Dynamic stochastic blockmodels: Statistical models for time-evolving networks

Significant efforts have gone into the development of statistical models for analyzing data in the form of networks, such as social networks. Most existing work has focused on modeling static networks, which represent either a single time snapshot or…

Authors: Kevin S. Xu, Alfred O. Hero III

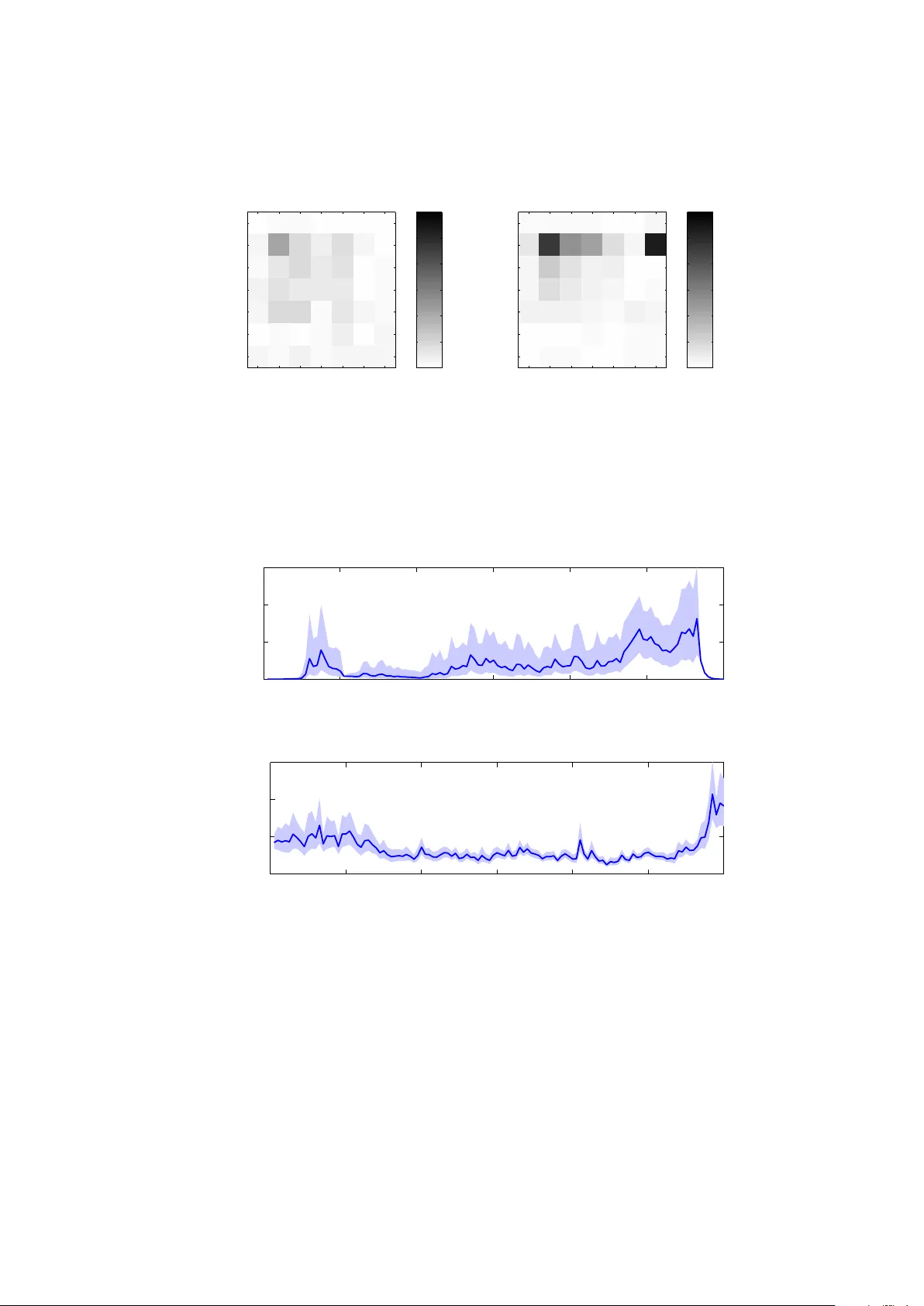

Dynamic sto c hastic blo c kmo dels: Statistical mo dels for time-ev olving net w orks Kevin S. Xu ? and Alfred O. Hero I II Departmen t of Electrical Engineering and Computer Science, Univ ersity of Michigan, Ann Arbor, MI, USA {xukevin, hero}@umich.edu Abstract. Significan t efforts hav e gone into the dev elopment of statis- tical mo dels for analyzing data in the form of netw orks, such as so cial net works. Most existing work has focused on mo deling static net works, whic h represen t either a single time snapshot or an aggregate view o ver time. There has b een recent interest in statistical mo deling of dynamic networks , whic h are observ ed at m ultiple points in time and offer a ric her represen tation of many complex phenomena. In this paper, we prop ose a state-space mo del for dynamic netw orks that extends the well-kno wn sto chastic blockmo del for static net works to the dynamic setting. W e then prop ose a procedure to fit the mo del using a modification of the extended Kalman filter augmen ted with a lo cal search. W e apply the pro cedure to analyze a dynamic so cial netw ork of email communication. Keyw ords: dynamic net work, sto c hastic blo c kmo del, state-space model 1 In tro duction Man y complex ph ysical, biological, and so cial phenomena are naturally repre- sen ted by net works. T remendous efforts ha ve b een dedicated to analyzing net- w ork data, which has led to the developmen t of many formal statistical mo dels for netw orks. Most research has fo cused on static netw orks, which either repre- sen t a single time snapshot of the phenomenon being inv estigated or an aggregate view o ver time. As such, statistical models for static net w orks ha ve a long history in statistics and so ciology among other fields [2]. How ever, most complex phe- nomena, including so cial b eha vior, are time-v arying, whic h has led researchers to consider dynamic, time-ev olving netw orks. In this pap er, we consider dynamic net works represented by a sequence of snapshots of the netw ork at discrete time steps. W e characterize suc h net works using a set of unobserved time-varying states from whic h the observ ed snapshots are derived. W e propose a state-space mo del for dynamic netw orks that com bines t wo t yp es of statistical mo dels: a static mo del for the individual snapshots and a temp oral mo del for the evolution of the states. The netw ork snapshots are mo d- eled using the stochastic blockmodel [5], a simple parametric mo del commonly ? Curren t affiliation: 3M Corp orate Researc h Lab oratory , St. Paul, MN, USA 2 Kevin S. Xu and Alfred O. Hero I II used in the analysis of static so cial net works. The state evolution is mo deled b y a stochastic dynamic system. Using a Cen tral Limit Theorem appro ximation, w e dev elop a near-optimal pro cedure for fitting the prop osed mo del in the on-line setting where only past and present netw ork snapshots are av ailable. The infer- ence pro cedure in volv es a mo dification of the extended Kalman filter, which is used for state tracking in many applications [3], augmented with a lo cal search strategy . W e apply the prop osed pro cedure to analyze a dynamic so cial netw ork of email comm unication and predict future email activity . 2 Related w ork Sev eral statistical mo dels for dynamic netw orks ha ve previously been prop osed b y extending a static mo del to the dynamic setting in a similar fashion to our prop osed mo del [2]. Two such mo dels include temp oral extensions of the expo- nen tial random graph mo del [1] and laten t space model [13]. More closely related to the state-space mo del we prop ose are several temp oral extensions of sto c has- tic blo c kmo dels (SBMs). SBMs divide no des in the netw ork into m ultiple classes and generate edges indep enden tly with probabilities θ ab dep enden t on the class mem b erships a, b of the no des [5]. Y ang et al. [15] propos e a dynamic SBM in- v olving a transition matrix that sp ecifies the probabilit y that a no de in class i at time t switches to class j at time t + 1 for all i, j, t and fit the mo del using Gibbs sampling and simu lated annealing. Ho et al. [4] prop ose a temp oral extension of a mixed-membership version of the SBM using linear state-space mo dels for the class membership vectors of no de clusters. One ma jor difference b etw een [4, 15] and this pap er is that w e treat the edge probabilities θ ab as time-varying states , while [4, 15] treat them as time-in v ariant parameters. In addition, our mo del allows for a simpler inference pro cedure using a Central Limit Theorem appro ximation. W e demonstrate the imp ortance of the time-v arying states for analysis of a dynamic so cial netw ork in Section 5. 3 Static sto c hastic blo c kmo dels W e first in tro duce notation and summarize the static sto c hastic blockmodel (SSBM), whic h w e use as the static model for the individual net work snap- shots. W e represent a dynamic netw ork by a time-indexed sequence of graphs, with W t = [ w t ij ] denoting the adjacency matrix of the graph observed at time step t . w t ij = 1 if there is an edge from no de i to no de j at time t , and w t ij = 0 otherwise. W e assume that the graphs are directed, i.e. w t ij 6 = w t j i in general, and that there are no self-edges, i.e. w t ii = 0. W ( s ) denotes the set of all snapshots up to time s , { W s , W s − 1 , . . . , W 1 } . The notation i ∈ a indicates that no de i is a member of class a . | a | denotes the n umber of no des in class a . The classes of all no des at time t is given b y a vector c t with c t i = a if i ∈ a at time t . W e denote the submatrix of W t corresp onding to the relations betw een no des in class a and class b by W t [ a ][ b ] . W e denote the v ectorized equiv alent of a matrix X , Dynamic sto c hastic blo c kmo dels 3 i.e. the v ector obtained by simply stac king columns of X on top of one another, b y x . Doubly-indexed subscripts such as x ij denote entries of matrix X , while singly-indexed subscripts suc h as x i denote en tries of the vectorized equiv alent x . Consider a snapshot at an arbitrary time step t . An SSBM is parameterized b y a k × k matrix Θ t = [ θ t ab ], where θ t ab denotes the probabilit y of forming an edge b et w een a no de in class a and a no de in class b , and k denotes the n umber of classes. The SSBM decomp oses the adjacency matrix in to k 2 blo c ks, where each block is asso ciated with relations b et ween no des in tw o classes a and b . Each blo c k corresp onds to a submatrix W t [ a ][ b ] of the adjacency matrix W t . Th us, given the class membership vector c t , eac h entry of W t is an indep enden t realization of a Bernoulli random v ariable with a blo ck-dependent parameter; that is, w t ij ∼ Bernoulli θ t c t i c t j . SBMs are used in t wo settings: 1. The a priori blo c kmo deling setting, where class memberships are known or assumed, and the ob jectiv e is to estimate the matrix of e dge pr ob abilities Θ t . 2. The a p osteriori blo c kmo deling setting, where the ob jectiv e is to simultane- ously estimate Θ t and the class mem b ership v ector c t . Since eac h entry of W t is indep enden t, the lik eliho o d for the SBM is given by f W t ; Φ t = Y i 6 = j θ t c i c j w t ij 1 − θ t c i c j 1 − w t ij = exp ( k X a =1 k X b =1 m t ab log θ t ab + n t ab − m t ab log 1 − θ t ab ) , (1) where m t ab = P i ∈ a P j ∈ b w t ij denotes the n umber of observe d edges in block ( a, b ), and n t ab = ( | a || b | a 6 = b | a | ( | a | − 1) a = b (2) denotes the num b er of p ossible edges in blo c k ( a, b ) [6]. The parameters are given b y Φ t = Θ t in the a priori setting, and Φ t = { Θ t , c t } in the a p osteriori setting. In the a priori setting, a sufficien t statistic for estimating Θ t is the matrix Y t of blo ck densities (ratio of observ ed edges to p ossible edges within a blo ck) with en tries y t ab = m t ab /n t ab . Y t also happens to b e the maxim um-likelihoo d estimate of Θ t , whic h can b e sho wn [6] by setting the deriv ative of the logarithm of (1) to 0. Estimation in the a p osteriori setting is more in volv ed, and many metho ds ha ve b een prop osed, including Gibbs sampling [8], labe l-switc hing [6, 16], and sp ectral clustering [12]. The label-switching metho ds use a heuristic for solving the combinatorial optimization problem of maximizing the likelihoo d (1) ov er the set of p ossible class memberships, which is to o large to p erform an exhaustive searc h. 4 Kevin S. Xu and Alfred O. Hero I II 4 Dynamic sto c hastic blo c kmo dels W e prop ose a state-space mo del for dynamic netw orks that consists of a tem- p oral extension of the static sto c hastic blo ckmodel. First we presen t the mo del and inference procedure for a priori blo c kmo deling, and then we discuss the ad- ditional steps necessary for a p osteriori blo c kmo deling. The inference pro cedure is on-line, i.e. the state estimate at time t is formed using only observ ations from time t and earlier. 4.1 A priori blo c kmo dels In the a priori SSBM setting, Y t is a sufficien t statistic for estimating Θ t as discussed in Section 3. Thus in the a priori dynamic SBM setting, we can equiv- alen tly treat Y t as the observ ation rather than W t . The entries of W t [ a ][ b ] are indep enden t and iden tically distributed (iid) Bernoulli ( θ t ab ); th us by the Cen tral Limit Theorem, the sample mean y t ab is appro ximately Gaussian with mean θ t ab and v ariance ( σ t ab ) 2 = θ t ab (1 − θ t ab ) /n t ab , where n t ab w as defined in (2). W e assume that y t ab is indeed Gaussian for all ( a, b ) and p osit the linear observ ation mo del Y t = Θ t + Z t , where Z t is a zero-mean iid Gaussian noise matrix with v ariance ( σ t ab ) 2 for the ( a, b )th entry . In the dynamic setting where past snapshots are av ailable, the observ ations w ould b e given by the set Y ( t ) . The set Θ ( t ) can then b e viewed as states of a dynamic system that is generating the noisy observ ation sequence. W e complete the mo del b y sp ecifying a mo del for the state evolution o ver time. Since θ t ab is a probability and m ust b e b ounded b et ween 0 and 1, we instead w ork with the matrix Ψ t = [ ψ t ab ] where ψ t ab = log( θ t ab ) − log (1 − θ t ab ), the logit of θ t ab . A simple mo del for the state evolution is the random walk ψ t = ψ t − 1 + v t , where