recruited consumers that are not signaled are penalized for deviating from their reported baseline as prescribed by the penalty function. 1) Consumer Recruitment and Selection: The objectiv e of SO is to minimize its cost during DR ev ents. During a DR ev ent, the load is at its peak Q 0 , and is desirable to achieve a load reduction of ∆ Q ∗ , which is the optimal load reduction (Refer Fig. 1). The SO recruits n sets of consumers. The recruitment is such that each set of consumers reduces load by ∆ Q ∗ for the specified re ward/kWh π ∗ . The consumers are tested before they are recruited. Here, the assumption is that the aggregate load reduction can be more reliably established than the individual load reduction which requires a reliable baseline estimate. Since the probability of selection or calling of each indi vidual consumer is restricted to probability p , the number n of such sets of consumers recruited satisfies np = 1 . When a DR ev ent occurs, one set is randomly chosen and its members are signaled to reduce consumption. This recruitment and selection process ensures that one set is always chosen. Hence, the required lev el of reduction ∆ Q ∗ is deliv ered during all DR events while satisfying the calling probability of each recruited consumer . It is inconceiv able that each set of consumers will exactly deliv er ∆ Q ∗ amount of reduction at the prescribed re ward. Hence, in the proposed mechanism, the SO is allowed to adjust the selected consumers within the DR e vent windo w . If the price remains higher than the TMC price within the DR e vent then the SO can call more consumers till the price falls to the desired level. Note that this does require the SO to recruit some set of consumers who can respond on short notice. Such type of consumers can be recruited under the flexible resour ce category . Here, we provide a very simple example to illustrate ho w the consumers are grouped and selected. Consider the case where the consumers are identical and have a capacity to deliver 0 . 5 kWh of reduction when paid at π ∗ = $0 . 05 / kWh. Let the probability of calling a consumer be p = 0 . 1 and the optimal load reduction ∆ Q ∗ = 10 kWh. Then the SO would recruit n = 1 /p = 10 groups each with a capacity to deliv er 10 kWh of reduction when paid at π ∗ = $0 . 05 / kWh. This implies that each of these groups would contain 20 such consumers and each of these groups will be called or selected by the probability p = 0 . 1 when a DR ev ent occurs. Remark 1. As stated earlier , for an incentive-based demand r esponse pr ogram, determining the right baseline is very important as baseline can not be measured. In our mechanism, consumers self-r eport their baseline. No other information fr om consumers is needed other than baseline r eport. Hence, our mechanism is minimal in the information it elicits fr om the consumers. 2) Rewar d and P enalty Function: The re ward function in the mechanism is set as R ( π 2 , f , q ) = π 2 ( f − q ) , if consumer is called, 0 , otherwise. (2) Thus, the SO pays the consumers according to the measured reduction f − q , where f is the consumer’ s baseline report and q is the measured consumption during the DR e vent. The rew ard per unit reduction is π 2 . The consumer’ s penalty function is specified as follo ws, Φ( f , q ) = 0 , if consumer is called, φ ( f − q ) , otherwise. (3) where the penalty function φ in (3) is chosen to be con vex, symmetric, and nonnegati ve with minimum value zero at the origin, i.e. it satisfies the following conditions: φ (0) = φ 0 (0) = 0 , ∀ x : φ ( x ) = φ ( − x ) , φ 00 ( x ) > 0 , (4) where φ 0 and φ 00 denote the first and second deriv ative of the penalty function φ . D. Consumer’ s Optimization Pr oblem The minimum expected cost incurred by a consumer is a function of the baseline report f and is given by H ( f ) = E θ min q { π 0 q − u ( q , θ ) + Φ( f , q ) − R ( π 2 , f , q ) } . (5) The consumer’s pr oblem is formulated as follows: CP: min f H ( f ) . (6) Hence, the consumer’ s problem is a two stage stochastic decision problem. In the first stage the consumer decides the optimal baseline report f , and in the second stage decides the optimal consumption q . Definition 1. Let f ∗ be defined as the baseline report that minimizes the cost that is incurr ed by the consumer , i.e. f ∗ = arg min H ( f ) . I I I . O P T I M A L BA S E L I N E R E P O RT A N D I N FL AT I O N In this section, we deri ve an optimality condition for the consumer baseline report that minimizes the expected cost of the consumer . The optimality condition has a nice economic interpretation because it establishes that the baseline report that 5 minimizes the expected cost is such that the mar ginal utility of the consumers equals the retail price of the electricity . The consumer’ s optimization problem CP gi ven by (6) is a two-step stochastic decision problem. W e characterize con- sumers’ s consumption decisions corresponding to the second stage problem and then obtain the optimality condition for the consumer’ s baseline report by solving the first stage problem. A. The Consumer’ s Second Stage Pr oblem The consumer has several choices. It can decide to partici- pate or not to participate in the DR program. If it decides to participate, then it can be signaled to reduce its consumption or not signaled. This gi ves rise to three possible scenarios for the second stage: a) consumer is not participating in the DR program, b) consumer is participating in the program but is not signaled to reduce consumption, c) consumer is participating in the program and is signaled to reduce consumption. W e obtain the optimal consumption for each of the three cases assuming that the baseline report f is given. The consumption when the consumer is not participating corresponds to the true baseline. Hence, we use this value as the baseline to characterize inflation in the DR program. a) Consumer is not participating in the DR pr ogram: In this case, R = 0 and Φ = 0 . Let J a ( q , θ ) denote the realized cost function for this case. It is then given by J a ( q , θ ) = π 0 q − u ( q , θ ) , (7) where π 0 is the retail price of electricity . The optimal con- sumption is giv en by q a ( θ ) = arg min q J a ( q , θ ) , which is a function of θ because its value is realized when the consumption decision is made. Note that q a ( θ ) is the solution of the first order optimality condition, π 0 − ∂ u ( q , θ ) ∂ q = 0 . (8) Hence, q a ( θ ) is given by q a ( θ ) = µ − 1 ( π 0 , θ ) , (9) where µ − 1 denotes the in verse function of the marginal utility , see (1), that alw ays e xists for ev ery θ . Moreover , since the consumer’ s utility is monotone increasing and concav e in q , the consumption q a ( θ ) is always nonnegati ve. b) Consumer is participating in the pr ogram but is not signaled to r educe consumption: The reward and penalty functions are given by (2) and (3). Let J b ( f , q ) denote the realized cost function which is given by J b ( f , q , θ ) = π 0 q − u ( q , θ ) + φ ( f − q ) . (10) As before, the v alue of θ is realized when the consumption decision is made. In this scenario the realized cost is also a function of the baseline report f in addition to the consumption decision and the value of θ . The optimal consumption is giv en by q b ( f , θ ) = arg min q J b ( f , q , θ ) , and so it satisfies the first order optimality condition, π 0 − ∂ u ( q , θ ) ∂ q − φ 0 ( f − q ) = 0 . (11) Hence, the optimal consumption satisfies the following im- plicit equation, q b ( f , θ ) = µ − 1 ( π 0 − φ 0 ( f − q b ( f , θ )) , θ ) , (12) and q b ( f , θ ) is also a function of f because the de viation from f incurs a penalty . c) Consumer is participating in the pr ogr am and is sig- naled to r educe consumption: Again, the reward and penalty functions are gi ven by equations (2) and (3), respectiv ely . Let J c ( q , θ ) denote the realized cost function which is giv en by J c ( q , f , θ ) = π 0 q − u ( q , θ ) − π 2 ( f − q ) . (13) The optimal consumption is gi ven by q c ( f , θ ) = arg min q J c ( f , q , θ ) . So q c ( f , θ ) is the solution of π 0 − ∂ u ( q , θ ) ∂ q + π 2 = 0 . (14) Hence, the optimal consumption q c is independent of f and is given by q c ( θ ) = µ − 1 ( π 0 + π 2 , θ ) . (15) The relation between the consumptions for the three dif fer- ent cases q a ( θ ) , q b ( θ , f ) , q c ( θ ) and the consumer’ s baseline report f are stated in the following lemma. Lemma 1. The optimal consumptions for the three cases q a ( θ ) , q b ( θ , f ) , q c ( θ ) satisfy the conditions (i) q c < q a and (ii) q a < q b < f or f < q b < q a for every θ . Pr oof. Refer Appendix. As a result of Lemma 1, a rational consumer that is partic- ipating in the DR program and is signaled always provides a load reduction with respect to its true baseline consumption q a . Howe ver , according to this lemma, a consumer that is participating and not signaled for reduction may inflate its consumption near to its inflated baseline report to avoid the penalty and gain from the inflated baseline when called for reduction. This behaviour needs to be controlled. B. The Optimal Baseline Report Let p denote the probability that the consumer is signaled to reduce when a DR ev ent occurs. The expected cost that is incurred by the consumer (5) can be expressed in terms of the probability p as follows: H ( f ) = p E θ J c ( f , q c , θ ) + (1 − p ) E θ J b ( f , q b , θ ) , (16) and it follows that the optimal baseline report f ∗ mini- mizes this H ( f ) . In the following lemma, we show that the consumer’ s expected cost H ( f ) is a con vex function of its argument f . 6 Lemma 2. The consumer’ s expected cost H ( f ) is a (strictly) con vex function of its argument f if and only if the penalty φ is (strictly) con vex. Pr oof. Refer Appendix. Since the penalty function φ was chosen to be conv ex, the consumer’ s expected cost H ( f ) is also con ve x. Definition 2 (Consumer’ s Expected Marginal Utility) . The consumer’ s expected mar ginal utility under the incentive- based self-reported DR pr ogram is given by M ( f ) = p E θ ∂ u ( q c , θ ) ∂ q + (1 − p ) E θ ∂ u ( q b , θ ) ∂ q . (17) The consumer’ s expected marginal utility is a function of the baseline report f , because the consumption q is a function of f . For example, if the consumer is participating in the DR program and is signaled, then its consumption is q b ( f , θ ) which solves the implicit equation (12) and does depend on f . The following theorem establishes the optimality condition for the optimal baseline report f ∗ in terms of M ( f ) , Theorem 1. The optimal baseline r eport f ∗ satisfies π 0 = M ( f ∗ ) and is a global minimizer of the cost function H ( f ) . Mor eover , the minimizer is unique when φ is strictly con vex. Pr oof. Refer Appendix. The optimality condition obtained in Theorem 1 has a nice interpretation from the classical consumer theory in economics [30]. The optimal baseline report f ∗ is such that the consumer’ s marginal utility equals the retail price of the electricity . Given f ∗ , the expected rew ard per unit of energy (in kWh) paid for the expected load reduction provided by a consumer is giv en by π ∗ ( f − E θ q c ( θ )) E θ q a ( θ ) − E θ q c ( θ ) = π ∗ + π ∗ E θ δ f ( θ ) E θ q a ( θ ) − E θ q c ( θ ) , (18) where δ f ( θ ) = f − q a ( θ ) is defined to be the inflation of the baseline report. From the second term, we infer that the expected inflation of the baseline report should be small to av oid a large excess payment. C. Contr ol of Baseline Inflation Here, we sho w that the penalty function in combination with randomized calling allows the SO to control the inflation of the optimal baseline report δ f ∗ ( θ ) = f ∗ − q a ( θ ) . First we establish that penalty is necessary and then sho w that with a penalty , the probability of calling p pro vides us a lever to control baseline inflation. 1) Optimal Baseline Report without P enalty: In this case, the optimality condition for the optimal baseline report f ∗ is giv en by dH ( f ) d f = p E θ dJ c ( f , q c , θ ) d f = − pπ 2 . (19) Since the sensitivity of the consumer’ s cost H ( f ) is negati ve with respect to f , it indicates that the consumer will report a very high baseline. 2) Optimal Baseline Report with P enalty: The introduction of a penalty function allo ws us to control the inflation in the baseline report by adjusting the probability of calling. This result is shown in the following lemma. Theorem 2. Let the penalty function φ be a quadratic function such that ∀ x : φ 00 ( x ) = 1 /λ . Then the measurable inflation in the optimal baseline r eport δ ˜ f ∗ ( θ ) = f ∗ − q b ( f ∗ , θ ) satisfies lim p → 0 E θ δ ˜ f ∗ ( θ ) = 0 . And when ∂ u 2 ( q ,θ ) ∂ q 2 = − 1 /d , lim p → 0 E θ δ f ∗ ( θ ) = 0 . Pr oof. Refer Appendix. For specific consumer utility and penalty functions, an ex- plicit expression for the expected baseline report inflation can be obtained. The following theorem provides this expression for the case where the consumer’ s utility and the penalty function are both quadratic. Theorem 3. Let the consumer’ s utility u and the penalty function φ be quadratic functions such that i) ∀ ( q , θ ) : ∂ u 2 ( q ,θ ) ∂ q 2 = − 1 /d , ii) ∀ x : φ 00 ( x ) = 1 /λ , wher e d and λ are positive scalars, then the expected inflation of the baseline r eport is given by E θ δ f ∗ ( p ) = f ∗ − E q a ( θ ) = ( d + λ ) pπ 2 1 − p . (20) Pr oof. Refer Appendix. The law of diminishing marginal utility establishes that the marginal utility declines with increase in consumption [30]. In Theorem 3, 1 /d is the rate of diminishment of the consumer’ s marginal utility , and it is a priv ate feature of the consumer that cannot be modified by the system operator . Unlike d , λ is a parameter of the DR program, because it defines the quadratic penalty function, i.e. φ ( x ) = x 2 / (2 λ ) . Hence, the SO can choose λ in the design of the DR program. Since λ > 0 , a lower bound for the e xpected inflation of baseline report is obtained by setting λ = 0 , E θ δ f ∗ = f ∗ − E θ q a ( θ ) ≥ dpπ 2 1 − p . (21) Moreov er , by choosing the parameter of the penalty function λ to be small enough, the expected inflation of the baseline report can be made arbitrarily close to its lower bound. Note that this lower bound is a function of p and is decreasing with p . Consequently , by choosing λ and p to be small the baseline inflation can be controlled. Here, we provide a simple numerical example to v alidate the abo ve results. In this example, u = cq − (0 . 5 /d ) q 2 , where c = $ . 5 / kWh and d ∈ { 0 . 1 , 0 . 2 , 0 . 3 , 0 . 4 } in ($ / kWh 2 ) − 1 . The retail price π 0 = $0 . 12 / kWh and the TMC price π ∗ = $0 . 05 / kWh and are typical v alues (Refer [31]). These set of parameter v alues correspond to a typical price sensi- tivity value of ∼ − 0 . 3 [32], [33]. The penalty coefficient λ = 0 . 1 ($ / kWh 2 ) − 1 . The probability p is chosen to be 7 q Φ( q ) 2 f Fig. 2. Penalty function with deadband p = 0 . 1 . T able II summarizes the simulation results and how it compares with the theoretical results for this example. T ABLE II B A S E LI N E I N FLAT IO N , δ f ∗ d 0.1 0.2 0.3 0.4 δ f ∗ (theory) 0 . 0011 0 . 0017 0 . 0022 0 . 0028 δ f ∗ (simul.) 0 . 0012 0 . 0017 0 . 0023 0 . 0028 D. Ensuring Individual Rationality with a Deadband The DR program is not guaranteed to be individually rational from the point of vie w of a single consumer because of the presence of uncertainty θ . When a consumer is not called, it consumes q b ( f , θ ) which varies with θ and is different from f , as it was shown in Lemma 1. As a result the consumer incurs a penalty and the mechanism is not guaranteed to be individually rational. This is not an issue in the absence of uncertainty . Indi vidual rationality of the program can be ensured by introducing a deadband in the penalty as illustrated in Figure 2. A penalty with deadband can be expressed as, φ ( f − q ) = ( ( | f − q |− ) 2 2 λ , if | f − q | ≥ , 0 , otherwise. (22) It is evident from such a design that there exists a deadband width such that the mechanism is individually rational. But a deadband worsens the inflation in baseline. In the theorem below , we provide an upper bound for the inflation in baseline when the penalty function has a deadband. The upper bound explicitly prov es that the baseline inflation can worsen with the introduction of a deadband. But this trade off has to be made to guarantee individual rationality . Theorem 4. Let the consumer’s utility u be a quadratic function such that ∀ ( q , θ ) : ∂ u 2 ( q , θ ) ∂ q 2 = − 1 /d. The penalty function φ is defined in (22) , wher e d and λ ar e positive scalars. Let max { q max − E θ q a ( θ ) , E θ q a ( θ ) − q min } ≤ , wher e q a ( θ ) ∈ [ q min , q max ] , then the expected inflation of the baseline report is bounded by E θ δ f ∗ ( p ) = f ∗ − E q a ( θ ) ≤ ( d + λ ) pπ 2 (1 − p ) + , (23) and the mechanism is individually rational. Pr oof. Refer Appendix. I V . S O ’ S C O S T The SO’ s overall cost includes four terms: the cost to pur- chase power from the wholesale market, the payment for DR services, the retail energy payments and the recruitment cost. W e ignore the recruitment cost for the initial analysis here. This allows us to mathematically deriv e an order approximate expression, with respect to p , for the resultant cost. Using this we sho w that p can be used as a le ver to control SO’ s cost as well. This allows the SO to achie ve an almost optimal cost in this case by choosing a very small value for p . W e then discuss the case where the recruitment cost is non-trivial. Here, we show that p is restricted as a lever for controlling SO’ s cost. This is because the recruitment costs becomes unbounded as p → 0 . Howe ver , we sho w , for a typical DR scenario, that the SO’ s cost is decreasing with p up to a certain threshold value. This threshold value is small enough that the cost can be significantly reduced by choosing this threshold as the selection probability . This suggests that the SO can still reduce its cost to significantly lower levels for typical DR scenarios. A. W ithout Recruitment Cost Let Q denote the net energy purchased from wholesale market, Π( Q ) the wholesale market’ s price, ∆ ˜ Q the measured net load reduction provided by the called DR resources, and π 0 the retail energy price. Then, the SO’ s overall cost, ignoring the recruitment cost, is gi ven by J S O = Π( Q ) Q + Π( Q )∆ ˜ Q − π 0 Q. (24) Let Q 0 denote the overall load had the DR resources not been called to reduce load and ∆ Q the true net reduction provided by the called DR resources, then Q 0 = Q + ∆ Q and the SO’ s cost can also be written as follows, J S O = (Π( Q 0 − ∆ Q ) − π 0 )( Q 0 − ∆ Q )+ Π( Q 0 − ∆ Q )(∆ Q + ∆ ˜ Q − ∆ Q ) , (25) where ∆ ˜ Q − ∆ Q corresponds to the inflation in net load reduction estimate, which arises from the inflation in baseline estimates of the recruited DR providers. From Theorem 3, it follows that the inflation ∆ ˜ Q − ∆ Q is O ( p ) where p is the probability of calling a consumer , which is a design v ariable of the DR mechanism. Hence, in this case, min ∆ Q,p =0 J S O = J ∗ S O , i.e., the SO’ s optimal cost can be achiev ed by driving the probability to zero. And so the optimal reduction ∆ Q ∗ = arg min ∆ Q,p =0 J S O . From the con vexity of J S O , when p is zero, it follows that ∆ Q ∗ satisfies the first order condition, ∆ Q ∗ = Q 0 − Π 0− 1 ( π 0 /Q 0 ) . (26) The market price corresponding to Q 0 − ∆ Q ∗ is exactly the TMC price π ∗ because Q 0 − ∆ Q ∗ is the optimal reduction. Consequently , ∆ Q ∗ satisfies π ∗ = Π( Q 0 − ∆ Q ∗ ) . (27) The SO recruits n = 1 /p sets of consumers such that each set can provide ∆ Q ∗ of load reduction when called for a DR 8 ev ent. Hence, the cost for the SO (25) when a particular set is called during a DR event is given by J S O = (Π( Q 0 − ∆ Q ∗ ) − π 0 )( Q 0 − ∆ Q ∗ )+ Π( Q 0 − ∆ Q ∗ )(∆ Q ∗ + ∆ ˜ Q − ∆ Q ∗ ) . (28) Using definition of J ∗ S O , J S O = J ∗ S O + Π( Q 0 − ∆ Q ∗ )(∆ ˜ Q − ∆ Q ∗ ) . (29) Substituting for baseline inflation from Theorem 3, J S O = J ∗ S O + Π( Q 0 − ∆ Q ∗ ) ¯ N ¯ d pπ 2 1 − p , (30) where ¯ N is the number of consumers in the set and ¯ d is the av erage rate of diminishment of the marginal utility across the recruited consumers in the set, which is an unknown. The SO chooses the reward rate as π 2 = π ∗ , and therefore J S O = J ∗ S O + ( π ∗ ) 2 ¯ N ¯ d p 1 − p = J ∗ S O + O ( p ) . (31) Note that with the inclusion of deadband to ensure individ- ual rationality , the SO’ s cost becomes, J S O = J ∗ S O + ( π ∗ ) 2 ¯ N ¯ d p 1 − p + π ∗ ¯ N = J ∗ S O + O ( p + ) . (32) Thus, for this case, the SO’ s cost is O ( p ) and O ( ) optimal and the SO’ s cost J S O approaches J ∗ S O when both p and approach zero. This result suggests that the SO can achiev e an almost optimal cost in this case by choosing a very small value for p . B. W ith Recruitment Cost Denote the recruitment cost per customer by π rec . Let N T be the total number of consumers recruited. Then N T is giv en by N T = n X i =1 ¯ N i , where n = 1 /p is the number of groups and ¯ N i is the number of consumers in group i . Including the total recruitment cost, which scales with N T , SO’ s overall cost is given by J S O = Π( Q ) · Q + Π( Q ) · ∆ ˜ Q − π 0 · Q + π rec · N T . (33) Note that, in this case, the optimal cost for SO J ∗ S O 6 = min ∆ Q,p =0 J S O . The reason is that the last term grows un- boundedly as p → 0 . This also suggests that, in this case, an almost optimal cost cannot be achie ved by choosing p to be very small. This is illustrated in the example below . W e provide a simple example here to illustrate how the SO’ s cost v aries with p when the recruited consumers pro vide ∆ Q ∗ reduction and when the recruitment cost is non-trivial. In the example we consider here, c = 5 × 10 2 $ / MWh, π 0 = $120 / MWh, Q 0 = 8000 MWh. W e consider two different v alues for d , i.e., d = 0 . 1 , d = 0 . 01 . The values of d are derived from demand reduction provided by typical customers assuming the payment to be $100 / MWh. The two d values correspond to large industrial customers and commer- cial places like retail stores etc. respectively [34]. W e assume 0 0.2 0.4 0.6 Probability of Calling ( p ) 0 0.5 1 1.5 2 SO Cost ($/hour) 10 5 d = 0.1 rec = $2/Customer rec = $0/Customer Optimal SO Cost 0 0.2 0.4 0.6 Probability of Calling ( p ) 0 0.5 1 1.5 2 SO Cost ($/hour) 10 5 d = 0.01 rec = $2/Customer rec = $0/Customer Optimal SO Cost 0 0.2 0.4 0.6 Probability of Calling ( p ) 0 0.5 1 1.5 2 SO Cost ($/hour) 10 5 d = 0.1 rec = $10/Customer rec = $0/Customer Optimal SO Cost 0 0.2 0.4 0.6 Probability of Calling ( p ) 0 0.5 1 1.5 2 SO Cost ($/hour) 10 5 d = 0.01 rec = $10/Customer rec = $0/Customer Optimal SO Cost Fig. 3. SO cost vs p when load reduction is ∆ Q ∗ during a DR ev ent. T op: π rec = $2 / Customer, bottom: π rec = $10 / Customer. that the supply ranges from 5000 MWh to 8000 MWh. Using the representati ve supply curve from [35] we approximate the in verse supply curve for this range by Π( Q ) = aQ + bQ 2 where a = − 0 . 0415 in $ / MWh and b = 8 . 3 × 10 − 6 in $ / MWh 2 . For this supply curve and Q 0 = 8000 MWh, π ∗ ∼ $100 / MWh and ∆ Q ∗ ∼ 1200 MWh. The reward payment of $100 / MWh and the aggregate load reduction of 1200 MWh are typical of DR programs spanning the region cov ered by a SO [36]. The first two plots of Figure 3 provides the variation of SO’ s cost with respect to p when the recruitment cost is π rec = $2 / Customer for different v alues of d and the bottom row plot of Figure 3 provides the variation of SO’ s cost when the recruitment cost π rec = $10 / Customer. The former recruitment cost, i.e. π rec = 2 , is based on typical service costs charged per customer on a monthly basis to recover the metering implementation and maintenance cost [37]. In our case, we consider the worst-case scenario where the SO bears this cost instead of passing it on to the DR participants. Note that the approximation of the SO’ s cost by ignoring recruitment cost, as in the pre vious section, is a reasonable approximation of the SO’ s cost up to a certain threshold probability . This threshold probability is as low as 0 . 1 and 0 . 2 for the cases d = 0 . 1 and d = 0 . 01 respectively . These d values and other parameter values are typical v alues as stated before. Hence we expect that, in a typical scenario such as this, a SO can still reduce its cost significantly by setting the calling probability equal to this threshold value. V . S E L F - R E P O RT E D B A S E L I N E V S . O T H E R B A S E L I N E E S T I M A T I O N M E T H O D S Here, we shall use the CAISO m/m method [8] for our comparativ e study . W e emphasize here that a similar analysis applies to other estimation methods like control group meth- ods. In CAISO’ s m/m method, the SO computes the av erage consumption of the most recent m similar but non-e vent days and uses this av erage-based estimate as the baseline. Hence, 9 the baseline estimate is a moving av erage of the consumption profile of the consumers. T ypically this average-based estimate from past consumption data is corrected by an adjustment factor to account for any v ariation in the consumption pattern from the past. This adjustment f actor is common to all baseline estimation methods and is highly recommended. As we shall see this factor is the primary cause for the existence of adverse incentiv es to inflate baseline. Hence, the analysis to follow equally applies to all current baseline methods that use an adjustment factor , which includes the control group methods. As discussed before, the individual optimal consumption decision depends on whether the consumer is signaled or not for reduction on a particular day . Also the baseline estimate used for the payments depends on the consumption in the days prior to the DR ev ent. So the payments made during future DR ev ents can influence the consumer to inflate their consumption during a non-ev ent day . On a particular day , the consumer’ s benefit depends on whether the consumer is signaled or not. As explained in Section III-A, if the consumer is participating in the DR program and is signaled to reduce, its total cost is J c ( q , f , θ ) given by (13) where f is the baseline estimate obtained by the CAISO m/m method. Howe ver , if the consumer is not signaled, its cost is J a ( q , θ ) (see equation 7). Unlike the incentive-based DR program with self-reported baseline, the CAISO program does not impose a penalty , and the consumer’ s cost is the same as if it were not participating in the DR program, when it is not called. Let T N denote the set of most recent m similar but non- ev ent days, and let f c denote the baseline calculated in CAISO’ s m/m model. Then, f c = 1 m X τ ∈T N q τ , (34) where { q τ : τ ∈ T N } is the set of consumption for the near past m similar non-ev ent days. The baseline estimation f c is multiplied by an adjustment factor C f to account for any variation in the consumption pattern. Hence, the CAISO baseline with adjustment factor is giv en by ¯ f c = f c C f , where f c was defined in (34). Let q denote the consumption on the current DR ev ent day , and q − the consumption on the day before. Let T E be the set of days before the days in the set T N , and define f − = 1 m P τ ∈T E q − τ as the average consumption of the days in the set T E . The correction factor for the current DR day is then computed as C f = q − f − . (35) T ypically , the consumers are signaled a day ahead of the DR e vent. So, the reward during the DR e vent on the cur- rent day can influence the consumer to inflate its day-ahead consumption q − . The day-ahead consumption is obtained by minimizing the joint cost of the current DR day and the day before with respect to q − , as these are the only two terms in the ov erall cost of the consumer that q − can influence. The joint cost for the two days is giv en by J a ( q − , θ ) + J c ( q , θ ) , where J a ( q − , θ ) = π 0 q − − u ( q − , θ ) , J c ( q , ¯ f c , θ ) = π 0 q − u ( q , θ ) − π 2 ( ¯ f c − q ) . Here, for illustration purposes, we hav e assumed identical utility functions and retail price for both the days. The analysis can be trivially extended to the general case where they are not identical. The term π 2 ( ¯ f c − q ) is the payment that the consumer recei ves for reducing consumption and the value of θ is realized when the consumption decision is made. By definition it follo ws that the optimal consumption q −∗ on the day before the current DR ev ent day is giv en by q −∗ ( θ , ¯ f c ) = arg min q − ( J a ( q − ) + J c ( q , ¯ f c )) . (36) From the first order optimality condition it follows that q −∗ should satisfy π 0 − µ ( q − , θ ) − π 2 ∂ ¯ f c ( q − ) ∂ q − = 0 . (37) On the DR ev ent day , f c and f − are constants. This implies, ∂ ¯ f c ( q − ) ∂ q − = f c f − . (38) Hence, the optimal consumption on the day before the current DR event day is q −∗ ( θ ) = µ − 1 π 0 − π 2 f c f − , θ . (39) Using this result, we provide a lower bound for the expected value of baseline inflation in the CAISO m/m method with adjustment factor , when the utility function is quadratic, in the following lemma. Lemma 3. Let the consumer’ s utility u be a quadratic function such that ∀ ( q , θ ) : ∂ u 2 ( q ,θ ) ∂ q 2 = − 1 /d wher e d is a positive scalar , then the baseline r eport ¯ f c satisfies E θ ( ¯ f c − q a ( θ )) > dπ 2 . (40) Pr oof. Refer Appendix. In the proposed DR mechanism, the expected baseline infla- tion with quadratic utility and penalty function was obtained in Theorem 4. From the discussion in the pre vious two sections, it follo ws that λ and p can be used as lev ers to control baseline. Hence by choosing λ and p to be sufficiently small and provided is not comparable to dπ 2 , which is the case when π 2 ∼ O ( π 0 ) , we get that E θ ( f ∗ − q a ( θ )) dπ 2 < E θ ( ¯ f c − q a ( θ )) . (41) Thus, in the self-reported approach, we can ensure that the inflation in baseline per consumer is significantly smaller compared to con ventional baseline estimation methods, such as CAISO’ s m/m method, that uses an adjustment factor . V I . C O N C L U S I O N W e proposed a mechanism for incenti ve-based DR pro- grams where the only information that is elicited from each 10 consumer is a self-report of its baseline consumption. The mechanism entails a calling probability for each consumer and a penalty when the consumer is not called. The mechanism provides the required service reliably by selecting a certain set of consumers during e very DR e vent. W e showed that the probability of calling and the penalty can be used to control the baseline inflation. W e also justified that the mechanism’ s cost can be significantly reduced by deploying DR resources. Finally , we showed that the self-reported baseline estimates a better baseline estimate than conv entional methods such as the CAISO’ s m/m method. R E F E R E N C E S [1] M. H. Albadi and E. El-Saadany , “ A summary of demand response in electricity markets, ” Electric power systems resear ch , vol. 78, no. 11, pp. 1989–1996, 2008. [2] F . E. R. Commission, “Demand response compensation in organized wholesale energy markets, ” F inal Rule Report , 2011. [3] C. D. W . Paul L. Joskow , “Dynamic pricing of electricity , ” The American Economic Revie w , vol. 102, no. 3, pp. 381–385, 2012. [Online]. A vailable: http://www .jstor .org/stable/23245561 [4] P . Chakraborty , E. Baeyens, and P . P . Khargonekar , “Distributed control of flexible demand using proportional allocation mechanism in a smart grid: Game theoretic interaction and price of anarchy , ” Sustainable Ener gy , Grids and Networks , vol. 12, pp. 30–39, 2017. [5] J. L. Mathieu, T . Haring, J. O. Ledyard, and G. Andersson, “Residential demand response program design: Engineering and economic perspec- tiv es, ” in European Energy Market (EEM), 2013 10th International Confer ence on the . IEEE, 2013, pp. 1–8. [6] S. Borenstein, M. Jaske, and A. Ros, “Dynamic pricing, advanced metering, and demand response in electricity markets, ” Journal of the American Chemical Society , vol. 128, no. 12, pp. 4136–45, 2002. [7] A. Faruqui and J. Palmer , “Dynamic pricing and its discontents, ” Re gulation , vol. 34, no. 3, pp. 16 – 22, 2011. [8] CAISO, Demand Response User Guide. V ersion 4.3 , California ISO, May 2017. [9] H. Chao, “Price-responsi ve demand management for a smart grid world, ” The Electricity Journal , vol. 23, no. 1, pp. 7–20, 2010. [10] F . A. W olak, “Residential customer response to real-time pricing: The anaheim critical peak pricing experiment, ” Center for the Study of Ener gy Markets , 2007. [11] H. P . Chao and M. DePillis, “Incentive ef fects of paying demand response in wholesale electricity markets, ” Journal of Regulatory Eco- nomics , vol. 43, no. 3, pp. 265–283, 2013. [12] J. V uelvas and F . Ruiz, “Rational consumer decisions in a peak time rebate program, ” Electric P ower Systems Researc h , vol. 143, pp. 533– 543, 2017. [13] J. Pierobon. (2013) T wo FERC settlements illustrate at- tempts to ‘game’ demand response programs. Last accessed 2019-3-30. [Online]. A v ailable: https://www .energycentral.com/c/ec/ ferc- settlements- illustrate- attempts- game- demand- response- programs [14] K. Coughlin, M. A. Piette, C. Goldman, and S. Kiliccote, “Estimating demand response load impacts: Ev aluation of baseline load models for non-residential buildings in california, ” Lawrence Berkele y National Laboratory , 2008. [15] C. Grimm, “Evaluating baselines for demand response programs, ” in AEIC Load Researc h W orkshop , 2008. [16] J. L. Mathieu, P . N. Price, S. Kiliccote, and M. A. Piette, “Quanti- fying changes in building electricity use, with application to demand response, ” IEEE T ransactions on Smart Grid , vol. 2, no. 3, pp. 507– 518, 2011. [17] T . K. Wijaya, M. V asirani, and K. Aberer , “When bias matters: An economic assessment of demand response baselines for residential customers, ” IEEE T ransactions on Smart Grid , vol. 5, no. 4, pp. 1755– 1763, 2014. [18] S. Nolan and M. OMalley , “Challenges and barriers to demand response deployment and evaluation, ” Applied Energy , vol. 152, pp. 1–10, 2015. [19] Y . W eng and R. Rajagopal, “Probabilistic baseline estimation via gaus- sian process, ” in IEEE P ower & Energy Society General Meeting , 2015. [20] Y . Zhang, W . Chen, R. Xu, and J. Black, “ A cluster-based method for calculating baselines for residential loads, ” IEEE T ransactions on smart grid , vol. 7, no. 5, pp. 2368–2377, 2016. [21] X. Zhou, N. Y u, W . Y ao, and R. Johnson, “Forecast load impact from demand response resources, ” in IEEE P ower and Ener gy Society General Meeting , 2016. [22] L. Hatton, P . Charpentier , and E. Matzner-Løber , “Statistical estimation of the residential baseline, ” IEEE Tr ansactions on P ower Systems , vol. 31, no. 3, pp. 1752–1759, 2016. [23] F . W ang, K. Li, C. Liu, Z. Mi, M. Shafie-Khah, and J. P . Catal ˜ ao, “Syn- chronous pattern matching principle-based residential demand response baseline estimation: Mechanism analysis and approach description, ” IEEE Tr ansactions on Smart Grid , vol. 9, no. 6, pp. 6972–6985, 2018. [24] J. L. Mathieu, D. S. Callaway , and S. Kiliccote, “Examining uncertainty in demand response baseline models and variability in automated re- sponses to dynamic pricing, ” in 2011 50th IEEE Conference on Decision and Control and European Contr ol Conference . IEEE, 2011, pp. 4332– 4339. [25] D. Muthirayan, D. Kalathil, K. Poolla, and P . V araiya, “Mechanism de- sign for demand response programs, ” arXiv preprint , 2017. [26] J. V uelvas, F . Ruiz, and G. Gruosso, “Limiting gaming opportunities on incentiv e-based demand response programs, ” Applied Ener gy , vol. 225, pp. 668–681, 2018. [27] P . Jacquot, O. Beaude, S. Gaubert, and N. Oudjane, “ Analysis and implementation of an hourly billing mechanism for demand response management, ” IEEE T ransactions on Smart Grid , 2018. [28] M. Muratori and G. Rizzoni, “Residential demand response: Dynamic energy management and time-varying electricity pricing, ” IEEE Tr ans- actions on P ower systems , vol. 31, no. 2, pp. 1108–1117, 2016. [29] J. H. Y oon, R. Baldick, and A. Novoselac, “Dynamic demand response controller based on real-time retail price for residential buildings, ” IEEE T ransactions on Smart Grid , vol. 5, no. 1, pp. 121–129, 2014. [30] P . Krugman and R. W ells, Microeconomics , 4th ed. New Y ork: W orth Publishers, 2012. [31] U.S. Energy Information Administration. (2018) Electric po wer monthly . Last accessed 2019-3-30. [Online]. A vailable: https://www . eia.gov/electricity/monthly/ [32] C. King and S. Chatterjee, “Predicting california demand response, ” Public Utilities F ortnightly , vol. 141, pp. 27–32, 01 2003. [33] P . C. Reiss and M. W . White, “Household electricity demand, revisited, ” The Review of Economic Studies , vol. 72, no. 3, pp. 853–883, 2005. [34] S. Kiliccote, P . Gas et al. , “Installation and commissioning automated demand response systems, ” 2008. [35] E. Hausman, R. Fagan, D. White, K. T akahashi, and A. Napoleon, “Lmp electricity markets: Market operations, market po wer , and v alue for consumers, ” Synapse Energy Economics , 2006. [36] P . Interconnection, “Demand response strategy , ” Report. June , 2017. [37] E. Doris and K. Peterson, “Government program briefing: Smart me- tering, ” National Renewable Energy Lab.(NREL), Golden, CO (United States), T ech. Rep., 2011. A P P E N D I X A. Pr oof of Lemma 1 In order to prove the second statement, we note that J b ( f , q , θ ) is the sum of two conv ex functions U 1 ( q ) = π 0 q − u ( q , θ ) and U 2 ( f , q ) = φ ( f − q ) . The minimizer of U 1 is q a ( θ ) and the minimizer of U 2 is q = f . Then the minimizer of J b = U 1 + U 2 necessarily lies between the minimizers of U 1 and U 2 which implies that q b ( f , θ ) lies between q a ( θ ) and f . The first statement follows from (15), (9) and the properties of the consumer’ s utility that is monotone increasing. B. Pr oof of Lemma 2 W e start by sho wing that 0 ≤ α ( f , θ ) < 1 , where α is the cost sensitivity defined as α ( f , θ ) = dq b ( f ,θ ) d f . The optimal consumption q b ( f , θ ) satisfies (11). Holding θ fixed and differentiating (11) further we get, φ 00 ( f − q ) − ∂ 2 u ( q , θ ) ∂ q 2 dq b ( f , θ ) d f − φ 00 ( f − q ) = 0 . 11 Con vexity of φ and strict con ve xity of − u implies the e xistence of dq b d f and is giv en by α ( f , θ ) = φ 00 ( f − q b ) − ∂ 2 u ( q b , θ ) ∂ q 2 − 1 φ 00 ( f − q b ) , and satisfies 0 ≤ α < 1 . Next, we differentiate H ( f ) twice to show that H 00 ( f ) > 0 . Differentiating H ( f ) we get H 0 ( f ) = (1 − p ) E θ dJ b ( f , q b , θ ) d f + p E θ dJ c ( f , q c , θ ) d f = (1 − p ) E θ φ 0 ( f − q b ) − pπ 2 . Differentiating once again, we get H 00 ( f ) = (1 − p ) E θ (1 − α ( f , θ )) φ 00 ( f − q b ) . Before we sho wed that (1 − α ( f , θ )) > 0 . Then, it follo ws that H ( f ) is (strictly) conv ex if and only if φ is (strictly) con vex. C. Pr oof of Theor em 1 The optimal forecast f ∗ satisfies the first order condition: H 0 ( f ) = (1 − p ) E θ dJ b ( f , q b , θ ) d f + p E θ dJ c ( f , q c , θ ) d f = 0 . The sensitivity of optimal cost J b ( f , q b , θ ) with respect to f is given by dJ b ( f , q b , θ ) d f = π 0 α ( f , θ ) − ∂ u ( q b , θ ) ∂ q α ( f , θ ) − φ 0 ( f − q b )( α ( f , θ ) − 1) , where α ( f , θ ) = dq b ( f ,θ ) d f . Then, taking into account that q b ( f , θ ) satisfies (11), we get dJ b ( f , q b , θ ) d f = φ 0 ( f − q b ) . (42) The sensitivity of optimal cost J c ( f , q c , θ ) with respect to f is given by dJ c ( f , q c , θ ) d f = π 0 β ( θ ) − ∂ u ( q c , θ ) ∂ q β ( θ ) − π 2 (1 − β ( θ )) , where β ( θ ) = dq c ( θ ) d f . As before, q c ( θ ) satisfies (14) and we get dJ c ( f , q c , θ ) d f = − π 2 = π 0 − ∂ u ( q c , θ ) ∂ q . (43) From equations (42) and (43), we obtain E θ φ 0 ( f ∗ − q b ( f ∗ , θ )) = pπ 2 1 − p . (44) The optimality condition follows from equations (11) and (14) because π 0 = (1 − p ) E θ ∂ u ( q b , θ ) ∂ q + p E θ ∂ u ( q c , θ ) ∂ q . (45) The right hand side in (45) is the expected marginal utility which implies that π 0 = M ( f ∗ ) . Since φ was selected to be conv ex, from Lemma 2, f ∗ is a global minimizer of H ( f ) . Moreover , if φ is a strictly conv ex function, again from Lemma 2, f ∗ is unique. D. Pr oof of Theor em 2 From equation (44), we hav e E θ φ 0 ( f ∗ − q b ( f ∗ , θ )) = E θ 1 /λ ( f ∗ − q b ( f ∗ , θ )) = pπ 2 1 − p . This implies, lim p → 0 f ∗ − E θ q b = lim p → 0 E θ δ ˜ f ∗ ( θ ) = 0 . From the optimality condition for q b ( f ∗ , θ ) (11) and when ∂ u 2 ( q ,θ ) ∂ q 2 = − 1 /d , q b ( f ∗ , θ ) = q a ( θ ) + d/λ ( f ∗ − q b ( f ∗ , θ )) . T aking expectations on both sides we get lim p → 0 E q b ( f ∗ , θ ) = E q a ( θ ) . That is, lim p → 0 f ∗ − E θ q a = lim p → 0 E θ δ f ∗ ( θ ) = 0 . E. Pr oof of Theor em 3 The consumptions q a ( θ ) and q c ( θ ) hav e the expressions: q a ( θ ) = µ − 1 ( π 0 , θ ) , q c ( θ ) = µ − 1 ( π 0 + π 2 , θ ) . Also from (45), we get π 0 = (1 − p ) E θ ∂ u ( q b , θ ) ∂ q + p E θ ∂ u ( q c , θ ) ∂ q = (1 − p ) E θ ∂ u ( q b , θ ) ∂ q + p ( π 0 + π 2 ) . This implies, E θ µ ( q b ( θ ) , θ ) = π 0 − p 1 − p π 2 . Since the utility function u is quadratic in q , the marginal utility µ = u 0 is affine in q . Moreov er, since µ 0 is independent of the random variable θ , it holds E θ µ − 1 ( E θ µ ( q ( θ ) , θ ) , θ ) = E θ q ( θ ) , and substituting q b ( θ ) in the previous expression, we obtain E θ q b ( θ ) = E θ µ − 1 π 0 − p 1 − p π 2 , θ . The consumer’ s utility u and the penalty φ are quadratic functions, then their deriv ati ves u 0 and φ 0 are affine and their in verse functions are also affine. Moreover , the deriv ative of the inv erse functions satisfy: ∂ k ∂ x k µ − 1 ( x ) = d, if k = 1 , 0 , if k > 1 . d k dx k φ 0− 1 ( x ) = λ, if k = 1 , 0 , if k > 1 . Then, the expressions of µ − 1 π 0 − pπ 2 1 − p , θ and 12 φ 0− 1 pπ 2 1 − p become µ − 1 π 0 − pπ 2 1 − p , θ = µ − 1 ( π 0 , θ ) + d pπ 2 1 − p = q a ( θ ) + d pπ 2 1 − p , and φ 0− 1 pπ 2 1 − p = λ pπ 2 1 − p . Using (44), we get f ∗ = E θ q b ( θ ) + φ 0− 1 p 1 − p π 2 . (46) By taking expectations, E θ q b ( θ ) = E θ q a ( θ ) + d pπ 2 1 − p . (47) and by substitution in (46), we obtain f ∗ = E θ q a ( θ ) + ( d + λ ) pπ 2 1 − p . F . Proof of Theorem 4 Define a family of penalty functions with deadband as follows: φ ∆ ( x ) = 0 , if | x | < − ∆ , ( | x | + ∆ − ) 3 / (6 λ ∆) , if − ∆ ≤ | x | ≤ , ∆ 2 / (6 λ ) + ( | x | − )∆ / (2 λ ) +( | x | − ) 2 / (2 λ ) , if | x | > , for 0 ≤ ∆ < . Note that φ ∆ is continuous with continuous deriv ativ es up to second order for 0 < ∆ < , and it ap- proaches the penalty function φ giv en by (22) as ∆ approaches zero, i.e. φ = lim ∆ → 0 + φ ∆ . The deriv ati ve of φ ∆ is: φ 0 ∆ ( x ) = 0 , if 0 ≤ x < − ∆ , ( x + ∆ − ) 2 / (2 λ ∆) , if − ∆ ≤ x ≤ , ∆ / (2 λ ) + ( x − ) /λ, if x > . for x ≥ 0 and φ 0 ∆ ( x ) = − φ 0 ∆ ( − x ) for x ≤ 0 , which is in vertible for any x 6 = 0 . From the fact that this penalty function is double dif fer- entiable, the optimality conditions established before hold for this specific case as well. W e do a case based analysis. Case f ∗ ≥ E θ q a ( θ ) + : From Lemma 1 we have that f ∗ ≥ q b ( f ∗ , θ ) ∀ θ . Then using (44), the con ve xity of φ 0 for x ≥ 0 , that f ∗ ≥ q b ( f ∗ , θ ) ∀ θ and Jensen’ s inequality , we get φ 0 ( E f ∗ − q b ( f ∗ , θ )) ≤ E θ φ 0 ( f ∗ − q b ( f ∗ , θ )) = pπ 2 1 − p . It is always possible to choose ∆ such that 0 < ∆ 2 λ < pπ 2 1 − p . For this value of ∆ , φ 0 ∆ ( x ) is alw ays restricted to x > . Since φ 0 ∆ is affine and in vertible, we get φ 0− 1 ∆ pπ 2 1 − p = λ pπ 2 1 − p − ∆ 2 + . Since E ( f ∗ − q b ( f ∗ , θ )) ≥ 0 , the fact that φ 0 is increasing for x ≥ 0 and from the previous equation it follows that f ∗ ≤ E θ q b ( θ ) + φ 0− 1 ∆ p 1 − p π 2 , and substituting the value of E θ q b ( θ ) gi ven by (47), we obtain f ∗ ≤ E θ q a ( θ ) + ( d + λ ) pπ 2 1 − p − ∆ 2 + . Hence, the result for the penalty function with deadband φ defined in (22) is obtained by taking limit when ∆ approaches zero, f ∗ ≤ E θ q a ( θ ) + ( d + λ ) pπ 2 1 − p + . Case f ∗ < E θ q a ( θ ) + : By this case it follows that f ∗ ≤ E θ q a ( θ ) + ( d + λ ) pπ 2 1 − p + . Individual Rationality : For an such that max { q max − E θ q a ( θ ) , E θ q a ( θ ) − q min } ≤ , the report f = E θ q a ( θ ) is individually rational. Thus the optimal baseline report f ∗ should be individually rational. Hence proved. G. Pr oof of Lemma 3 W e start by sho wing that f c > f − . Recall that f − is the av erage of consumption on the days prior to the previous m non-ev ent days. The consumption on these days only appear in the denominator of the CAISO’ s baseline estimate for future DR ev ents. Hence, the incenti ve for the consumer is to reduce the consumption on these days so as to inflate the baseline. On the other hand, f c is the average of the consumption on the previous m non-ev ent days. And the consumption on these days only appear in the numerator of the baseline estimate for any future DR ev ents, through the term f c . Hence, the incentiv e for the consumer is to increase the consumption on these days. Since ev erything else is the same for the day prior to the non-event day and the non-ev ent day except for this incentiv e to reduce and increase, respectively , we conclude that f c > f − . This implies: q −∗ ( θ ) > µ − 1 ( π 0 − π 2 , θ ) . Hence, ¯ f c − q a ( θ ) > µ − 1 ( π 0 − π 2 , θ ) − µ − 1 ( π 0 , θ ) = dπ 2 . T aking expectation with respect to θ we obtain E θ ( ¯ f c − q a ( θ )) > dπ 2 , and this completes the proof.

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment