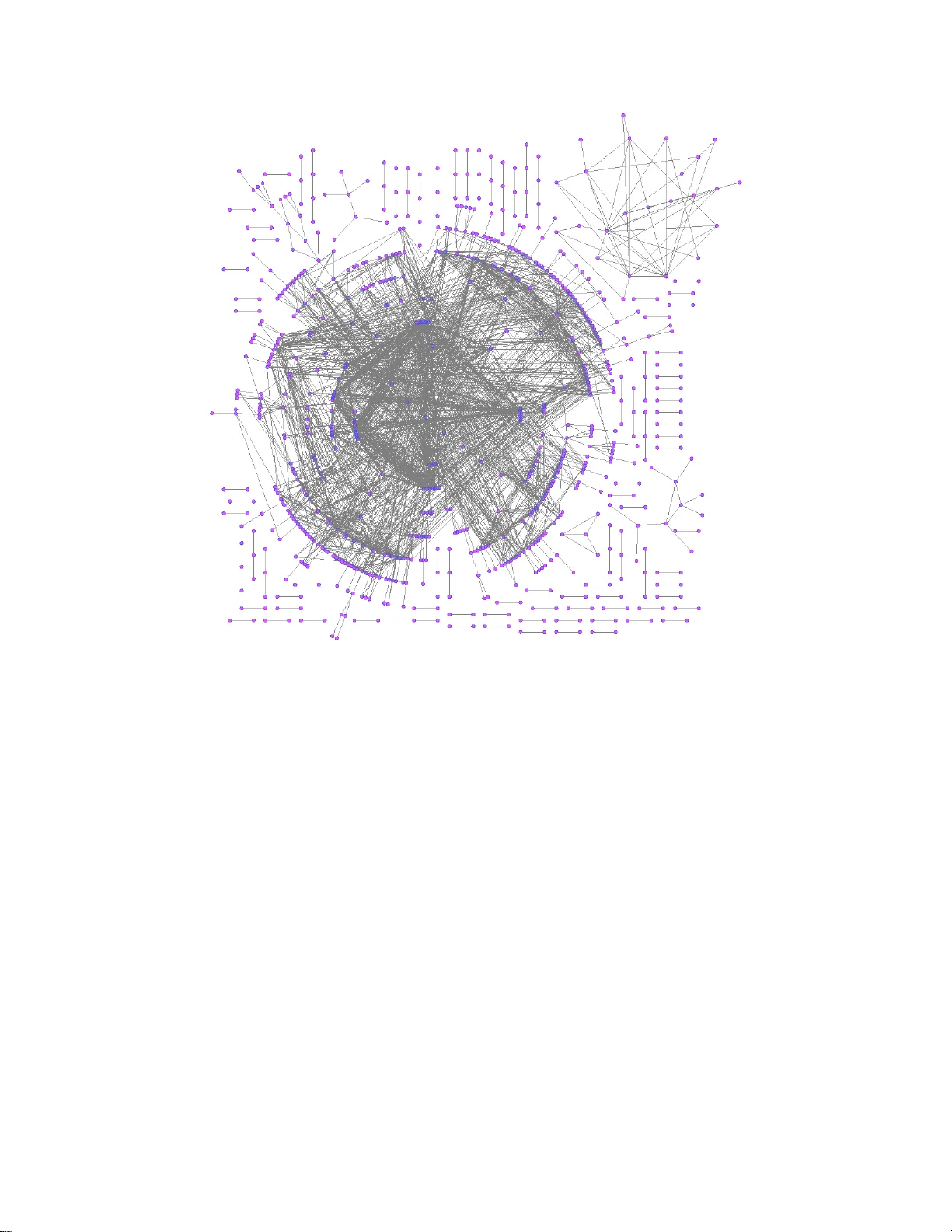

Large Scale Correlation Screening

This paper treats the problem of screening for variables with high correlations in high dimensional data in which there can be many fewer samples than variables. We focus on threshold-based correlation screening methods for three related applications…

Authors: Alfred O. Hero, Bala Rajaratnam