ψ t is the v ector representation of the matrix Ψ t , and v t is a random v ector of zero-mean Gaussian entries, commonly referred to as pro cess noise, with co v ariance matrix Γ t . The entries of the pro cess noise vector are not necessarily indep enden t or identically distributed (unlike the entries of Z t ) to allow for states to evolv e in a correlated manner. The observ ation mo del can then b e written in terms of ψ t as 1 y t = h ψ t + z t , (3) where the function h : R k 2 → R k 2 is defined by h i ( x ) = 1 / (1 + e − x i ), i.e. the logistic function applied to each entry of x . W e denote the cov ariance matrix of z t b y Σ t , which is a diagonal matrix 2 with entri es given b y ( σ t ab ) 2 . A graphical represen tation of the proposed model for the dynamic netw ork is shown in Fig. 1. 1 Note that w e hav e conv erted the block densities Y t and observ ation noise Z t to their resp ectiv e vector representations y t and z t . 2 The indices ( a, b ) for ( σ t ab ) 2 are conv erted into a single index i corresponding to the v ector representation z t . Dynamic sto c hastic blo c kmo dels 5 Logistic SBM . . . Fig. 1. Graphical representation of the prop osed mo del. The rectangular b o xes denote observ ed quantities, and the ov als denote unobserved quantities. The logistic SBM refers to applying the logistic function to each en try of Ψ t to obtain Θ t then generating W t using Θ t and c t . T o p erform inference on this mo del, we assume the initial state is Gaussian distributed, i.e. ψ 0 ∼ N µ 0 , Γ 0 , and that { ψ 0 , v 1 , . . . , v t , z 1 , . . . , z t } are mu- tually indep enden t. If (3) w as linear in ψ t , then the optimal estimate of ψ t in terms of minim um mean-squared error would b e giv en by the Kalman filter [3]. Due to the non-linearity , we apply the extended Kalman filter (EKF), which linearizes the dynamics ab out the predicted state and provides an near-optimal estimate of ψ t . The predicted state under the random walk mo del is simply ˆ ψ t | t − 1 = ˆ ψ t − 1 | t − 1 with cov ariance R t | t − 1 = R t − 1 | t − 1 + Γ t . Let J t denote the Ja- cobian of h ev a luated at the predicted state ˆ ψ t | t − 1 . The EKF up date equations are as follo ws [3]: Near-optimal Kalman gain: K t = R t | t − 1 J t T h J t R t | t − 1 J t T + Σ t i − 1 P osterior state estimate: ˆ ψ t | t = ˆ ψ t | t − 1 + K t h y t − h ˆ ψ t | t − 1 i P osterior estimate cov ariance: R t | t = I − K t J t R t | t − 1 The p osterior state estimate ˆ ψ t | t pro vides a near-optimal fit to the mo del at time t given the observed sequence W ( t ) . How to c ho ose the hyperparameters µ 0 , Γ 0 , Σ t , Γ t in an optimal manner is b eyond the scop e of this pap er and is discussed in [14, c hap. 5]. 4.2 A p osteriori blo c kmo dels In many applications, the class memberships c t are not known a priori and must b e estimated along with Ψ t . This can b e done using lab el-switching metho ds [6, 16], but rather than maximizing the likelihoo d, we maximize the p osterior state density given the entire sequence of observ ations W ( t ) up to time t to accoun t for the prior information. This is done by alternating b etw een lab el- switc hing and applying the EKF. 6 Kevin S. Xu and Alfred O. Hero I II The p osterior state density is given by f ψ t | W ( t ) ∝ f W t | ψ t , W ( t − 1) f ψ t | W ( t − 1) . (4) By the conditional indep endence of current and past observ ations given the cur- ren t state, W ( t − 1) drops out of the first term in (4). It can thus b e obtained simply b y substituting h ( ψ t ) for θ t in (1). The second term in (4) is equiv alent to f ψ t | y ( t − 1) b ecause the class mem b erships at all previous time steps hav e already b een estimated. By applying the Kalman filter to the linearized tem- p oral mo del [3], f ψ t | y ( t − 1) ∼ N ˆ ψ t | t − 1 , R t | t − 1 . Thus the logarithm of the p osterior density is given by log f ψ t | W ( t ) = c − 1 2 ψ t − ˆ ψ t | t − 1 T R t | t − 1 − 1 ψ t − ˆ ψ t | t − 1 + k X a =1 k X b =1 m t ab log h ψ t ab + n t ab − m t ab log 1 − h ψ t ab , (5) where c is a constan t term indep enden t of ψ t that can b e ignored 3 . W e use the log-p osterior (5) as the ob jective function for lab el-switc hing. W e find that a simple lo cal search (hill climbing) algorithm [11] initialized using the estimated class memberships at the previous time step suffices, b ecause only a small fraction of no des change classes betw een time steps in most applications. A t the initial time step, w e employ the sp ectral clustering algorithm of Sussman et al. [12] for the SSBM as the initialization. 5 Application to Enron email net w ork W e demonstrate the prop osed pro cedure on a dynamic so cial netw ork con- structed from the Enron corpus [9, 10], which consists of ab out 0 . 5 million email messages b et ween 184 Enron employ ees from 1998 to 2002. W e place directed edges betw een emplo yees i and j at time t if i sends at least one email to j during w eek t . Each time step corresponds to a 1-week in terv al. W e make no distinction b et w een emails sen t “to”, “cc”, or “b cc”. In addition to the email data, the roles of most of the employ ees within the company (e.g. CEO, president, manager, etc.) are a v ailable, whic h we use as classes for a priori blockmodeling. Employ ees with unkno wn roles are placed in an “others” class. 5.1 State tracking W e b egin by examining the temp oral v ariation of the states, which we refer to as state tr acking . Recall that the states Ψ t corresp ond to the logit of the edge probabilities Θ t . W e first apply the a priori EKF to obtain the state estimates ˆ ψ t | t and their v ariances (the diagonal of R t | t ). Applying the logistic function, we can then obtain the estimated edge probabilities ˆ Θ t | t with confidence in terv als. 3 A t the initial time step, ˆ ψ 1 | 0 = µ 0 and R 1 | 0 = Γ 0 + Γ 1 . Dynamic sto c hastic blo c kmo dels 7 Recipient class Sender class 1 2 3 4 5 6 7 1 2 3 4 5 6 7 0 0.1 0.2 0.3 0.4 0.5 0.6 (a) W eek 59: a normal week Recipient class Sender class 1 2 3 4 5 6 7 1 2 3 4 5 6 7 0 0.1 0.2 0.3 0.4 0.5 0.6 (b) W eek 89: CEO Skilling resigns Fig. 2. Estimated edge probabilit y matrices for tw o selected w eeks. En try ( i, j ) denotes the estimated probability of an edge from class i to class j . Classes are as follo ws: (1) directors, (2) CEOs, (3) presidents, (4) vice-presidents, (5) managers, (6) traders, and (7) others. Notice the increase in the probability of edges from CEOs during the week of Skilling’s resignation. 0 20 40 60 80 100 120 0 0.2 0.4 0.6 Week Edge probability (a) Presidents to presidents 0 20 40 60 80 100 120 0 0.05 0.1 0.15 Week Edge probability (b) Others to others Fig. 3. A priori EKF estimated edge probabilities ˆ θ t | t ab (solid lines) with 95% confidence in terv als (shaded region) for selected a, b b y week. An increase in edge probabilities b et w een Enron presidents (a) o ccurs prior to a similar increase b et ween those in other roles (b) suggesting insider knowledge. 8 Kevin S. Xu and Alfred O. Hero I II Examining the temporal v ariation of ˆ Θ t | t rev eals some in teresting trends. F or example, a large increase in the probabilities of edges from CEOs is found at w eek 89. This is the w eek in whic h CEO Jeffrey Skilling resigned and is confirmed to b e the cause of the increased probabilities b y examining the con tent of the emails. Fig. 2 shows a comparison of the matrix ˆ Θ t | t during a normal week and during the w eek Skilling resigned. Another in teresting trend is highlighted in Fig. 3, where the temp oral v ari- ation of tw o selected edge probabilities ov er the en tire data trace with 95% confidence interv als is shown. Edge probabilities b et ween Enron presiden ts show a steady increase as Enron’s financial situation worsens, hinting at more fre- quen t and widespread insider discussions, while emails b et ween others (not of one of the six known roles) b egin to increase only after Enron falls under federal in vestigation. A key observ ation from this analysis is the imp ortance of mo deling the edge probabilities as time-v arying states, as opp osed to time-inv arian t parameters as in [4, 15]. Indeed the temp or al variation of the edge probabilities is what rev eals the internal dynamics of this time-ev olving social net work. F urthermore, the temp oral mo del pro vides estimates with less uncertaint y than the static SBM, with 95% confidence in terv als that are 24% narrow er on av erage. 5.2 Dynamic link prediction Next w e turn to the task of dynamic link prediction, which differs from static link prediction [7] b ecause the link predictor m ust simultaneously predict the new edges that will b e formed at time t + 1, as well as the current edges (as of time t ) that will disapp ear at time t + 1, from the observ ations W ( t ) . The latter task is not addressed b y most static link prediction metho ds in the literature. Since the SBM assumes sto c hastic equiv alence b etw een no des in the same class, the EKF alone is only a goo d predictor of the block densities Y t , not the edges themselv es. How ever, the EKF can b e combined with a predictor that operates on individual edges to form a link predictor. A simple individual- lev el predictor is the exp onen tially-weigh ted moving a verage (EWMA) given by ˆ W t +1 = λ ˆ W t + (1 − λ ) W t . Using a conv ex com bination of the EKF and EWMA predictors, w e obtain a b etter link predictor that incorp orates b oth blo c k-level c haracteristics (through the EKF) and individual-lev el c haracteristics (through the EWMA). This can b e seen from the receiver op erating c haracteristic (ROC) curv es in Fig. 4. The a p osteriori EKF slightly outp erforms the a priori EKF b ecause the a p osteriori EKF finds a b etter fit to the dynamic SBM via a b etter assignmen t of no des to classes than the a priori (assumed) assignment. 6 Conclusion This pap er prop oses a statistical mo del for dynamic net works that utilizes a set of unobserved time-v arying states to c haracterize the dynamics of the net work. The prop osed mo del extends the well-kno wn sto c hastic blo c kmo del for static Dynamic sto c hastic blo c kmo dels 9 0 0.2 0.4 0.6 0.8 1 0 0.2 0.4 0.6 0.8 1 False positive rate True positive rate A priori EKF + EWMA A posteriori EKF + EWMA EWMA Fig. 4. Comparison of ROC curv es for link prediction on Enron data. T rue p ositiv e rate denotes the fraction of actual edges that are correctly predicted, and false p ositive rate denotes the fraction of non-edges that are predicted to b e edges. The conv ex com- bination of either EKF with the EWMA outp erforms the EWMA alone by accounting for blo c k-level characteristics. net works to the dynamic setting can b e used for either a priori or a p osteriori blo c kmo deling. The main contribution of the pap er is a near-optimal on-line in- ference pro cedure for the prop osed mo del using a mo dification of the extended Kalman filter, augmen ted with a local search. W e applied the proposed inference pro cedure to the Enron email netw ork and disco vered some interesting trends when w e examined the estimated states. One such trend w as a steady increase in emails b et ween Enron presidents as Enron’s financial situation worsened, while emails b et w een other employ ees remained at their baseline levels un til Enron fell under federal inv estigation. In addition, the prop osed pro cedure show ed promis- ing results for predicting future email activity . W e b eliev e the prop osed mo del and inference pro cedure can b e applied to rev eal the internal dynamics of many other dynamic net works. Ac knowledgmen ts. This work w as partially supp orted by the Army Research Office grant W911NF-12-1-0443. Kevin Xu was partially supp orted by an aw ard from the Natural Sciences and Engineering Researc h Council of Canada. References [1] Ahmed, A., Xing, E.P .: Recov ering time-v arying netw orks of dep endencies in so cial and biological studies. Pro c. Nat. Acad. Sci. 106(29), 11878–11883 (2009) 10 Kevin S. Xu and Alfred O. Hero I II [2] Golden b erg, A., Zheng, A.X., Fien b erg, S.E., Airoldi, E.M.: A survey of sta- tistical net work mo dels. F ound. T rends Mach. Learn. 2(2), 129–233 (2010) [3] Ha ykin, S.: Kalman filtering and neural netw orks. Wiley-Interscience (2001) [4] Ho, Q., Song, L., Xing, E.P .: Evolving cluster mixed-mem b ership blo ck- mo del for time-v arying net works. In: Pro ceedings of the 14th Int. Conf. Artif. In tell. Statist. (2011) [5] Holland, P .W., Laskey , K.B., Leinhardt, S.: Sto chastic blo c kmo dels: First steps. So c. Netw. 5(2), 109–137 (1983) [6] Karrer, B., Newman, M.E.J.: Sto c hastic blockmodels and communit y struc- ture in net works. Phys. Rev. E 83, 016107 (2011) [7] Lib en-No w ell, D., Klein b erg, J.: The link-prediction problem for so cial net- w orks. J. Am. So c. Inf. Sci. 58(7), 1019–1031 (2007) [8] No wicki, K., Snijders, T.A.B.: Estimation and prediction for sto c hastic blo c kstructures. J. Am. Stat. Asso c. 96(455), 1077–1087 (2001) [9] Prieb e, C.E., Conroy , J.M., Marchette, D.J., P ark, Y.: Scan statistics on Enron graphs. Comput. Math. Organ. Theory 11(3), 229–247 (2005) [10] Prieb e, C.E., Conroy , J.M., Marchette, D.J., P ark, Y.: Scan statistics on Enron graphs (2009), http://cis.jhu.edu/ ~ parky/Enron/enron.html [11] Russell, S.J., Norvig, P .: Artificial in telligence: A mo dern approach. Pren tice Hall, 2nd edn. (2003) [12] Sussman, D.L., T ang, M., Fishkind, D.E., Prieb e, C.E.: A consis- ten t adjacency spectral em b edding for sto c hastic blo ckmodel graphs. arXiv:1108.2228v3 [stat.ML] (2012) [13] W estveld, A.H., Hoff, P .D.: A mixed effects model for longitudinal relational and net w ork data, with applications to in ternational trade and conflict. Ann. Appl. Stat. 5(2A), 843–872 (2011) [14] Xu, K.S.: Computational metho ds for learning and inference on dynamic net works. Ph.D. thesis, Universit y of Mic higan (2012) [15] Y ang, T., Chi, Y., Zhu, S., Gong, Y., Jin, R.: Detecting communities and their ev olutions in dynamic so cial netw orks—a Bay esian approac h. Mach. Learn. 82(2), 157–189 (2011) [16] Zhao, Y., Levina, E., Zh u, J.: Consistency of communit y detection in net- w orks under degree-corrected stochastic blo c k models. The Annals of Statis- tics (in press) (2012)

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment