Limits of Risk Predictability in a Cascading Alternating Renewal Process Model

Most risk analysis models systematically underestimate the probability and impact of catastrophic events (e.g., economic crises, natural disasters, and terrorism) by not taking into account interconnectivity and interdependence of risks. To address this weakness, we propose the Cascading Alternating Renewal Process (CARP) to forecast interconnected global risks. However, assessments of the model’s prediction precision are limited by lack of sufficient ground truth data. Here, we establish prediction precision as a function of input data size by using alternative long ground truth data generated by simulations of the CARP model with known parameters. We illustrate the approach on a model of fires in artificial cities assembled from basic city blocks with diverse housing. The results confirm that parameter recovery variance exhibits power law decay as a function of the length of available ground truth data. Using CARP, we also demonstrate estimation using a disparate dataset that also has dependencies: real-world prediction precision for the global risk model based on the World Economic Forum Global Risk Report. We conclude that the CARP model is an efficient method for predicting catastrophic cascading events with potential applications to emerging local and global interconnected risks.

💡 Research Summary

The paper addresses a critical shortcoming of most quantitative risk‑analysis frameworks: the systematic underestimation of low‑probability, high‑impact events because they ignore the interdependence and connectivity among risks. To overcome this, the authors introduce the Cascading Alternating Renewal Process (CARP), a stochastic network model that extends the classic Alternating Renewal Process (ARP) by allowing multiple states, Poisson‑driven transitions, and weighted edges that encode how the activation of one risk influences others. Four hidden parameters govern the dynamics: an internal ignition rate (α), an external ignition rate (β), and two recovery rates (γ, δ). Parameter inference is performed via Maximum Likelihood Estimation (MLE).

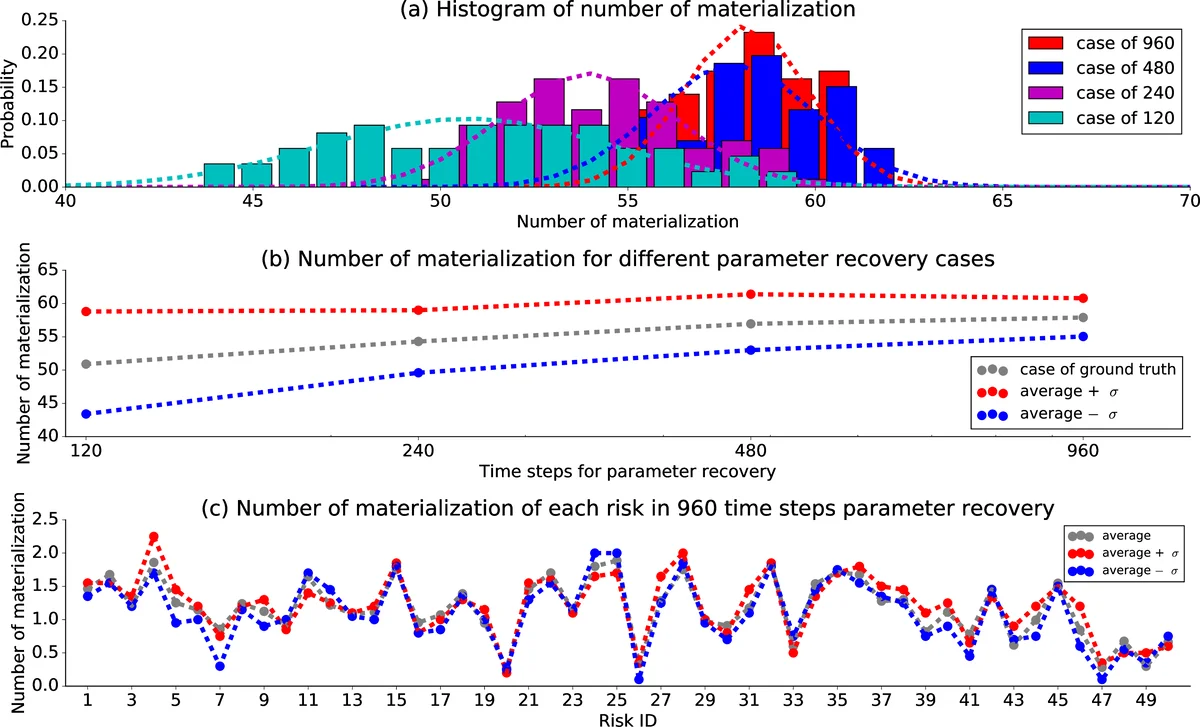

The study proceeds in two complementary parts. First, a synthetic “city‑fire” environment is built from modular blocks containing large, medium, and small houses. The houses differ in fire‑propagation probability and recovery speed, which translates into distinct node degrees in the underlying graph. By varying the number of blocks, the authors generate cities of arbitrary size. They then run stochastic simulations for seven training‑data lengths (100 to 6 400 time steps), each repeated 50 times with different random seeds, thereby creating 350 independent ground‑truth datasets with known parameter values.

For each dataset, MLE recovers α, β, γ, and δ. The authors evaluate recovery quality using relative error and its variance. The key empirical findings are:

- The mean relative error decays toward zero as the amount of historical data grows, confirming the consistency of MLE.

- The variance of the relative error follows a power‑law decay with an exponent close to –0.5, exactly as predicted by asymptotic theory for maximum‑likelihood estimators. In log‑log plots the slope is approximately –0.5 for all four parameters.

- α and β exhibit larger errors than γ and δ because they jointly determine the initiation of fires; errors in one can be partially compensated by opposite errors in the other, leading to a characteristic trade‑off.

- Standard deviations of the relative errors also shrink according to the same power‑law, reinforcing the robustness of the estimator.

The second part applies the same methodology to a real‑world dataset: the Global Risk Network compiled in the World Economic Forum’s Global Risk Report. Using the observed activation histories of global risks, the authors estimate the CARP parameters and find that the error‑decay patterns observed in the synthetic experiments persist, despite the single‑realization nature of the empirical data. This demonstrates that CARP can be calibrated on actual interdependent risk systems and that its predictive precision can be quantified even when only one historical record is available.

A sensitivity analysis further explores how perturbations of the recovered parameters (adding or subtracting one standard deviation) affect model outputs. Across four scenarios—using the true target values, the mean recovered values, mean + σ, and mean – σ—the authors observe only minor differences in the estimated durations of operational, burning, and recovery states, indicating that the inference procedure is relatively insensitive to moderate parameter fluctuations.

In summary, the paper makes three principal contributions:

- Model Innovation – CARP explicitly incorporates risk interdependencies and multi‑state dynamics within a unified stochastic framework.

- Quantitative Limits of Predictability – By generating synthetic ground truth and systematically varying data length, the authors empirically establish that parameter‑recovery error shrinks as a power law (exponent ≈ –0.5), providing a concrete rule for how much historical data is needed to achieve a desired prediction precision.

- Real‑World Validation – Applying CARP to the World Economic Forum risk network confirms that the same error‑decay behavior holds for actual global risk data, supporting the model’s practical relevance.

The findings suggest that CARP can serve as an efficient tool for forecasting cascading catastrophic events, with clear guidance on the data requirements for reliable risk assessment. Future work could extend the model to incorporate real‑time data streams, explore additional risk domains (e.g., power‑grid failures, pandemics), and integrate mitigation strategies to evaluate how interventions alter the cascade dynamics.

Comments & Academic Discussion

Loading comments...

Leave a Comment