A Survey of Online Card Payment Fraud Detection using Data Mining-based Methods

💡 Research Summary

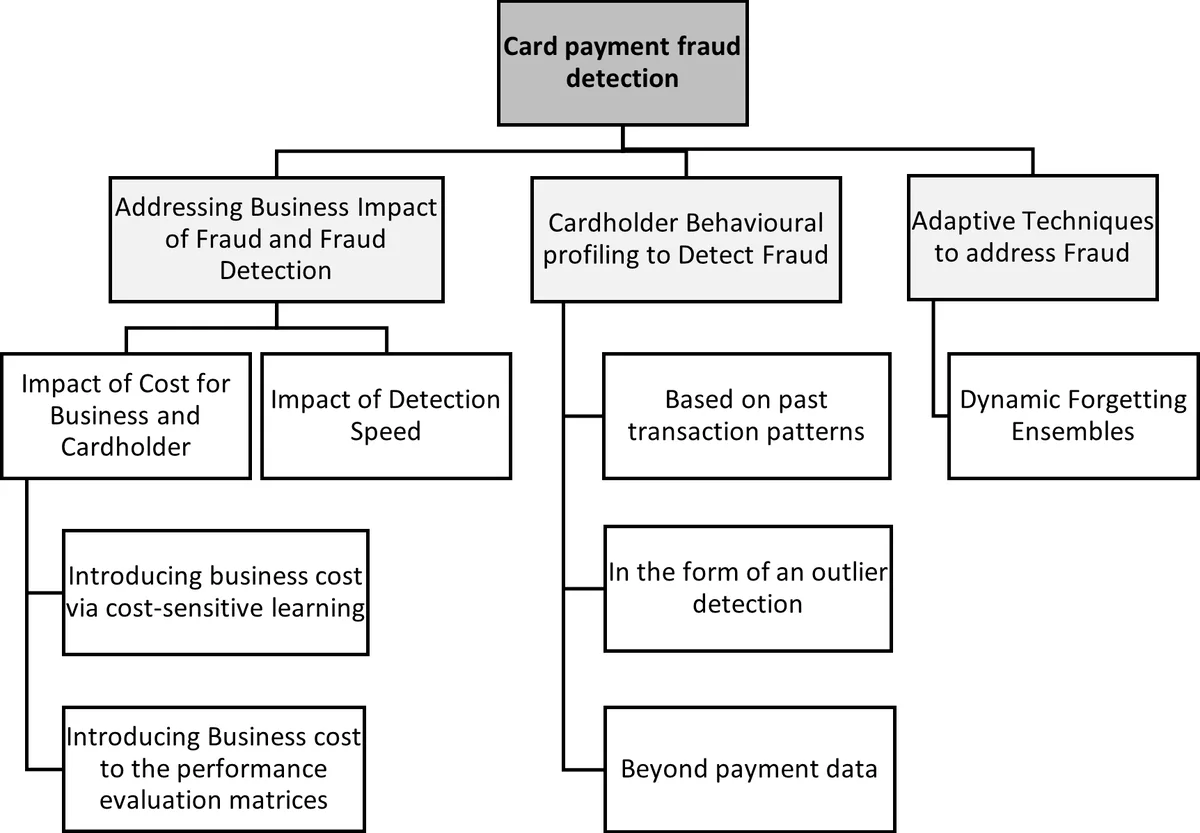

This survey provides a comprehensive review of data‑mining and machine‑learning techniques applied to online card payment fraud detection, covering 45 peer‑reviewed studies published between 2009 and 2020. The authors construct a taxonomy that organizes the literature around three principal challenges: (1) business impact, (2) behavioral profiling for feature engineering, and (3) adaptive methods to cope with the evolving nature of fraud.

In the business‑impact dimension, the survey emphasizes that fraud detection models must be cost‑sensitive rather than merely accuracy‑driven. Several works incorporate transaction‑value‑based cost matrices or instance‑level weighting to penalize false negatives (missed fraud) more heavily than false positives (legitimate transactions flagged as fraud). This approach aligns model training with real‑world financial losses incurred by banks, payment processors, and merchants.

The behavioral‑profiling strand focuses on modeling legitimate cardholder behavior first and then detecting deviations. Researchers extract a rich set of temporal, monetary, and interaction features (e.g., time‑of‑day, purchase amount distribution, cart abandonment patterns) and apply dimensionality‑reduction (PCA, autoencoders) or feature‑importance techniques to select the most discriminative variables. Recent studies adopt recurrent neural networks (LSTM, GRU) to capture sequential dependencies, thereby addressing concept drift—the gradual shift in fraud patterns over time.

Adaptive techniques are discussed extensively. Online learning, incremental model updates, and drift‑detection algorithms such as ADWIN and DDM are employed to keep models current as fraudsters change tactics. Some papers propose ensemble frameworks that combine static and dynamic learners, enabling rapid response to emerging fraud types without retraining the entire system.

Class imbalance, a pervasive issue because fraudulent transactions typically constitute less than 1 % of all records, is tackled through oversampling methods (SMOTE, ADASYN), undersampling, cost‑sensitive learning, and ensemble classifiers (XGBoost, LightGBM). The survey reports that gradient‑boosting models consistently achieve high AUC and recall on highly skewed datasets, especially when paired with appropriate cost functions. Evaluation metrics extend beyond accuracy to include F1‑score, AUC, and latency, reflecting the operational constraints of real‑time payment processing.

The comparative analysis of classifiers covers traditional models (logistic regression, SVM, decision trees) and modern approaches (random forests, gradient boosting, deep neural networks). The authors note that models integrating cost‑sensitivity and imbalance‑handling techniques outperform naïve baselines, and that inference speed is a critical factor for deployment in payment gateways where transaction latency directly impacts user experience.

Finally, the survey identifies gaps in the current literature. No existing work simultaneously satisfies real‑time cost‑sensitivity, adaptive drift handling, and class‑imbalance mitigation within a single unified framework. Moreover, emerging regulatory requirements (GDPR, CCPA) and the demand for explainable AI (XAI) are largely unaddressed. The authors suggest future research directions such as federated learning to preserve data privacy across banks and merchants, incorporation of XAI methods (SHAP, LIME) for transparent decision making, automated feature engineering via AutoML, and multimodal data fusion (transaction logs, behavioral biometrics, device fingerprints). These avenues aim to bridge the gap between academic prototypes and robust, production‑grade fraud detection systems in the rapidly evolving digital economy.

Comments & Academic Discussion

Loading comments...

Leave a Comment