Consensus Algorithms and the Decomposition-Separation Theorem

Convergence properties of time inhomogeneous Markov chain based discrete and continuous time linear consensus algorithms are analyzed. Provided that a so-called infinite jet flow property is satisfied by the underlying chains, necessary conditions fo…

Authors: Sadegh Bolouki, Rol, P. Malhame

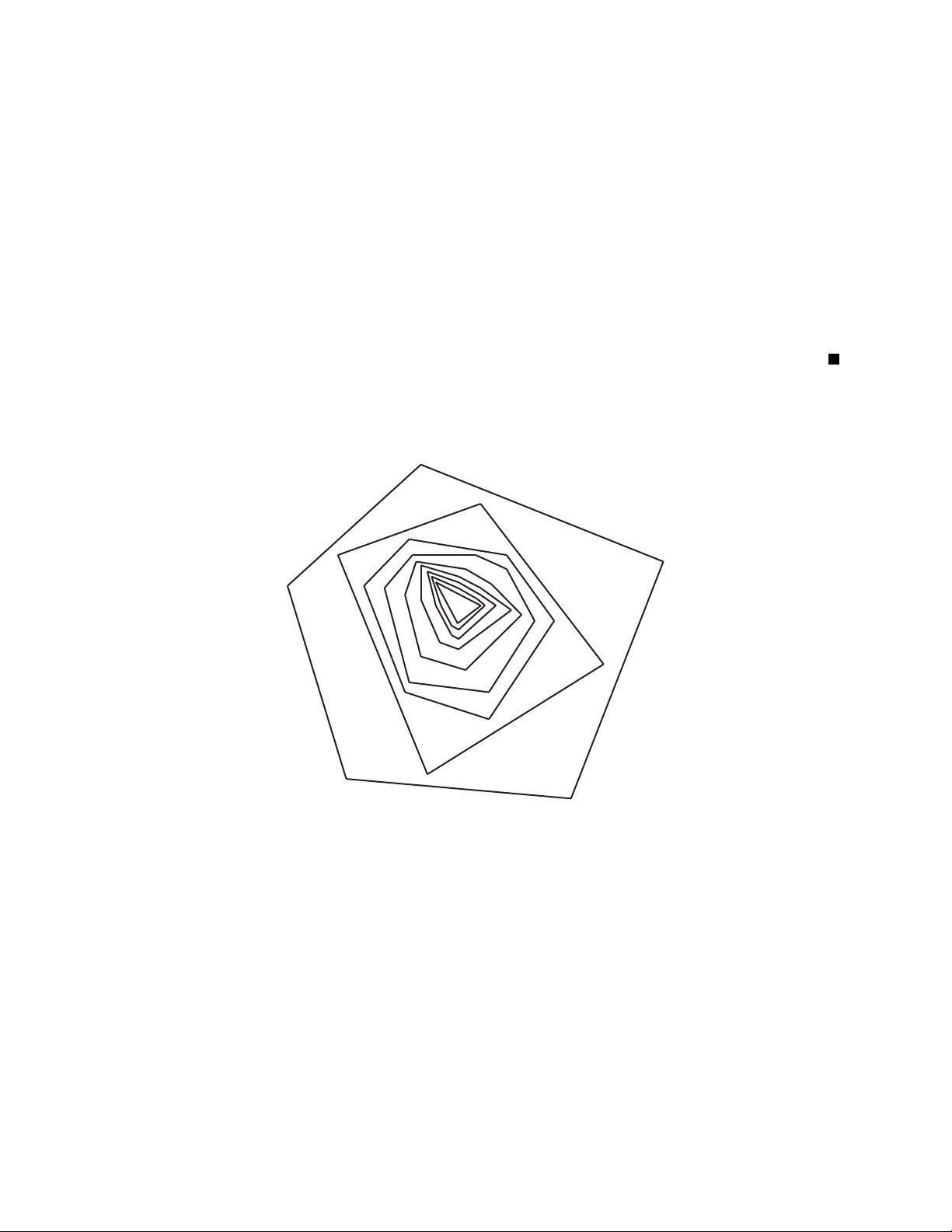

1 Consensus Algorithms and the Decomposition-Separation Theorem Sadegh Bolouki and Roland P . Malham ´ e Abstract Con ver gence properties of time inhomogeneous Markov chain based discrete and continuous time linear consensus algorithms are analyzed. Provided that a so-called infinite jet flo w property is satisfied by the underlying chains, necessary conditions for both consensus and multiple consensus are estab- lished. A recent extension by Sonin of the classical K olmogorov-Doeblin decomposition-separation for homogeneous Marko v chains to the inhomogeneous case is then employed to show that the obtained necessary conditions are also sufficient when the chain is of class P ∗ , as defined by T ouri and Nedi ´ c. It is also shown that Sonin’ s theorem leads to a rediscov ery and generalization of most of the existing related consensus results in the literature. I . I N T RO D U C T I O N Linear consensus algorithms and their con ver gence properties have gained increasing attention in the past decade. They were first introduced in [1], where the author considered the case when the interactions rates between any two agents are time-in v ariant. Later , more general cases were considered in [2]–[11]. The authors aimed at identifying suf ficient conditions for consensus to occur , i.e., for states to asymptotically con ver ge to the same value. Beside consensus, multiple consensus has been the subject of many articles, e.g., [12]–[16]. Multiple consensus refers to the case when each agent state con ver ges, as time grows large, to an individual limit which may or may not be dif ferent from the individual limits of other agent states. Considering the work on linear consensus algorithms, [14]–[16] appear to provide the most general sufficient conditions for the occurrence of consensus or multiple consensus in a multi-agent system with dynamics described by a linear consensus algorithm. S. Bolouki and R.P . Malham ´ e are with the Department of Electrical Engineering, Polytechnique Montr ´ eal, Montreal, QC, H3T 1J4 CA e-mail: (sadegh.bolouki,roland.malhame@polymtl.ca). August 6, 2018 DRAFT 2 In this paper , we deal with the limiting behavior of a general linear consensus algorithm in both discrete and continuous time. Let V = { 1 , . . . , N } be the set of agents. In discrete time, we consider an N -agent system with linear update equation: x ( t + 1) = A ( t ) x ( t ) , ∀ t ≥ 0 . (1) In (1), t indicates the discrete time index, x ( t ) = [ x 1 ( t ) · · · x N ( t )] 0 , t ≥ 0 , is the vector of agent states, where prime ( 0 ) indicates the transposition, A ( t ) , t ≥ 0 , is the matrix of interaction r ates a ij ( t ) , 1 ≤ i, j ≤ N , and { A ( t ) } is the underlying chain or transition chain of the system, which is a chain of ( N × N ) ro w-stochastic matrices, i.e, for e very t ≥ 0 , all elements of A ( t ) are non-negati ve and each row of A ( t ) sums up to 1. Throughout the paper , for simplicity , we refer to a ro w-stochastic matrix as a stochastic matrix. Since A ( t ) is a stochastic matrix for e very t ≥ 0 , sequence { x ( t ) } , by definition, forms a backwar d Markov chain with transition chain { A ( t ) } (notice the ev olution is described by a right hand multiplication by a column vector instead of the usual left hand multiplication by a ro w vector). Although we mainly focus on the discrete time case in this work, we shall extend our results to the continuous time case. If all components of x ( t ) asymptotically con ver ge to the same limit, irrespectiv e of the time index t or the values at which they are initialized, unconditional global consensus , or simply , unconditional consensus , is said to occur . Furthermore, if there e xists a fix ed partition of the N agents such that unconditional consensus occurs for the corresponding sub vectors of x ( t ) , then unconditional multiple consensus is said to occur . The subsets in the partition are then said to form consensus clusters. It is well known that under dynamics (1), unconditional consensus is equi valent to er godicity of chain { A ( t ) } (see [2]), i.e., the property that backward products con verge to matrices with identical ro ws. Furthermore, [16] and [17] establish that a consensus algorithm with update chain { A ( t ) } will induce multiple consensus if { A ( t ) } is so-called class- er godic , i.e., for ev ery t 0 ≥ 0 , the product A ( t ) A ( t − 1) · · · A ( t 0 ) con ver ges, as t → ∞ . For class-ergodic chains, set V can be partitioned into er godic classes , whereby i, j in V belong to the same er godic class if the difference between the i th and j th rows of matrix product A ( t ) A ( t − 1) · · · A ( t 0 ) v anishes, as t → ∞ . Under multiple consensus, the agent indices within the ergodic classes are the same as those within consensus clusters. Sonin, in his so-called Decomposition-Separation (D-S) Theorem [18], suggests an elegant August 6, 2018 DRAFT 3 and illuminating physical interpretation of the dynamics in (1), which we now report for com- pleteness: Start with a forward propagating Markov chain with ( N × N ) transition matrices P ( t ) and associated sequence of probability distrib ution vectors m ( t ) : m 0 ( t + 1) = m 0 ( t ) P ( t ) , ∀ t ≥ 0 . (2) Interpret m i ( t ) , i ∈ V , t ≥ 0 , as the volume of some liquid, say water for example, in a cup i (out of N cups), at time t ≥ 0 , while p ij ( t ) m i ( t ) is the volume of liquid transferred from cup i to cup j at time t ≥ 0 (see Fig. 1). Fig. 1: A physical interpretation of a Markov chain. The volume of liquid in cup i , ∀ i ∈ V , is assumed to be initialized as m i (0) at time zero. No w , let x i ( t ) , i ∈ V , t ≥ 0 , be the concentr ation of a certain substance, such as sugar , alcohol, etc., within the liquid of cup i at time t . W e first assume that the volume of each cup is non-zero at all times in order to make the concentration well-defined. Moreo ver , assume, for e very i ∈ V , that x i ( t ) is initialized as x i (0) at time zero. It is not dif ficult to show that, for e very i ∈ V , and t ≥ 0 : x i ( t + 1) = P j ∈V p j i ( t ) m j ( t ) x j ( t ) m i ( t + 1) . (3) Let: x ( t ) , h x 1 ( t ) · · · x N ( t ) i 0 , (4) and ( N × N ) matrix A ( t ) , with elements a ij ( t ) , i, j ∈ V , be defined by: a ij ( t ) = p j i ( t ) m j ( t ) /m i ( t + 1) , ∀ t ≥ 0 . (5) August 6, 2018 DRAFT 4 From (3), (4), and (5), we conclude that: x ( t + 1) = A ( t ) x ( t ) , ∀ t ≥ 0 . (6) Since A ( t ) is stochastic for ev ery t ≥ 0 (check (5)), { x ( t ) } forms a backward Marko v chain, with transition chain { A ( t ) } , as in (1). Removing the non-zero volume assumption, { A ( t ) } is constructed in such a way that elements of A ( t ) , t ≥ 0 , satisfy: m i ( t + 1) a ij ( t ) = m j ( t ) p j i ( t ) , ∀ i, j ∈ V , ∀ t ≥ 0 . (7) The D-S Theorem, [18], describes the limiting behavior of both m ( t ) and x ( t ) , as t grows large. Ho wev er , to take adv antage of the D-S Theorem in a general consensus algorithm (1), one has to, first, answer the follo wing questions: Starting with a backward propagating Marko v chain generated by { A ( t ) } , is it always possible to find an associated forward propagating Markov chain, with distribution vector { m ( t ) } , generated by a transition chain { P ( t ) } , satisfying an equation of the form (7)? And ho w , if so? As discussed in this paper , due to the existence of a so-called absolute pr obability sequence for { A ( t ) } , as prov ed in fundamental work [19], one could sho w the existence of the desired chains satisfying (7). More specifically , any absolute probability sequence { m ( t ) } admitted by { A ( t ) } , would help construct a forward propagating sequence of transition matrices, via (7). In this paper , it is established that, based on the D-S Theorem, all these previous results can be subsumed. Furthermore, inspired by [17], and recalling the notion of jets in Markov chains from [20], we introduce a property of chains resulting in necessary conditions for the unconditional occurrence of consensus or multiple consensus in (1). W e also establish that, under an additional assumption, that is the chain being in the so-called Class P ∗ [14], these necessary conditions also become sufficient. In addition to the notation defined in the beginning of this section, we adopt the follo wing notation throughout the paper . Letter t stands for either discrete or continuous time indices according to context. Φ( t, τ ) , t, τ ≥ 0 , represents the state transition matrix of the considered system, which can be defined in either the discrete time domain, as in (1), or the continuous time domain, as we will see later on. Moreov er , Φ i ( t, τ ) and Φ i,j ( t, τ ) , 1 ≤ i, j ≤ N , denote the i th column and the ( i, j ) th element (intersection of i th ro w and j th column) of Φ( t, τ ) August 6, 2018 DRAFT 5 respecti vely , while Φ 0 i ( t, τ ) refers to the i th column of Φ 0 ( t, τ ) (the prime acts first), which is also the transpose of the i th row of Φ( t, τ ) . For an arbitrary vector v ∈ R N , and 1 ≤ i ≤ N , v i denotes the i th element of v . The overline ( ¯ ) on a subset indicates complementation of the subset in the uni versal set of interest. The rest of the paper is org anized as follo ws. In Section II, we state necessary conditions for class-ergodicity and er godicity of a chain. The D-S Theorem, and its application in a general linear consensus algorithm, are discussed in Section III. In Section IV, based on the D-S Theorem, we analyze the con vergence properties of chains in Class P ∗ . It is sho wn, in Section V, that this analysis leads to a generalization of most of the existing results in the literature on con ver gence properties of linear consensus algorithms. A geometric approach is introduced in Section VI that applies to both discrete and continuous time consensus protocols. From the geometric frame work built, we extend our analysis to the continuous time case in Section VII. Concluding remarks end the paper in Section VIII. I I . T H E I N FI N I T E J E T - F L O W P R O P E RT Y Inspired by [20], as reported in [18] and [17], in this section, we introduce a property of chains of stochastic matrices, herein called the infinite jet-flow pr operty , leading to necessary conditions for ergodicity and class-ergodicity of the chain. Definition 1: F or a giv en subset V 0 of finite set V = { 1 , . . . , N } , a jet J in V 0 is a sequence { J ( t ) } of subsets of V 0 . A jet J in V 0 is called pr oper if ∅ 6 = J ( t ) ( V 0 , ∀ t ≥ 0 (see Fig. 2). Moreov er , for a jet J , jet-limit J ∗ denotes the limit of the sequence { J ( t ) } , as t gro ws lar ge, if it exists, in the sense that the sequence becomes constant after a finite time. When the elements of the sequence are all identical to a subset S of V , the jet will be referred to as jet S . Definition 2: A tuple of jets ( J 1 , . . . , J c ) is a jet-partition of V , if ( J 1 ( t ) , . . . , J c ( t )) is a partition of V for ev ery t ≥ 0 . Definition 3: Let chain { A ( t ) } of stochastic matrices be gi ven. For any two disjoint jets J s and J k in V , U A ( J s , J k ) , or simply U ( J s , J k ) , when no ambiguity results, denotes the total interactions between the two jets over the infinite time interval, as defined by: U ( J s , J k ) = P ∞ t =0 h P i ∈ J s ( t +1) P j ∈ J k ( t ) a ij ( t ) + P i ∈ J k ( t +1) P j ∈ J s ( t ) a ij ( t ) i . (8) August 6, 2018 DRAFT 6 Fig. 2: Example of a proper jet J in V = { 1 , 2 , 3 , 4 , 5 } : J (0) = { 1 , 2 , 3 , 5 } , J (1) = { 1 , 5 } , J (2) = { 2 } , J (3) = { 2 , 5 } , . . . Moreov er , U A ( t ) ( J s , J k ) , or simply , U t ( J s , J k ) , denotes the interactions between the two jets at time t . More specifically , U t ( J s , J k ) = P i ∈ J s ( t +1) P j ∈ J k ( t ) a ij ( t ) + P i ∈ J k ( t +1) P j ∈ J s ( t ) a ij ( t ) . (9) Definition 4: The complement of jet J in V , denoted by V \ J , or simply , ¯ J , is the jet defined by the set sequence {V \ J ( t ) } . Definition 5: A chain { A ( t ) } of stochastic matrices is said to have the infinite jet-flow pr operty ov er subset V 0 of V if, for e very proper jet J in V 0 , U ( J, V 0 \ J ) is unbounded. If V 0 = V , chain { A ( t ) } is simply said to ha ve the infinite jet-flo w property . Example 1: The following chain { A ( t ) } t ≥ 0 is an e xample of chains with the infinite jet-flow property: A ( t ) = 1 0 0 1 − 1 t +1 0 1 t +1 0 0 1 , if t is ev en , (10) and A ( t ) = 1 0 0 1 t +1 0 1 − 1 t +1 0 0 1 , if t is odd . (11) August 6, 2018 DRAFT 7 It is not easy , at this stage, to show that chain { A ( t ) } defined by (10 – 11) has the infinite jet-flow property . In Lemma 2 stated later in the paper , we suggest a way to check the infinite jet-flow property of a chain that implies the infinite jet-flo w property of { A ( t ) } defined by (10 – 11). Example 2: Chain { A ( t ) } t ≥ 0 defined by: A ( t ) = 1 0 0 1 − 1 ( t +1) 2 0 1 ( t +1) 2 0 0 1 , if t is ev en , (12) and A ( t ) = 1 0 0 1 ( t +1) 2 0 1 − 1 ( t +1) 2 0 0 1 , if t is odd , (13) is an example of chains for which the infinite jet-flo w property is not satisfied. More specifically , if we define jet J by: J ( t ) = { 1 } if t is e ven { 1 , 2 } if t is odd (14) then we have: U ( J, V \ J ) = ∞ X t =0 1 ( t + 1) 2 < ∞ , (15) which shows that the infinite jet-flow property does not hold. In the following proposition, we state a sufficient condition for the infinite jet-flo w property to hold. Definition 6: [14] For a chain { A ( t ) } of stochastic matrices, we define its infinite flow graph , G A ( V , E ) , by an undirected graph of size N , such that: E = { ( i, j ) | i, j ∈ V , i 6 = j , ∞ X t =0 ( a ij ( t ) + a j i ( t )) = ∞} . (16) The set of nodes of each connected component of G A ( V , E ) is called an island of { A ( t ) } . Moreov er , chain { A ( t ) } is said to hav e the infinite flow pr operty if and only if G A ( V , E ) is connected. August 6, 2018 DRAFT 8 The follo wing theorem states a necessary condition for class-ergodicity of chain { A ( t ) } of stochastic matrices. Theor em 1: A chain { A ( t ) } of stochastic matrices is class-ergodic only if the infinite jet-flow property holds over each island of { A ( t ) } . Pr oof: Assume that, on the contrary , { A ( t ) } is class-ergodic, yet some proper jet J , in an island I of { A ( t ) } , is such that U A ( J, I \ J ) is bounded. Recall, from Definition 1, that by a proper jet in I , we mean ∅ 6 = J ( t ) ( I , ∀ t ≥ 0 . Since U A ( J, I \ J ) is bounded and I is an island of { A ( t ) } , we conclude that U A ( J, V \ J ) is bounded as well. Recalling the definition of l 1 -approximation from [13], a chain { B ( t ) } is an l 1 -approximation of chain { A ( t ) } if: ∞ X t =0 k A ( t ) − B ( t ) k < ∞ , (17) where for con venience only , the norm refers to the max norm , i.e., the maximum of the absolute v alues of the matrix elements. W e now form chain { B ( t ) } , an l 1 -approximation of chain { A ( t ) } , by eliminating interactions between J and V \ J at all times. From [13, Lemma 1], it is kno wn that l 1 -approximations do not influence the ergodic classes of a chain. Therefore, { B ( t ) } will remain class-ergodic with the same ergodic classes as { A ( t ) } . Also, the islands of B(t) are the same as those of A(t). On the other hand, U B ( J, V \ J ) = 0 . Gi ven two distinct arbitrary constants, α 1 and α 2 , let states of a multi-agent system, y i ( t ) , i ∈ V , ev olve via dynamics y ( t + 1) = B ( t ) y ( t ) , ∀ t ≥ 0 , and be initialized at: y i (0) = α 1 if i ∈ J (0) , and y i (0) = α 2 otherwise. Since there is no interaction between J and V \ J at any time, we conclude that for e very t ≥ 0 , we have: y i ( t ) = α 1 if i ∈ J ( t ) , and y i ( t ) = α 2 otherwise. Since { B ( t ) } is class-ergodic, lim t →∞ y i ( t ) exists for e very i ∈ V and the consensual agents can be grouped into clusters sharing the same limit and forming an ergodic class. Since the elements in { J ( t ) } are always associated with the same value of y for any t , they will asymptotically belong to a fixed limiting cluster S ∗ , namely agents for which y i ( t ) con verges to α 1 . Since J is a proper jet in I , we hav e: ∅ 6 = S ∗ ( I . Consider , no w , jet S ∗ on island I . S ∗ is essentially the limiting jet J ∗ of J . Since the island structure is common for chains { A ( t ) } and { B ( t ) } , we kno w that U B ( J ∗ , I \ J ∗ ) is unbounded. This is in contradiction with U B ( J, I \ J ) ≤ U B ( J, V \ J ) = 0 , which completes the proof. Later in this paper , we shall establish the suf ficiency of the infinite jet-flo w property in Theorem 1, provided { A ( t ) } is in Class P ∗ , as defined in [14]. W e no w note that the infinite flow property August 6, 2018 DRAFT 9 of { A ( t ) } , which is a necessary condition for ergodicity of { A ( t ) } according to [21], is equi v alent to the e xistence of a single island. Thus, Theorem 1 immediately results in the follo wing corollary which is a necessary condition for ergodicity of chain { A ( t ) } of stochastic matrices. Cor ollary 1: A chain { A ( t ) } of stochastic matrices is er godic only if it has the infinite jet-flo w property . Corollary 1 provides a more restrictiv e necessary condition for ergodicity of a chain than Theorems 1 and 2 of [17]. For instance, from Corollary 1, we conclude that the chain of Example 2 is not er godic since it does not ha ve the infinite jet-flow property . Ho we ver , this cannot be concluded from Theorem 1 and 2 of [17]. On the other hand, we notice that the infinite jet-flo w property is not suf ficient for ergodicity . For instance, one can verify that the chain of Example 1 is not ergodic while the infinite jet-flow property holds. Definition 7: A jet J in V is called an independent jet if the total influence of ¯ J on J is finite ov er the infinite time interval, i.e., ∞ X t =0 X i ∈ J ( t +1) X j ∈ ¯ J ( t ) a ij ( t ) < ∞ . (18) The follo wing theorem, which is a generalization of Corollary 1, states yet another necessary condition for ergodicity of chain { A ( t ) } of stochastic matrices. Theor em 2: A chain { A ( t ) } of stochastic matrices is ergodic only if no two disjoint indepen- dent jets in V exist. Pr oof: Assume that on the contrary , there exist two disjoint independent jets J 1 and J 2 in V . Similar to the proof of Theorem 1, form chain { B ( t ) } , an l 1 -approximation of { A ( t ) } , by eliminating the influence of ¯ J s on J s , s = 1 , 2 , at all times. Recall that { A ( t ) } and { B ( t ) } will share the same ergodicity properties. Let states of a multi-agent system, y i ( t ) , 1 ≤ i ≤ N , e volv e via dynamics y ( t + 1) = B ( t ) y ( t ) , ∀ t ≥ 0 , and be initialized such that for ev ery i ∈ J s (0) ( s = 1 , 2 ), y i (0) = α s , where α 1 6 = α 2 . Then, for e very t ≥ 0 , we have: y i ( t ) = α s , ∀ i ∈ J s ( t ) ( s = 1 , 2 ). Since α 1 6 = α 2 , consensus does not occur . Consequently , chain { B ( t ) } and thus { A ( t ) } could not possibly be ergodic. As an e xample, for chain { A ( t ) } of Example 1, jet { 1 } and jet { 3 } are tw o disjoint independent jets in V = { 1 , 2 , 3 } . Thus, Theorem 2 implies that { A ( t ) } is not ergodic. August 6, 2018 DRAFT 10 Remark 1: The follo wing argument explains why Theorem 2 generalizes Corollary 1. W ithout the infinite jet-flow property , there exists a jet J such that U ( J , V 0 \ J ) is bounded. Thus, both jets J and V \ J are independent jets. On the other hand, jet J and V \ J are disjoint. Thus, infinite jet-flo w is a weaker condition than the non-existence of any two disjoint independent jets. I I I . R E L A T I O N S H I P T O T H E D - S T H E O R E M Consider a multi-agent system with states ev olving according to linear algorithm (1), where { A ( t ) } is a chain of stochastic matrices. Based on the work of K olmogorov in [19], we kno w that for e very chain { A ( t ) } t ≥ 0 , there exists a sequence { π ( t ) } t ≥ 0 of probability distribution v ectors, called absolute pr obability sequence , such that π 0 ( t + 1) A ( t ) = π 0 ( t ) , ∀ t ≥ 0 . (19) The transition chain { P ( t ) } of the forward propagating chain associated with { A ( t ) } and { π ( t ) } as in (7), must be such that: π i ( t ) p ij ( t ) = π j ( t + 1) a j i ( t ) , ∀ i, j ∈ V , ∀ t ≥ 0 . (20) More specifically , if π i ( t ) 6 = 0 , then: p ij ( t ) = π j ( t + 1) a j i ( t ) /π i ( t ) , (21) while if π i ( t ) = 0 , for some i and t ≥ 0 , we choose p ij ( t ) ’ s non-negati ve, arbitrarily such that: N X j =1 p ij ( t ) = 1 . (22) Note that in the former case ( π i ( t ) 6 = 0 ), (22) is automatically satisfied, implying that P ( t ) is a stochastic matrix for e very t ≥ 0 . It is easy to see that: π 0 ( t ) P ( t ) = π 0 ( t + 1) , ∀ t ≥ 0 . (23) Thus, { π ( t ) } forms the probability distribution vector of an inhomogeneous forward propagating Marko v chain. Let V ( J s , J k ) denote the total flow between two arbitrary jets J s and J k in V August 6, 2018 DRAFT 11 ov er the infinite time interval as defined by: V ( J s , J k ) = P ∞ t =0 h P i ∈ J k ( t ) P j ∈ J s ( t +1) r ij ( t ) + P i ∈ J s ( t ) P j ∈ J k ( t +1) r ij ( t ) i , (24) where r ij ( t ) = π i ( t ) p ij ( t ) = π j ( t + 1) a j i ( t ) . (25) V alue r ij ( t ) can be interpreted as the absolute joint probability of being in i at time t and j at time t + 1 . Recalling U from (8), we note that for ev ery J s , J k in V , V ( J s , J k ) ≤ U ( J s , J k ) . Sonin, in his elegant work [18], characterizes the limiting behavior of the tw o sequences { π ( t ) } and { x ( t ) } (ev olving via (1)) in the so-called D-S Theorem as the follo wing. Theor em 3: (Sonin’ s D-S Theor em) There exists an integer c , 1 ≤ c ≤ N , and a decomposition of V into jet-partition ( J 0 , J 1 , . . . , J c ) , J k = { J k ( t ) } , 0 ≤ k ≤ c , such that irrespectiv e of the particular time or state at which x i ’ s are initialized, (i) For ev ery k , 1 ≤ k ≤ c , there exist constants π ∗ k and x ∗ k , such that lim t →∞ X i ∈ J k ( t ) π i ( t ) = π ∗ k , (26) and lim t →∞ x i t ( t ) = x ∗ k , (27) for ev ery sequence { i t } , i t ∈ J k ( t ) . Furthermore, lim t →∞ P i ∈ J 0 ( t ) π i ( t ) = 0 . (ii) For ev ery distinct k , s , 0 ≤ k , s ≤ c : V ( J k , J s ) < ∞ . (iii) This decomposition is unique up to jets { J ( t ) } such that for any { π ( t ) } we hav e: lim t →∞ X i ∈ J ( t ) π i ( t ) = 0 and V ( J, V \ J ) < ∞ . (28) W e shall take adv antage of the Sonin’ s D-S Theorem to characterize the asymptotic behavior of a class of chains of stochastic matrices in the following section. I V . C O N V E R G E N C E I N C L A S S P ∗ In this section, we apply Sonin’ s D-S Theorem to chains in class P ∗ as first defined in [14]. August 6, 2018 DRAFT 12 Definition 8: [14, Definition 3] Chain { A ( t ) } is said to be in class P ∗ if it admits an absolute probability sequence uniformly bounded away from zero, i.e., there exists p ∗ > 0 such that π i ( t ) ≥ p ∗ , ∀ i ∈ V , ∀ t ≥ 0 . (29) For chains in Class P ∗ , it is immediately implied that in the jet decomposition of the D-S Theorem, there is no jet J 0 . Otherwise, lim t →∞ P i ∈ J 0 ( t ) π i ( t ) would be bounded away from zero by at least p ∗ , which is in contradiction with the D-S Theorem. Therefore, there is a jet- partition of V into jets J 1 , . . . , J c , such that for ev ery k = 1 , . . . , c , lim t →∞ x i t ( t ) = x ∗ k , for e very sequence { i t } , where i t ∈ J k ( t ) . Thus, we hav e the following proposition for chains in Class P ∗ . Pr oposition 1: Consider a multi-agent system with dynamics (1), where chain { A ( t ) } is in Class P ∗ . Then, the set of accumulation points of states is finite. Pr oof: Obvious if we note that { x ∗ k | 1 ≤ k ≤ c } form the set of accumulation points of states. Lemma 1: If { A ( t ) } ∈ P ∗ , then for e very two jets J 1 and J 2 in V , V ( J 1 , J 2 ) = ∞ if and only if U ( J 1 , J 2 ) = ∞ . Pr oof: The result is obvious if one notes that p ∗ U ( J 1 , J 2 ) ≤ V ( J 1 , J 2 ) ≤ U ( J 1 , J 2 ) . (30) Theor em 4: A chain { A ( t ) } in Class P ∗ is class-ergodic if and only if the infinite jet-flow property holds over each island of { A ( t ) } . In case of class-ergodicity of { A ( t ) } , islands are the ergodic classes of { A ( t ) } , and constitute the jet limits in the jet decomposition of { A ( t ) } . Moreov er , these limits are attained in finite time. Pr oof: W e first assume that chain { A ( t ) } in P ∗ is class-ergodic. Then, Theorem 1 implies that the infinite jet-flo w property holds o ver each island of the chain. W e no w sho w that if { A ( t ) } ∈ P ∗ is class-er godic, islands are the er godic classes of { A ( t ) } . Let us call an agent i ∈ V , a prime member of jet J k if i ∈ J k ( t ) for infinitely many times. Having defined the prime membership, there exists some Sonin’ s jet-decomposition of { A ( t ) } such that each agent becomes the prime member of a unique jet. T o obtain such a jet-decomposition, start with an arbitrary jet- August 6, 2018 DRAFT 13 decomposition and let any two jets with a common prime member merge. The merging process results in a Sonin’ s jet-decomposition with the desired property . Jets of such decomposition have the property that they become time-in v ariant after a finite time. Thus, the jet-limits exist for each jet and are ergodicity classes of { A ( t ) } . If i and j belong to the same jet-limit, they are in the same island since they are in the same ergodic class of { A ( t ) } ( [13], Lemma 2). Con versely , assume that i and j are neighbors in the infinite flow graph, i.e., P ∞ t =0 ( a ij ( t ) + a j i ( t )) = ∞ . If i and j were to belong to dif ferent jet-limits J s ∗ , J k ∗ , then U ( J s , J k ) would be unbounded. Thus, based on Lemma 1, V ( J s , J k ) would be unbounded as well, which contradicts property (ii) in the D-S theorem. Therefore, ev ery two neighbors in the infinite flow graph belong to the same jet-limit. Consequently , every i and j in the same island must be in the same jet-limit. T o pro ve the suf ficiency , we assume that the infinite jet-flow property holds over each island. Let ( J 1 , . . . , J c ) be a Sonin’ s jet-decomposition, and for ev ery k = 1 , . . . , c , lim t →∞ x i t ( t ) = x ∗ k for every sequence { i t } , where i t ∈ J k ( t ) . Let I be an arbitrary island. W e aim to sho w that, for ev ery i ∈ I , lim t →∞ x i ( t ) exists. T o this aim, k eeping in mind that the aim is achie ved is one of jets J 1 , . . . , J c contains island I after some finite time, we follow three steps. Pick an arbitrary jet J k among J 1 , . . . , J c . Step 1: W e sho w that, infinitely often, we ha ve: I ∩ J k ( t ) = ∅ or I ∩ J k ( t ) = I , where ∅ denotes the empty set. Indeed, assume instead that this behavior occurs only a finite number r of times, denoted t 1 , . . . , t r . W e form a proper jet J in I such that: J ( t ) = I ∩ J k ( t ) , if t 6 = t i , 1 ≤ i ≤ r. (31) Since the infinite jet-flow property holds o ver I , U ( J , I \ J ) is unbounded. On the other hand, except for a finite number of time indices t = t i , 1 ≤ i ≤ r , U t ( J, I \ J ) ≤ U t ( J k , V \ J k ) . This implies that U ( J k , V \ J k ) is unbounded, and, according to Lemma 1, so is V ( J k , V \ J k ) . This is in contradiction with the D-S Theorem. Therefore, I ∩ J k ( t ) = ∅ or I happens infinitely many times. This means that either one or both of the e vents I ∩ J k ( t ) = ∅ and I ∩ J k ( t ) = I occurs infinitely often. Step 2: W e sho w that there are at most a finite number of times such that I ⊆ J k ( t ) and I 6⊆ J k ( t + 1) . Indeed, denote: , 1 3 min {| x ∗ s − x ∗ l | | 1 ≤ s 6 = l ≤ c } , (32) August 6, 2018 DRAFT 14 there exists T ≥ 0 such that: | x i ( t ) − x ∗ l | < , ∀ l = 1 , . . . , c, ∀ i ∈ J l ( t ) , ∀ t ≥ T . (33) For some giv en t ≥ T assume that: I ⊆ J k ( t ) and I 6⊆ J k ( t + 1) . Then, there exists i ∈ I such that i ∈ J k ( t ) \ J k ( t + 1) . In view of (1), (32), and (33), we then hav e: | X j 6∈ J k ( t ) a ij ( t )( x j ( t ) − x i ( t )) | ≥ . (34) On the other hand, | P j 6∈ J k ( t ) a ij ( t )( x j ( t ) − x i ( t )) | ≤ P j 6∈ J k ( t ) a ij ( t ) | x j ( t ) − x i ( t ) | ≤ L P j 6∈ J k ( t ) a ij ( t ) , (35) where L , max { x j (0) − x i (0) , | i, j ∈ V } . (36) Note that L remains an upper bound of | x j ( t ) − x i ( t ) | , ∀ t ≥ 0 , since states are updated via a con vex combination of previous states. Eqs. (34) and (35) imply: X j 6∈ J k ( t ) a ij ( t ) ≥ /L. (37) Therefore, since i ∈ I : X l ∈ I X j 6∈ I a lj ( t ) ≥ X j 6∈ I a ij ( t ) ≥ X j 6∈ J k ( t ) a ij ( t ) ≥ /L. (38) Since U ( I , V \ I ) < ∞ , inequality (38) can only occur for finitely man y times t . This sho ws that if I ⊆ J k ( t ) happens infinite times, then there exists T such that I ⊆ J k ( t ) for e very t ≥ T . Consequently , lim t →∞ x i ( t ) exists, ∀ i ∈ I , and is equal to x ∗ k . Therefore, assume that for a fixed island I , I ⊆ J k ( t ) happens only a finite number of times for ev ery k , 1 ≤ k ≤ c . Thus, from the result of Step 1 , I ∩ J k ( t ) = ∅ must happen infinite times, for ev ery k , 1 ≤ k ≤ c . Step 3: W e show that if I ∩ J k ( t ) = ∅ happens infinite times, for ev ery k , 1 ≤ k ≤ c , then, the following contradiction occurs: F or ev ery k , 1 ≤ k ≤ c , there e xists T k ≥ 0 such that I ∩ J k ( t ) = ∅ , ∀ t ≥ T k . The proof is established by induction on k . With no loss of generality , August 6, 2018 DRAFT 15 assume that x ∗ 1 < · · · < x ∗ k . ( k = 1) : Recalling and T from (32) and (33), assume that for a fixed t ≥ T we hav e I ∩ J 1 ( t ) = ∅ and I ∩ J 1 ( t + 1) 6 = ∅ . Thus, there exists i ∈ I such that i ∈ J 1 ( t + 1) \ J 1 ( t ) . Therefore, X j ∈ J 1 ( t ) | a ij ( t )( x j ( t ) − x i ( t )) | ≥ . (39) Noting that J 1 ( t ) ⊆ V \ I , by repeating steps (34)-(38), we conclude that there are at most finitely many times at which I ∩ J 1 ( t ) = ∅ and I ∩ J 1 ( t + 1) 6 = ∅ . This together with the fact that I ∩ J 1 ( t ) = ∅ happens infinite times, shows that there exists T 1 ≥ 0 such that I ∩ J 1 ( t ) = ∅ , ∀ t ≥ T 1 . k − 1 → k ( 1 < k ≤ c ): Assume that for a fixed t ≥ max { T l | 1 ≤ l < k } , we hav e I ∩ J k ( t ) = ∅ and I ∩ J k ( t + 1) 6 = ∅ . Thus, there exists i ∈ I such that i ∈ J k ( t + 1) \ J k ( t ) . Therefore, X j ∈ S k l =1 J l ( t ) | a ij ( t )( x j ( t ) − x i ( t )) | ≥ . (40) Once again, we note that S k l =1 J l ( t ) ⊆ ¯ I , and repeat steps (34)-(38) to sho w that there exists T k ≥ 0 such that I ∩ J k ( t ) = ∅ , ∀ t ≥ T k . Cor ollary 2: A chain { A ( t ) } ∈ P ∗ is ergodic if and only if it has the infinite jet-flo w property . Since con ver gence of states occurs inside each jet J k , 1 ≤ k ≤ c , for multiple consensus to occur unconditionally (class-ergodicity of { A ( t ) } ), it suffices that for each jet of the D-S Theorem jet decomposition, its jet-limit exists. V . R E L A T I O N S H I P T O P R E V I O U S W O R K A. W eakly Aperiodic Chains in Class P ∗ In this section of the paper , we see how the weak aperiodicity property , as defined in [14], guarantees that the infinite jet-flo w property holds o ver each island. In accordance with [14], weak aperiodicity of a chain is defined as follo ws: Definition 9: A chain { A ( t ) } of stochastic matrices is said to be weakly aperiodic if there exists γ > 0 such that for e very distinct i, j ∈ V and each t ≥ 0 , there exists l ∈ V such that a li ( t ) .a lj ( t ) ≥ γ a ij ( t ) . (41) August 6, 2018 DRAFT 16 Lemma 2: Let { A ( t ) } be a chain of stochastic matrices in Class P ∗ that is weakly aperiodic. Then, the infinite jet-flow property holds over each island of { A ( t ) } . In particular , in presence of a single island, the infinite jet-flow property holds for chain { A ( t ) } . Pr oof: Let { A ( t ) } be weakly aperiodic, I be an arbitrary island of { A ( t ) } , and J be an arbitrary jet in I . If jet-limit J ∗ exists, since I is a connected component of the infinite flo w graph, U ( J ∗ , I \ J ∗ ) is unbounded. Consequently , U ( J, I \ J ) is unbounded and the lemma holds. Thus instead, assume that for jet J , the jet-limit does not exist. Therefore, for infinitely many times t , we must hav e: J ( t + 1) 6⊆ J ( t ) . Let t be fixed and J ( t + 1) 6⊆ J ( t ) . Thus, there exists i ∈ J ( t + 1) \ J ( t ) . From the weak aperiodicity property of { A ( t ) } (see (41)), for ev ery j ∈ J ( t ) , there exists l ∈ V such that: γ a ij ( t ) ≤ a li ( t ) .a lj ( t ) ≤ min { a li ( t ) , a lj ( t ) } ≤ U t ( J, V \ J ) , (42) where U t is defined in (9). The reason for the last inequality is that, whether l ∈ J ( t + 1) or l 6∈ J ( t + 1) , one of a li ( t ) , a lj ( t ) appears in U t ( J, V \ J ) . Hence, X j ∈ J ( t ) γ a ij ( t ) ≤ | J ( t ) | U t ( J, V \ J ) . (43) On the other hand, P j ∈ J ( t ) γ a ij ( t ) = γ P j ∈ J ( t ) a ij ( t ) = γ 1 − P j 6∈ J ( t ) a ij ( t ) ≥ γ (1 − U t ( J, V \ J )) . (44) Relations (43) and (44) imply: U t ( J, V \ J ) ≥ γ / ( γ + | J ( t ) | ) > γ / ( γ + N ) . (45) Since (45) holds for infinitely many times t , U ( J, V \ J ) = P ∞ t =0 U t ( J, V \ J ) is unbounded, and so is U ( J, I \ J ) (since J is a jet in I , and I is an island). Theorem 4 and Lemma 2 immediately imply the follo wing corollary which is the deterministic counterpart of Theorem 4 of [14]. Cor ollary 3: Every weakly aperiodic chain in Class P ∗ is class-ergodic. Note that an equi valent definition of weak periodicity is as follo ws. August 6, 2018 DRAFT 17 Definition 10: A chain { A ( t ) } of stochastic matrices is weakly aperiodic if there exists γ > 0 such that for e very distinct i, j ∈ V and each t ≥ 0 , there exists l ∈ V such that min { a li ( t ) , a lj ( t ) } ≥ γ a ij ( t ) . (46) T o achiev e class-ergodicity under the P ∗ class assumption, the number of times in which an agent moves from a jet to another must be finite. Indeed, let , 1 3 min {| x ∗ s − x ∗ k | | 1 ≤ k 6 = s ≤ c } . (47) Then, there exists T such that for e very t ≥ T , | x i ( t ) − x ∗ k | < , ∀ i ∈ J k ( t ) . (48) If agent i moves from a jet, say J 1 , to another jet, say J 2 , at time t ( i ∈ J 1 ( t ) ∩ J 2 ( t + 1) ), we must hav e: | X j 6∈ J 1 ( t ) a ij ( t )( x j ( t ) − x i ( t )) | ≥ . (49) On the other hand, | P j 6∈ J 1 ( t ) a ij ( t )( x j ( t ) − x i ( t )) | ≤ P j 6∈ J 1 ( t ) a ij ( t ) | x j ( t ) − x i ( t ) | ≤ L P j 6∈ J 1 ( t ) a ij ( t ) , (50) where L is defined in Eq. (36). Eqs. (49) and (112) imply: X j 6∈ J 1 ( t ) a ij ( t ) ≥ /L. (51) Thus, there exists j 6∈ J 1 ( t ) such that a ij ( t ) ≥ L ( N − 1) . (52) No w , from the definition of weak aperiodicity , we kno w that there e xists l ∈ V such that min { a li ( t ) , a lj ( t ) } ≥ γ a ij ( t ) ≥ γ /L ( N − 1) . Note that i and j are in dif ferent jets at time t . Thus, l cannot be in the same jet with both i and j at time t . Therefore, at least one of a li ( t ) , a lj ( t ) August 6, 2018 DRAFT 18 indicates an interaction between a jet and its complement. Since both v alues are bounded below by γ /L ( N − 1) , the sum of interactions between jets J k ’ s and their complements is at least γ /L ( N − 1) at time t . On the other hand, from the D-S Theorem, we now that the total sum of flo ws between jets and their complements is finite ov er the infinite time interv al. Since { A ( t ) } is of Class P ∗ , the total sum of interactions between the jets and their complements must be finite as well. Hence, the number of times that the sum of interactions is at least γ /L ( N − 1) , must be finite. Therefore, there are finite times in which an agent mov es from a jet to another , and the jets become time-in variant after a finite time. It is straightforward to see that the time-in variant jets are connected components of the infinite flow graph. B. Self-Confident and Cut-Balanced Chains Definition 11: [16] A chain { A ( t ) } of stochastic matrices is self-confident with bound δ if a ii ( t ) ≥ δ , ∀ i ∈ V , ∀ t ≥ 0 . Definition 12: [15] A chain { A ( t ) } of stochastic matrices is cut-balanced with bound K if for ev ery V 1 ⊆ V and t ≥ 0 : X i 6∈V 1 X j ∈V 1 a ij ( t ) ≤ K X i ∈V 1 X j 6∈V 1 a ij ( t ) . (53) Pr oposition 2: [14], [16] If chain { A ( t ) } is self-confident and cut-balanced, then it is class- ergodic and the islands form the ergodic classes of { A ( t ) } . Pr oof: Assume that { A ( t ) } has self-confidence and cut-balance properties with bounds δ and K respectiv ely . The chain being self-confident and cut-balanced, it in Class P ∗ (see [14, Theorem 7] where self-confidence is referred to as strong aperiodicity). Thus, from Theorem 4, it is suf ficient to sho w that for an arbitrary island I and an arbitrary proper jet J in I , we have U ( J, I \ J ) = ∞ (that is the infinite jet flow property holds island-wise). Indeed, if jet-limit J ∗ exists, unboundedness of U ( J , I \ J ) is immediately implied from unboundedness of U ( J ∗ , I \ J ∗ ) in view of the definition of islands. Otherwise, there are infinitely many instants t such that J ( t ) 6 = J ( t + 1) . At ev ery such t , there exists i ∈ I such that i ∈ ( J ( t ) \ J ( t + 1)) ∪ ( J ( t + 1) \ J ( t )) . Therefore, recalling (9), U t ( J, I \ J ) ≥ a ii ( t ) ≥ δ . Since there are infinitely many such times, U ( J, I \ J ) is unbounded. August 6, 2018 DRAFT 19 C. Balanced Asymmetric Chains Definition 13: [16] A chain { A ( t ) } of stochastic matrices is said be balanced asymmetric with bound M , if for e very subsets V 1 , V 2 ⊆ V of the same cardinality , and for ev ery t ≥ 0 : X i 6∈V 1 X j ∈V 2 a ij ( t ) ≤ M X i ∈V 1 X j 6∈V 2 a ij ( t ) . (54) Pr oposition 3: Every balanced asymmetric chain is in Class P ∗ . T o prove Proposition 3, we need the following lemma. Lemma 3: Let A be an ( N × N ) balanced asymmetric matrix with bound M . Then, there exists a permutation matrix P N × N such that the product P A is self-confident with bound δ = 4 / ( M N 2 + 4 N − 4) . Pr oof: Form a bipartite-graph H ( V , E ) from A with N nodes in each part. Let V 1 and V 2 , each a copy of V , be sets of nodes of the two parts of H . F or e very i ∈ V 1 and j ∈ V 2 , connect i to j if a ij ≥ δ = 4 / ( M N 2 + 4 N − 4) . W e wish to show that H has a perfect matching. By Hall’ s Marriage Theorem [22, Theorem 5.2], it suf fices to sho w that for e very subset K ⊆ V 1 , we hav e | D ( K ) | ≥ |K| where D ( K ) = { j ∈ V 2 |∃ i ∈ K s.t. ( i, j ) ∈ E } . (55) Indeed, assume that on the contrary , there exists K ⊆ V 1 such that k 0 = | D ( K ) | < |K| = k . Let K = { c 1 , . . . , c k } and D ( K ) = { d 1 , . . . , d k 0 } . Define K 0 ( K by K 0 = { c 1 , . . . , c k 0 } . W e no w hav e: X i ∈K 0 X j 6∈ D ( K ) a ij < k 0 ( N − k 0 ) δ ≤ δ N 2 / 4 . (56) On the other hand, P i 6∈K 0 P j ∈ D ( K ) a ij ≥ P i ∈K\K 0 P j ∈ D ( K ) a ij = ( k − k 0 ) − P i ∈K\K 0 P j 6∈ D ( K ) a ij ≥ ( k − k 0 ) − ( k − k 0 )( N − k 0 ) δ ≥ 1 − ( N − 1) δ. (57) August 6, 2018 DRAFT 20 Since K 0 , D ( K ) ( V are of identical cardinalities, the balanced asymmetry property of A together with (56) and (57) imply that 1 − ( N − 1) δ < δ M N 2 / 4 . (58) Thus, δ > 4 / ( M N 2 + 4 N − 4) , which is a contradiction. Therefore, H has a perfect matching and consequently , there exists a permutation τ such that a τ ( i ) ,i ≥ δ , ∀ i . Thus, the permutation matrix P with e τ ( i ) as its i th row , where e j denotes a ro w vector of length N with 1 in the j th position and 0 in ev ery other position, is such that the product P A is self-confident with δ . Pr oof of Pr oposition 3: Let { A ( t ) } be a balanced asymmetric chain with bound M . Set: δ = 4 / ( M N 2 + 4 N − 4) . W e recursiv ely define sequence { P ( t ) } of permutation matrices as follo ws: From Lemma 3, we kno w that there e xists a permutation matrix P (0) such that the product P (0) A (0) is self-confident with δ . Find permutation matrix P ( t ) , t ≥ 1 , such that the product P ( t ) A ( t ) P 0 ( t − 1) is self-confident with δ . Note that the existence of P ( t ) is implied by Lemma 3, taking into account the fact that the product A ( t ) P 0 ( t − 1) is balanced asymmetric with bound M , since the columns of the product are a permutation of the columns of A ( t ) , itself a balanced asymmetric matrix with bound M . Hence, if we define chain { B ( t ) } by: B ( t ) = P ( t ) A ( t ) P 0 ( t − 1) , (59) then, { B ( t ) } has both the self-confidence and balanced asymmetry properties. Since balanced asymmetry is stronger than cut-balance, chain { B ( t ) } is both self-confidence and cut-balanced. Thus, from [14], we conclude that chain { B ( t ) } belongs to the set P ∗ . Furthermore, it is straightforward to show that if { π ( t ) } is an absolute probability sequence adapted to chain { B ( t ) } , then { π ( t ) P ( t − 1) } , where P ( − 1) = I N × N , is an absolute probability sequence adapted to chain { A ( t ) } . This immediately implies that { A ( t ) } ∈ P ∗ . The class property P ∗ implies that absolute probabilities are uniformly bounded away from zero, and as a result, that there is no J 0 in the jet decomposition of the D-S Theorem. Therefore, we again consider only J 1 , . . . , J c as the jet decomposition. Pr oposition 4: If { A ( t ) } is balanced asymmetric, then the cardinality of each jet in the jet decomposition of the D-S Theorem, becomes time-in v ariant after a finite time. August 6, 2018 DRAFT 21 Pr oof: Let { A ( t ) } be balanced asymmetric with bound M . It suffices to show that there are finite times in which cardinality of a jet, in the jet decomposition of the D-S Theorem, increases by at least 1. In the follo wing, we see what happens when the cardinality of a jet, say J k , increases. Assume that for a fix ed t ≥ 0 , we ha ve | J k ( t + 1) | > | J k ( t ) | . For an arbitrary i ∈ J k ( t + 1) , let T ( J k ( t + 1) be such that i 6∈ T and |T | = | J k ( t ) | . Thus by the balanced asymmetry property , P j ∈ J k ( t ) a ij ( t ) ≤ P l 6∈T P j ∈ J k ( t ) a lj ( t ) ≤ M P l ∈T P j 6∈ J k ( t ) a lj ( t ) ≤ M P l ∈ J k ( t +1) P j 6∈ J k ( t ) a lj ( t ) . (60) Therefore, P i ∈ J k ( t +1) P j ∈ J k ( t ) a ij ( t ) ≤ | J k ( t + 1) | .M P i ∈ J k ( t +1) P j 6∈ J k ( t ) a ij ( t ) . (61) On the other hand, P i ∈ J k ( t +1) P j ∈ J k ( t ) a ij ( t ) = | J k ( t + 1) | − P i ∈ J k ( t +1) P j 6∈ J k ( t ) a ij ( t ) . (62) Eqs. (61) and (62) together imply: X i ∈ J k ( t +1) X j 6∈ J k ( t ) a ij ( t ) ≥ | J k ( t + 1) | 1 + M | J k ( t + 1) | ≥ 1 1 + M . (63) Once again, since the cumulativ e interaction between J k and ¯ J k must be finite over the infinite time interv al because of the D-S Theorem and in view of the class property P ∗ , (63) can occur only for finitely many times t , and this completes the proof. An immediate corollary of Proposition 4 is as follo ws. Cor ollary 4: [16] Consider a multi-agent system with dynamics (1), where { A ( t ) } is balanced asymmetric. Then, z i ( t ) con ver ges for every i ∈ V , as t goes to infinity , where z i ( t ) is the i th least value among x 1 ( t ) , . . . , x N ( t ) . Definition 14: [17] A chain { A ( t ) } of stochastic matrices is said to hav e the absolute infinite flow pr operty , if for e very jet J in V with a time-in variant size, U ( J, V \ J ) is unbounded. Pr oposition 5: [16] If { A ( t ) } is balanced asymmetric, then, { A ( t ) } is class-ergodic if and only if the absolute infinity property holds ov er each island of { A ( t ) } . Furthermore, in case of August 6, 2018 DRAFT 22 class-ergodicity , islands are the ergodic classes of { A ( t ) } . Pr oof: From Proposition 3, we know that { A ( t ) } ∈ P ∗ . Therefore, taking advantage of Theorem 4, it suffices to show that absolute infinite flow and infinite jet-flow properties are equi valent on each island. Obviously , the former is implied by the latter . W e prov e the con verse as follows: Let the absolute infinite flow property hold o ver each island. Assume that I is an arbitrary island of { A ( t ) } and J is an arbitrary jet in I . If the cardinality of jet J becomes time-in variant after a finite time, unboundedness of U ( J, I \ J ) is immediately implied from the absolute infinite flo w property ov er I . Otherwise, the cardinality of J increases infinitely many times by at least 1. In this case, from the proof of Proposition 4 (see (63)), we know that V ( J, V \ J ) is unbounded, and consequently U ( J, V \ J ) is unbounded follo wing Lemma 1. Moreov er , U ( J, V \ J ) + U ( I \ J, V \ I ) = U ( J, I \ J ) + U ( I , V \ I ) , (64) and since U ( I , V \ I ) is bounded because I is an island, unboundedness of U ( J, V \ J ) implies that U ( J, I \ J ) = ∞ . This completes the proof. Cor ollary 5: [16] If chain { A ( t ) } is balanced asymmetric, then it is er godic if and only if it has the absolute infinite flow property . V I . A G E O M E T R I C A P P R O A C H T O W A R D S C O N S E N S U S A L G O R I T H M S In this section, we introduce a geometric framework for a general linear consensus algorithm, that not only interprets the notions of jets and the ocean as explained in the pre vious sections, but serves an alternativ e proof of our results stated in the pre vious sections, and furthermore, as will be shown in the next section, extends them naturally to the continuous time case. Let Φ( t, τ ) , t, τ ≥ 0 , be the state transition matrix of discrete time model (1), i.e., Φ( t, τ ) = A ( t − 1) A ( t − 2) · · · A ( τ ) . (65) Therefore, x ( t ) = Φ( t, τ ) x ( τ ) , ∀ t, τ ≥ 0 . (66) For e very t ≥ τ ≥ 0 , assume that C t,τ is the con ve x hull of the columns of Φ 0 ( t, τ ) . Note that each column of Φ 0 ( t, τ ) is a stochastic vector representing a point in R N , and C t,τ is a polytope in R N if we consider points and segments in R N as polytopes with one and two v ertices respecti vely . August 6, 2018 DRAFT 23 Lemma 4: F or e very t 2 ≥ t 1 ≥ τ , we have: C t 2 ,τ ⊂ C t 1 ,τ , i.e., polytope C t 1 ,τ contains polytope C t 2 ,τ . Pr oof: From (65), we hav e: Φ 0 ( t 2 , τ ) = Φ 0 ( t 1 , τ )Φ 0 ( t 2 , t 1 ) . (67) Since Φ( t 2 , t 1 ) is a stochastic matrix, each column of Φ 0 ( t 2 , τ ) is a con ve x combination of columns of Φ 0 ( t 1 , τ ) . Therefore, ev ery column of Φ 0 ( t 2 , τ ) lies in C t 1 ,τ , and the lemma is prov ed. Lemma 4 sho ws that for a fixed τ ≥ 0 , C t,τ shrinks as t grows. A projection of nested polytopes C t,τ ’ s on a two-dimensional space is sho wn in Fig 3. Fig. 3: An example of nested polygons con verging to a triangle. It is to be noted that when underlying chain { A ( t ) } of dynamics (1) is ergodic, the nested polygons will con ver ge to a point in R N . In general, one concludes that for e very τ ≥ 0 , lim t →∞ C t,τ exists and is also a polytope in R N . Let C τ be the limiting polytope with c τ vertices. It is clear that 1 ≤ c τ ≤ N . One can show that c τ is a non-decreasing function of τ (see [23, Part VIII-B]) and becomes constant after some finite time. W e assume, without loss of generality , that c τ is equal to constant c , ∀ τ ≥ 0 . It is worth mentioning that the choice of letter c here, that also represents the number of jets in the jet decomposition of the Sonin’ s D-S Theorem in August 6, 2018 DRAFT 24 this paper , for the number of vertices of limiting polytope C 0 , is not accidental, as it will be sho wn, in the current section, that the two numbers are equal. Let v 1 , . . . , v c be the c vertices of C 0 . Assume that { 0 t } is a sequence of agents, i.e., 0 t ∈ V for ev ery t ≥ t 0 . Theor em 5: If sequence { 0 t } t ≥ 0 , 0 t ∈ V , ∀ t ≥ 0 , is such that the distance between Φ 0 0 t ( t, 0) and set { v 1 , . . . , v c } does not con ver ge to zero as t grows large, then: inf { π 0 t ( t ) | t ≥ 0 } = 0 . (68) Pr oof: W e kno w that vector v i , 1 ≤ i ≤ c , lies outside of the con ve x hull of vectors v j ’ s, j 6 = i . Let w i be the nearest point to v i , on the con vex hull of v j ’ s, j 6 = i . For a small 0 > 0 , draw a hyperplane, distant 0 from v i , crossing segment v i w i and orthogonal to it. Let u ( t ) , Φ 0 0 t ( t, 0) . For a sufficiently small 0 , there e xists a subsequence of { u ( t ) } such that v i and the elements of the subsequence lie on opposite sides of the hyperplane for ev ery i , 1 ≤ i ≤ c . Otherwise, the distance between { u ( t ) } and set { v 1 , . . . , v c } would con ver ge to zero. Define: 0 1 , min {| v i − w i | | 1 ≤ i ≤ c } , (69) and: , min { 0 , 0 1 / 4 } , (70) and for an arbitrary constant δ , 0 < δ < 1 , let: 1 , δ / (2 N ) (71) W e summarize the rest of the proof, since it is v ery similar to the proof of [23, Lemma 7], from (25) to (35). W e know that for a sufficiently large time T ≥ 0 , if t ≥ T , e very vector in C t, 0 lies within an 1 -distance of C 0 . For e very i , 1 ≤ i ≤ c , draw a hyperplane l i , parallel to the hyperplane drawn pre viously , distant from v i , crossing segment v i w i . Draw also a hyperplane m i , parallel to l i , on the other side of v i , distant 1 from v i (see Fig. 4). Define for ev ery i , 1 ≤ i ≤ c : S i = { j ∈ V | Φ 0 j ( T , 0) lies in strip margined by l i , m i } . (72) August 6, 2018 DRAFT 25 Fig. 4: Planes l i and m i are orthogonal to segment v i w i . One can show that, S i ’ s, 1 ≤ i ≤ c , are disjoint non-empty sets. Define also: S 0 = V \ c [ j =1 S j . (73) As mentioned above, there exists a subsequence of { u ( t ) } such that v i and the elements of the subsequence lie on the opposite sides of l i (note that ≤ 0 ) for ev ery i = 1 , . . . , c . W ithout loss of generality , assume that { u ( T ) } belongs to that subsequence (otherwise, choose T 1 > T such that u ( T 1 ) belongs to that subsequence, and replace T by T 1 in the argument). Hence, S 0 6 = ∅ , and S i ’ s partition agent set V . Similar to the proof of [23, Lemma 7], we have the follo wing inequality (equiv alence of inequality (35) in [23]): X j 6∈ S i ( u i ) j ≤ 2 δ / (2 N + 1) < δ / N . (74) Consequently , X j ∈ S 0 ( u i ) j ≤ X j 6∈ S i ( u i ) j < δ / N . (75) August 6, 2018 DRAFT 26 Thus, for ev ery i ∈ V and j ∈ S 0 : inf { Φ i,j ( t, T ) | t ≥ T } < δ / N . (76) Consequently , inf { X i ∈V ,j ∈ S 0 Φ i,j ( t, T ) | t ≥ T } < N δ / N = δ. (77) Since we have: π j ( T ) = π ( t )Φ j ( t, T ) = X i ∈V π i ( t )Φ i,j ( t, T ) ≤ X i ∈V Φ i,j ( t, T ) , (78) from (77) we conclude that: π j ( T ) < δ, ∀ j ∈ S 0 . (79) W e recall that S 0 includes one of the elements of sequence { 0 t } , i.e., 0 T . Hence, π 0 T ( T ) < δ . Recall also that δ was chosen arbitrarily . By letting δ go to zero, we conclude that inf { π 0 t ( t ) | t ≥ 0 } = 0 , and the theorem is prov ed. Remark 2: W e explain, in the following, that there is a one-to-one correspondence between the vertices of limiting polytope C 0 and jets J 1 , . . . , J c of the Sonin’ s jet decomposition. Recall, from Section III, that ho w we employed the absolute probability sequence of chain { A ( t ) } to construct a forw ard propagating Markov chain from the giv en backward one. Now , let J k be an arbitrary jet among J 1 , . . . , J c . Let, also, { k t } be a sequence inside jet J k , i.e., k t ∈ J k ( t ) , ∀ t ≥ 0 . Since, due to the D-S Theorem, lim t →∞ x k t ( t ) exists irrespectiv e of what x (0) is, lim t →∞ Φ 0 k t ( t, 0) exists as well, and is irrespective of how the sequence is chosen. W e aim to sho w that lim t →∞ Φ 0 k t ( t, 0) is one of v 1 , . . . , v c . Since the volume of J k ( t ) con ver ges to a non-zero constant, as t → ∞ , one can form a sequence { k t } inside jet J k , i.e., k t ∈ J k ( t ) , ∀ t ≥ 0 , such that: lim inf { π k t ( t ) | t ≥ 0 } > 0 . (80) One way to form such a sequence is to pick, at each time instant, the cup in J k that has the maximum volume. From Theorem 5 and inequality (80), we conclude that the distance between Φ 0 k t ( t, 0) and set { v 1 , . . . , v c } , the vertices of limiting polytope C 0 , must vanish as t gro ws large. Thus, lim t →∞ Φ 0 k t ( t, 0) is belongs to set { v 1 , . . . , v c } . August 6, 2018 DRAFT 27 It is also clear that if sequences { s t } and { k t } are in two disjoint jets J s and J k respecti vely , lim t →∞ Φ 0 s t ( t, 0) and lim t →∞ Φ 0 k t ( t, 0) cannot con ver ge to the same vertex of C 0 , since otherwise, merging the two jets would violate the uniqueness of the Sonin’ s jet decomposition. V I I . C O N S E N S U S I N T H E C O N T I N U O U S T I M E C A S E One may define a general linear consensus algorithm in continuous time as follows: ˙ x = A ( t ) x ( t ) , t ≥ 0 , (81) where x ( t ) is the v ector of opinions at each time instant t ≥ 0 and { A ( t ) } is the underlying chain of the system. It is assumed that each matrix of underlying chain A ( t ) has zero row sum and non-negati ve off-diagonal elements and each element a ij ( t ) of A ( t ) is a measurable function. These constraints on the underlying chain suggest a view of A(t) as the e volution of the intensity matrix of a time inhomogeneous Markov chain. W e shall use in this section, a continuous time version of the geometric framework dev eloped in Section VI, in con ver gence analysis of agents in a network with continuous time dynamics (81), particularly when underlying chain { A ( t ) } is in a continuous time version of Class P ∗ . Let Φ( t, τ ) , t, τ ≥ 0 , represent the state transition matrix of system associated with (81), i.e., x ( t ) = Φ( t, τ ) x ( τ ) , ∀ t ≥ τ ≥ 0 . (82) Note that similar to the discrete time case, Φ( t, τ ) is a stochastic matrix for ev ery t ≥ τ ≥ 0 . More specifically , Φ i,j ( t, τ ) can be considered as transition probability of a backward propagating inhomogeneous Markov chain. In particular , for e very t 2 ≥ t 1 ≥ τ ≥ 0 , we have: Φ i,j ( t 2 , τ ) = X k Φ i,k ( t 2 , t 1 )Φ k,j ( t 1 , τ ) , (83) with the conditions: Φ i,j ( t, τ ) ≥ 0 , (84) X j Φ i,j ( t, τ ) = 1 , (85) Φ i,j ( t, t ) = δ ij , (86) August 6, 2018 DRAFT 28 where δ ij is the Kronecker symbol. Underlying chain { A ( t ) } is said to be ergodic if for ev ery τ ≥ 0 , Φ( t, τ ) con verges to a matrix with equal rows as t → ∞ . Similar to the discrete time case, er godicity of { A ( t ) } is equiv alent to the occurrence of unconditional consensus in (81). Moreov er , { A ( t ) } is class-ergodic if for e very τ ≥ 0 , lim t →∞ Φ( t, τ ) exists, b ut with possibly distinct ro ws. Chain { A ( t ) } is class-er godic if and only if multiple consensus occurs in (81) unconditionally . Recall that the associated state transition matrix associated with (81) can be e xpressed via the Peano-Baker series (see [24, Section 1.3]): Φ( t, τ ) = I N × N + R t τ A ( σ 1 ) dσ 1 + R t τ A ( σ 1 ) R σ 1 τ A ( σ 2 ) dσ 2 dσ 1 + R t τ A ( σ 1 ) R σ 1 τ A ( σ 2 ) R σ 2 τ A ( σ 3 ) dσ 3 dσ 2 dσ 1 + · · · , (87) where I N × N denotes the N × N identity matrix. Remember that state transition matrix Φ( t, τ ) is in vertible for ev ery t ≥ τ ≥ 0 . Furthermore, once again, based on [19], we kno w that for ev ery state transition matrix Φ( t, τ ) , t, τ ≥ 0 , there exists an absolute probability sequence { π ( t ) } , t ≥ 0 , such that: π ( τ ) = π ( t )Φ( t, τ ) , ∀ t, τ ≥ 0 . (88) Having recalled the state transition matrix and the absolute probability sequence for the con- tinuous time model (81), we can no w carry out a continuous time v ersion of the geometric frame work dev eloped in Section VI. Once again, for ev ery t ≥ τ ≥ 0 , assume that C t,τ is the conv ex hull of columns of Φ 0 ( t, τ ) , or equi valently transposed ro ws of Φ( t, τ ) . Remember that each column of Φ 0 ( t, τ ) is a stochastic vector as in the discrete time case. Now , note that Lemma 4 holds for the continuous time as well, since its proof remains v alid assuming that the time indices refer to continuous time. Therefore, we again assume that limiting polytopes C τ ’ s, τ ≥ 0 , exist. Let c τ be the number of vertices of C τ . W e sho w in the following that, c τ , τ ≥ 0 , is constant (unlike the discrete time case in which c τ was monotonic increasing with respect to τ ). Assume that τ 2 ≥ τ 1 ≥ 0 are two arbitrary time instants. W e wish to show that c τ 1 = c τ 2 . August 6, 2018 DRAFT 29 Define linear operator φ τ 2 ,τ 1 : R N → R N by: φ τ 2 ,τ 1 ( v ) , Φ 0 ( τ 2 , τ 1 ) v , ∀ v ∈ R N . (89) Note now that from properties of state transition matrices, for t ≥ τ 2 ≥ τ 1 ≥ 0 , we have: Φ 0 ( t, τ 1 ) = Φ 0 ( τ 2 , τ 1 )Φ 0 ( t, τ 2 ) . (90) Therefore, in vie w of (90) by taking t to infinity , the vertices of C τ 2 are uniquely mapped to vectors in R N which because of the linearity of map (89), will play the role of vertices for the generation of con ve x hull C τ 1 . Also, it is not dif ficult to sho w that the images of v ertices of C τ 2 must remain vertices of C τ 1 , for if one of the images of a vertex of C τ 2 , say v , turned out to be a conv ex combination of other v ertices of C τ 1 , this would also be true for the in verse images of these vertices (also vertices of C τ 2 due to in vertibility of matrix Φ 0 ( τ 2 , τ 1 ) ), and v would then fail to be a vertex of C τ 2 . In conclusion, C τ 1 and C τ 2 will have the same number of vertices, and (89) constitutes a one to one map between corresponding pairs of vertices. One may now use the same ar gument to e xtend Theorem 5 to the continuous time case while t 0 , the initial time in Theorem 5, can be chosen arbitrarily here (recall that for Theorem 5 to be true, C t 0 must hav e had the maximum number of vertices among all C τ ’ s, and since c τ is constant for τ ≥ 0 in the continuous time case, t 0 can be chosen arbitrarily). W e no w aim to take adv antage of Theorem 5 to address the limiting behavior of system (81) when underlying chain { A ( t ) } is in Class P ∗ . Lemma 5: F or ev ery j ∈ V , π j ( τ ) ≤ inf ( X i ∈V Φ i,j ( t, τ ) | t ≥ τ ) . (91) Pr oof: Obvious, since for ev ery t ≥ τ : π j ( τ ) = π ( t )Φ j ( t, τ ) = X i ∈V π i ( t )Φ i,j ( t, τ ) ≤ X i ∈V Φ i,j ( t, τ ) . (92) Adopting the same definition of Class P ∗ as in the discrete time case (see Section IV), we state the following lemma. August 6, 2018 DRAFT 30 Lemma 6: A state transition matrix Φ( t, τ ) , t, τ ≥ 0 , associated with (81), is in Class P ∗ if and only if for ev ery j ∈ V : inf ( X i ∈V Φ i,j ( t, τ ) | t ≥ τ ) > 0 . (93) Pr oof: The only if part is an immediate result of Lemma 5, and the if part is a result of the way the existence of the absolute probability sequence can be obtained in [19] by al ways choosing to initialize agent probabilities on finite intervals with a uniform distribution. Let the infinite flo w graph of a continuous time chain { A ( t ) } is defined according to Definition 6 by replacing summation with inte gral. The follo wing theorem describes the con vergence properties of system (81) when the underlying chain is in Class P ∗ . Theor em 6: If state transition matrix Φ( t, τ ) , t, τ ≥ 0 , is in Class P ∗ , then multiple consensus occurs unconditionally in system (81). Moreov er , the number of consensus clusters is equal to the number of the components of the infinite flo w graph of the transition chain. In particular, consensus occurs unconditionally if and only if the infinite flow property holds. The follo wing theorem clarifies that Theorem 6 generalizes continuous time consensus results of [15]. Theor em 7: If transition chain { A ( t ) } in (81) is cut-balanced, then state transition matrix Φ( t, τ ) , t ≥ τ ≥ 0 , is in Class P ∗ . Pr oof: Let { A ( t ) } be cut-balanced with bound K . Assume that Φ( t, τ ) , t ≥ τ ≥ 0 , is the state transition matrix associated with (81). In vie w of Lemma 6, our aim is to sho w that: 1 / N e 0 Φ A ( t, τ ) ≥ p ∗ e 0 , for some p ∗ > 0 , where e 0 = h 1 · · · 1 i , and the inequality is to be understood element-wise. Assume that α = sup {− a ii ( t 0 ) | i ∈ V , τ ≤ t 0 ≤ t } . Let chain B be such that B ( t 0 ) = A ( t 0 ) + 2 α I , ∀ τ ≤ t 0 ≤ t , where I is the identity matrix. It is easy to verify that: Φ B ( t, τ ) = e 2 α ( t − τ ) Φ A ( t, τ ) . (94) Moreov er , by construction, on-diagonal elements of B ( t 0 ) , τ ≤ t 0 ≤ t , are greater than or equal to α . Note that B ( t 0 ) ( τ ≤ t 0 ≤ t ) is not a stochastic matrix; instead each of its rows sums up to 2 α . W e calculate in the following, 1 / N e 0 Φ B ( t, τ ) . Therefore, from the Peano-Baker series (87), August 6, 2018 DRAFT 31 the expression: 1 N e 0 Z t τ B ( σ 1 ) Z σ 1 τ B ( σ 2 ) · · · Z σ k − 1 τ B ( σ k ) dσ k · · · dσ 1 (95) is of interest. Expression (95) is equal to: (2 α ) k N e 0 Z t τ B ( σ 1 ) 2 α Z σ 1 τ B ( σ 2 ) 2 α · · · Z σ k − 1 τ B ( σ k ) 2 α dσ k · · · dσ 1 , (96) which is also equal to: (2 α ) k Z t τ Z σ 1 τ Z σ k − 1 τ 1 N e 0 B ( σ 1 ) 2 α B ( σ 2 ) 2 α · · · B ( σ k ) 2 α dσ k · · · dσ 1 . (97) Note that B ( t 0 ) / 2 α is a sequence of transition matrices which generates a Marko v chain which is both cut-balanced and self-confident, and hence in Class P ∗ ( [14, Theorem 7]). As a result, there exists a positiv e p ∗ such that: 1 N e 0 B ( σ 1 ) 2 α · B ( σ 2 ) 2 α · · · · · B ( σ k ) 2 α ≥ p ∗ e 0 . (98) Inequality (98) implies that expression (97), and consequently expression (95), is greater than or equal to (2 α ) k p ∗ ( t − τ ) k /k ! . No w , if we write 1 / N e 0 Φ B ( t, τ ) as sum of expressions like (95), we hav e: 1 / N e 0 Φ B ( t, τ ) ≥ ∞ X k =0 (2 α ) k p ∗ ( t − τ ) k k ! = p ∗ e 2 α ( t − τ ) . (99) Thus, 1 / N e 0 Φ A ( t, τ ) ≥ p ∗ e 2 α ( t − τ ) .e − 2 α ( t − τ ) = p ∗ , (100) and from Lemma 6 the theorem is proved. V I I I . C O N C L U S I O N W e considered a general linear distributed av eraging algorithm in both discrete time and continuous time. Follo wing [17], and recalling the notion of jets from [20], we introduced a property of chains of stochastic matrices, more precisely , the infinite jet-flo w property in the discrete time case. The latter property is sho wn to be a strong necessary condition for ergodicity of the chain. Moreover , for the chain to be class-ergodic, the infinite jet-flow property must hold ov er each connected component of the infinite flow graph, as defined in [14]. August 6, 2018 DRAFT 32 W e then illustrated the close relationship between Sonin’ s D-S Theorem and con ver gence properties of linear consensus algorithms. By emplo ying the D-S Theorem, we showed in the discrete time case that the necessary conditions found earlier are also suf ficient in case the chain is in Class P ∗ [14]. W e argued that the obtained equiv alent conditions for ergodicity and class-ergodicity of chains in Class P ∗ can subsume the pre vious related results in the literature, [14]–[16] in particular . A geometric approach w as then introduced to interpret the jets in the D-S Theorem. The approach turned out to be a powerful method to rediscov er our aforementioned results, and also to extend them to the continuous time case. In future work, we shall attempt an extension of our results to the case when the number of agents increases to infinity , although the D-S Theorem holds only if N is finite. R E F E R E N C E S [1] M. H. DeGroot, “Reaching a consensus, ” Journal of the American Statistical Association , vol. 69, no. 345, pp. 118–121, 1974. [2] S. Chatterjee and E. Seneta, “T owards consensus: some con vergence theorems on repeated a veraging, ” J ournal of Applied Pr obability , pp. 89–97, 1977. [3] J. N. Tsitsiklis, D. P . Bertsekas, M. Athans et al. , “Distributed asynchronous deterministic and stochastic gradient optimization algorithms, ” IEEE transactions on automatic contr ol , vol. 31, no. 9, pp. 803–812, 1986. [4] J. N. Tsitsiklis, “Problems in decentralized decision making and computation. ” DTIC Document, T ech. Rep., 1984. [5] D. P . Bertsekas and J. N. Tsitsiklis, P arallel and distributed computation: numerical methods . Prentice-Hall, Inc., 1989. [6] A. Jadbabaie, J. Lin, and A. S. Morse, “Coordination of groups of mobile autonomous agents using nearest neighbor rules, ” IEEE T ransactions on Automatic Contr ol , vol. 48, no. 6, pp. 988–1001, 2003. [7] V . Blondel, J. Hendrickx, A. Olshevsky , and J. Tsitsiklis, “Con vergence in multiagent coordination, consensus, and flocking, ” in Proceedings of 44th IEEE Confer ence on Decision and Contr ol and European Contr ol Conference (CDC-ECC 2005) , 2005, pp. 2996–3000. [8] L. Moreau, “Stability of multiagent systems with time-dependent communication links, ” IEEE T ransactions on A utomatic Contr ol , vol. 50, no. 2, pp. 169–182, 2005. [9] J. M. Hendrickx and V . Blondel, “Con ver gence of different linear and nonlinear vicsek models, ” in Pr oceedings of 17th International Symposium on Mathematical Theory of Networks and Systems (MTNS2006) , 2006, pp. 1229–1240. [10] J. M. Hendrickx, “Graphs and networks for the analysis of autonomous agent systems, ” Ph.D. dissertation, Ecole Polytechnique, 2008. [11] S. Li, H. W ang, and M. W ang, “Multi-agent coordination using nearest neighbor rules: a revisit to vicsek model, ” arXiv pr eprint cs/0407021 , 2004. [12] J. Lorenz, “ A stabilization theorem for dynamics of continuous opinions, ” Physica A: Statistical Mechanics and its Applications , vol. 355, no. 1, pp. 217–223, 2005. August 6, 2018 DRAFT 33 [13] B. T ouri and A. Nedi ´ c, “On approximations and ergodicity classes in random chains, ” IEEE T ransactions on Automatic Contr ol , vol. 57, no. 11, pp. 2718–2730, 2012. [14] ——, “Product of random stochastic matrices, ” IEEE T ransactions on Automatic Control , vol. 59, no. 2, pp. 437–448, 2014. [15] J. M. Hendrickx and J. N. Tsitsiklis, “Con vergence of type-symmetric and cut-balanced consensus seeking systems, ” IEEE T ransactions on Automatic Contr ol , vol. 58, no. 1, pp. 214–218, 2013. [16] S. Bolouki and R. P . Malham ´ e, “Ergodicity and class-ergodicity of balanced asymmetric stochastic chains, ” GERAD T echnical Report G-2012-93 , 2012. [17] B. T ouri and A. Nedi ´ c, “On backward product of stochastic matrices, ” Automatica , vol. 48, no. 8, pp. 1477–1488, 2012. [18] I. M. Sonin et al. , “The decomposition-separation theorem for finite nonhomogeneous markov chains and related problems, ” in Markov Pr ocesses and Related T opics: A F estschrift for Thomas G. Kurtz . Institute of Mathematical Statistics, 2008, pp. 1–15. [19] A. K olmogoroff, “Zur theorie der markoffschen ketten, ” Mathematische Annalen , vol. 112, no. 1, pp. 155–160, 1936. [20] D. Blackwell, “Finite non-homogeneous chains, ” Annals of Mathematics , pp. 594–599, 1945. [21] B. T ouri and A. Nedi ´ c, “On ergodicity , infinite flow , and consensus in random models, ” IEEE T ransactions on Automatic Contr ol , vol. 56, no. 7, pp. 1593–1605, 2011. [22] J. A. Bondy and U. S. R. Murty , Graph theory with applications . Macmillan London, 1976, vol. 6. [23] S. Bolouki, R. P . Malham ´ e, M. Siami, and N. Motee, “ ´ eminence grise coalition: on the shaping of public opinion, ” arXiv pr eprint , 2014. [24] R. W . Brockett, Finite dimensional linear systems . New Y ork Wile y , 1970. August 6, 2018 DRAFT

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment