Pathwidth, trees, and random embeddings

We prove that, for every $k=1,2,...,$ every shortest-path metric on a graph of pathwidth $k$ embeds into a distribution over random trees with distortion at most $c$ for some $c=c(k)$. A well-known conjecture of Gupta, Newman, Rabinovich, and Sinclai…

Authors: James R. Lee, Anastasios Sidiropoulos

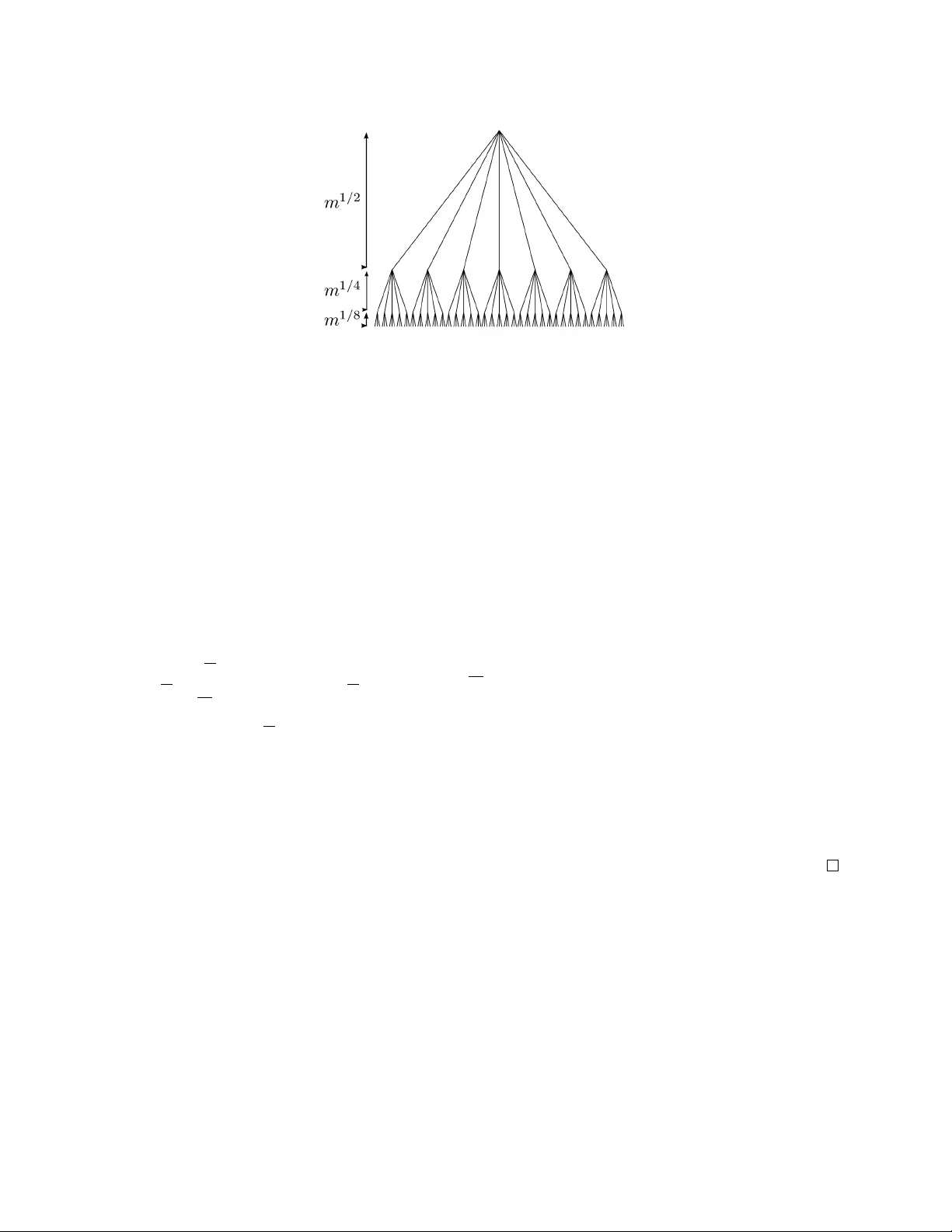

P ath width, trees, and random em b eddings James R. Lee † Anastasios Sidirop oulos ‡ Abstract W e pro v e that, for every in teger k ≥ 1, ev ery shortest-path metric on a graph of pathwidth k em b eds into a distribution o v er random trees with distortion at most c = c ( k ), indep endent of the graph size. A w ell-known conjecture of Gupta, Newman, Rabino vich, and Sinclair [GNRS04] states that for every minor-closed family of graphs F , there is a constant c ( F ) suc h that the m ulti-commo dit y max-flow/min-cut gap for every flo w instance on a graph from F is at most c ( F ). The preceding embedding theorem is used to prov e this conjecture whenever the family F do es not con tain all trees. 1 In tro duction W e view an undirected graph G = ( V , E ) as a top ological template that supp orts a n um b er of differen t geometries. Such a geometry is sp ecified b y a non-negativ e length function len : E → [0 , ∞ ) on edges, whic h induces a shortest-path pseudometric d len on V , with d len ( u, v ) = length of the shortest path b etw een u and v in G, where a pseudometric migh t ha ve d len ( u, v ) = 0 for some pairs u, v ∈ V with u 6 = v . A pseudometric d is supp orte d on G if d = d len for some such len : E → [0 , ∞ ). F rom this p oint of view, we are in terested in prop erties whic h hold simultaneously for all geometries supp orted on G , or even for all geometries supp orted on a family of graphs F . In what follo ws, w e will deal exclusively with finite graphs and families of finite graphs unless explicitly stated otherwise. In the seminal works of Linial-London-Rabinovic h [LLR95] and Aumann-Rabani [AR98], and later Gupta-Newman-Rabinovic h-Sinclair [GNRS04], the geometry of graphs is related to the clas- sical study of the relationship b etw een flows and cuts. Multi-commo dit y flo ws and L 1 em b eddings. F or a metric space ( X , d ), we use c 1 ( X , d ) to denote the L 1 distortion of ( X , d ), i.e. the infim um o v er all n um b ers D such that X admits an em b edding f : X → L 1 with d ( x, y ) ≤ k f ( x ) − f ( y ) k 1 ≤ D · d ( x, y ) for all x, y ∈ X . Here, w e hav e L 1 = L 1 ([0 , 1]), whic h can b e replaced b y the sequence space ` 1 when X is finite. ∗ A portion of the results in this pap er w ere announced at the 41st Annual Symposium on the Theory of Computing [LS09]. † Computer Science & Engineering, Univ ersity of W ashington. Research partially supp orted by NSF grant CCF- 0644037 and a Sloan Research F ellowship. E-mail: jrl@cs.washington.edu . ‡ T oy ota T echnological Institute at Chicago. E-mail: tasos@ttic.edu . 1 Corresp onding to the preceding discussion, for a graph G = ( V , E ) w e write c 1 ( G ) = sup c 1 ( V , d ) where d ranges ov er all metrics supp orted on G . F or a family F of graphs, w e write c 1 ( F ) = sup G ∈F c 1 ( G ). Th us for a family F of finite graphs, c 1 ( F ) ≤ D if and only if every geometry supp orted on a graph in F embeds into L 1 with distortion at most D . A multi-c ommo dity flow instanc e in G is specified b y a pair of non-negativ e mappings cap : E → R and dem : V × V → R . W e write maxflow ( G ; cap , dem) for the v alue of the maximum c oncurr ent flow in this instance, which is the maximal v alue ε suc h that a flow of v alue ε · dem( u, v ) can b e sim ultaneously routed b etw een every pair u, v ∈ V while not violating the given edge capacities. A natural upp er b ound on maxflow ( G ; cap , dem) is given by the sp arsity of any cut S ⊆ V : Φ( S ; cap , dem) = P uv ∈ E cap( u, v ) | 1 S ( u ) − 1 S ( v ) | P u,v ∈ V dem( u, v ) | 1 S ( u ) − 1 S ( v ) | , (1) where 1 S : V → { 0 , 1 } is the indicator function for mem b ership in S . In the case where dem( u, v ) > 0 for exactly one pair u, v , also known as single-c ommo dity flow [FF56], minimizing the upp er b ound (1) ov er all cuts S ⊆ V computes the minimum u - v cut in G , and the max-flow/min-cut theorem states that this upp er b ound is achiev ed by the corresp onding maxim um flow. In general, w e write gap ( G ) = sup cap , dem min S ⊆ V Φ( S ; cap , dem) maxflo w ( G ; cap , dem) . for the maxim um ratio b etw een the b est upp er b ound given b y (1) and the v alue of the flo w, o v er all multi-commodity flo w instances on G . This is the multi-c ommo dity max-flow/min-cut gap for G . Now w e can state the fundamental relationship b etw een the geometry of graphs and the flows they supp ort: Theorem 1.1 ([LLR95, GNRS04]) . F or every gr aph G , c 1 ( G ) = gap ( G ) . In the general Sparsest Cut problem (also kno wn as Sparsest Cut with general demands), given G , cap, and dem, we wan t to find a cut in G of minimum sparsity . Combined with the techniques of [LR99, LLR95], Theorem 1.1 implies that there exists a c 1 ( G )-appro ximation for the general Sparsest Cut problem on a graph G . Motiv ated by this connection, Gupta, Newman, Rabino vich, and Sinclair sought to char acterize the graph families F suc h that c 1 ( F ) < ∞ , and they p osed the follo wing conjecture. W e will say that a family of graphs F forbids some minor if there exists a graph G that is not a minor of any graph in F . Conjecture 1 ([GNRS04]) . F or every family of finite gr aphs F , one has c 1 ( F ) < ∞ if and only if F forbids some minor. W e refer to Section 1.3 for a review of graph minors. Progress on the preceding conjecture has b een limited. Classical work of Ok amura and Seymour [OS81] implies that c 1 ( Outerplana r ) = 1, where Outerplanar denotes the class of outerplanar graphs (planar graphs where all vertices lie on a single face). Gupta, Newman, Rabinovic h, and Sinclair [GNRS04] prov ed that c 1 ( T reewidth (2)) = O (1), where T reewidth ( k ) denotes the family of all graphs of treewidth at most k (see, e.g. [Die05] for a discussion of treewidth, or Section 1.3 for the relev ant definitions). This w as improv ed to c 1 ( T reewidth (2)) = 2 in [LR10, CJL V08]. Finally , in [CGN + 06], it is sho wn that c 1 ( Outerplana r ( k )) < 2 O ( k ) for all k ∈ N , where Outerplanar ( k ) denotes the class of k -outerplanar graphs. W e remark that a strengthening of Conjecture 1, regarding integer m ulti-commo dity flows, has been in v estigated b y Chekuri, Shepherd, and W eib el [CSW10]. The present paper is dev oted to proving the following sp ecial case of Conjecture 1. 2 Theorem 1.2. Every minor-close d family of finite gr aphs F which do es not c ontain every p ossi- ble tr e e satisfies c 1 ( F ) < ∞ . Equivalently, the multi-c ommo dity max-flow/min-cut gap for F is uniformly b ounde d, i.e. gap ( F ) < ∞ , whenever F has b ounde d p athwidth. W e remark that Theorem 1.2 implies a p olynomial-time O (1)-approximation algorithm for the general Sparsest Cut problem on graphs of b ounded pathwidth. Recently , an O (1)-approximation algorithm for graphs of b ounded treewidth has b een obtained b y Chlam tac, Krauthgamer, and Ragha vendra [CKR10]. W e also note that [CKR10] uses a differen t approach, and do es not es- tablish an analogous b ound on the multi-commodity max-flo w/min-cut gap for graphs of b ounded treewidth (whic h remains an imp ortant op en problem). 1.1 Simplifying the top ology with random embeddings A basic question is whether one can embed a graph metric G into a graph metric H with a simpler top ology (for example, p erhaps G is planar and H is a tree), where the embedding is required to ha ve small distortion, i.e. such that every pairwise distance c hanges by only a b ounded amount. The viability of this approach as a general metho d was ruled out by Rabino vich and Raz [RR98]. F or instance, Ω( n ) distortion is required to embed an n -cycle into a tree. In general (see [CG04]), if all metrics supp orted on a sub division of some graph G can b e embedded with distortion O (1) in to metrics supp orted on a family F , then G is a minor of some graph in F , implying that we ha ve not obtained a reduction in top ological complexity . On the other hand, a classical example attributed to Karp [Kar89] shows that random reductions migh t still b e effective: If one remo ves a uniformly random edge from the n -cycle, this giv es an em b edding into a random tree which has distortion at most 2 “in exp ectation.” More formally , if ( X , d ) is an y finite metric space, and Y is a family of finite metric spaces, w e sa y that ( X , d ) admits a sto chastic D -emb e dding into Y if there exists a randomly c hosen metric space ( Y , d Y ) ∈ Y and a randomly c hosen mapping F : X → Y such that the follo wing tw o prop erties hold. Non-con tracting. With probability one, for every x, y ∈ X , w e ha ve d Y ( F ( x ) , F ( y )) ≥ d ( x, y ). Lo w-expansion. F or every x, y ∈ X , E h d Y ( F ( x ) , F ( y )) i ≤ D · d ( x, y ) . F or t wo graph families F and G , we write F G if there exists a D < ∞ suc h that every metric supp orted on F admits a sto chastic D -em b edding into the family of metrics supp orted on G . W e will write F D G if we wish to emphasize the particular constant. Finally , w e write F 6 G if no suc h D exists. The relationship with Conjecture 1 is given by the follo wing simple lemma (see, e.g. [GNRS04]). Lemma 1.3. If F D G , then c 1 ( F ) ≤ D · c 1 ( G ) . A t first glance, seems like a p o werful op eration; indeed, in [GNRS04] it is pro v ed that OuterPlana r T rees , where OuterPlanar and T rees are the families of outerplanar graphs and connected, acylic graphs, resp ectiv ely . In general, if L is a finite list of graphs, w e will write E L for the family of all graphs which do not ha ve a member of L as a minor. The preceding result can b e restated as E { K 2 , 3 } E { K 3 } , where K n and K m,n denote the complete and complete 3 bipartite graphs, resp ectively . Unfortunately , [GNRS04] also show ed that this cannot b e pushed m uch further: E { K 4 } 6 E { K 3 } . Restated, this means that ev en graphs of treewidth 2 cannot b e sto c hastically embedded into trees. These lo wer b ounds were extended in [CG04] to sho w that T reewidth ( k + 3) 6 T reewidth ( k ) for any k ≥ 1. Finally , in [CJL V08], these results are extended to any family with a weak closure prop ert y , which we describ e next. Sums of graphs. W e now introduce a graph op eration which will b e useful in stating our results. Supp ose that H and G are t wo graphs and C H , C G are k -cliques in H and G resp ectiv ely , for some k ≥ 1. One defines the k -sum of H and G as the graph H ⊕ k G which results from taking the disjoin t union of H and G and then iden tifying the t wo cliques C H and C G , and p ossibly remo ving a subset of the clique edges. W e remark that the notation is somewhat am biguous, as both the cliques and their iden tifications are implicit. F or a family of graphs F , w e write ⊕ k F for the closure of F under i -sums for every i = 1 , 2 , . . . , k . With this notation in hand, w e can state the following theorem. Theorem 1.4 ([CJL V08]) . If F and G ar e families of gr aphs and G is minor-close d, then ⊕ 2 F G implies F ⊆ G . In fact, one case of this theorem relies on Theorem 1.7 pro ved in the presen t pap er, which states that for every k = 1 , 2 , . . . , we hav e T rees ∩ P athwidth ( k + 1) 6 Pathwidth ( k ), where P athwidth ( k ) denotes the class of pathwidth- k graphs (see Section 1.3 for the relev ant definitions). Theorem 1.4 implies, for example, that Planar ∩ T reewidth ( k + 1) 6 T reewidth ( k ) for any k ≥ 1, where Plana r is the family of planar graphs, since planar graphs and b ounded treewidth graphs are b oth closed under 2-sums. The assumptions of the preceding theorem imply that ev en random em b eddings are not particularly useful for reducing the top ology when ⊕ 2 F = F . Ho wev er, some recen t reductions suggest that when ⊕ 2 F 6 = F , the situation is more hop eful. In [CGN + 06], it is pro v ed that Outerplanar ( k ) T rees . Perhaps more surprisingly , it is sho wn in [IS07] that Genus ( g ) Planar , where Genus ( g ) is the family of graphs em b edded on an orien table surface of gen us g , and Genus (0) = Planar . Note that while trees and planar graphs are closed under 2-sums, neither Outerplana r ( k ) nor Genus ( g ) are for k ≥ 1 and g ≥ 1. It should b e noted that an extensiv e amoun t of work has b een done on embedding finite metric spaces into distributions o ver trees, where the distortion is allo wed to depend on n , the num b er of p oints in the metric space; see, e.g. [Bar96, Bar98, FR T04]. These results are not particularly useful for us since we desire b ounds that are indep endent of n . 1.2 Results and techniques W e no w discuss the main results of the pap er, along with the techniques that go into pro ving them. In [GNRS04], it is prov ed that c 1 ( T reewidth (2)) < ∞ , and later works [LR10, CJL V08] nailed do wn the precise dep endence c 1 ( T reewidth (2)) = 2. Resolving whether c 1 ( T reewidth (3)) is finite seems quite difficult, and is a well-kno wn op en problem. In fact, perhaps the simplest “width 3” problem (whic h w as op en un til the present w ork) in v olves the family P athwidth (3) (recall that P athwidth ( k ) ⊆ T reewidth ( k ) denotes the family of graphs of path width at most k ; see Section 1.3). These families are fundamen tal in the graph minor theory (see e.g. [RS83, Lov06]); see Lemma 1.9 for an inductiv e definition. 4 Our main technical theorem shows that graphs of b ounded path width can b e randomly em- b edded in to trees. In fact, the theorem sho ws something sligh tly stronger, that the target trees themselv es can b e taken to hav e b ounded path width. Theorem 1.5. F or every k ∈ N , Pathwidth ( k ) T rees ∩ P athwidth ( k ) . Quantitatively, P athwidth ( k ) D T rees ∩ P athwidth ( k ) , for some D ≤ (4 k ) k 3 +1 . In particular, this v erifies Conjecture 1 for graphs of b ounded pathwidth. The quan titative b ound of Theorem 1.5 is lik ely far from tight. Naiv ely , one might hop e that for D ≤ O (log k ), one has Pathwidth ( k ) D T rees . But, in fact, known results imply that the distortion must satisfy D ≥ Ω( k ). The k -th lev el diamond graph (see [GNRS04]) has pathwidth O ( k ) but it is shown in [GNRS04] that ev ery sto chastic embedding of this graph in to a distribution o ver trees incurs distortion Ω( k ). Rob ertson and Seymour [RS83] show ed that a minor-closed family F excludes a forest if and only if F ⊆ Pathwidth ( k ) for some k ∈ N . Corollary 1.6. If T is any tr e e, then E { T } T rees . As a consequence of this, together with Lemma 1.3, and the elemen tary fact that c 1 ( T rees ) = 1, w e resolve Conjecture 1 whenever F forbids some tree, yielding Theorem 1.2. W e remark that Theorem 1.2 w as unknown even for F = P athwidth (3). In Section 4, we complement our upp er b ound by pro ving the follo wing theorem. Theorem 1.7. F or every k ∈ N , Pathwidth ( k + 1) ∩ T rees 6 P athwidth ( k ) . This result serv es t w o purp oses. First, it shows that our pro of of Theorem 1.5, which embeds P athwidth ( k ) directly into trees cannot pro ceed by inductively reducing the path w idth by one. Secondly , it is needed in the pro of of Theorem 1.4 in the case when F contains only trees (the tec hniques of [CJL V08] handle the case when F con tains at least one cycle). W e remark that, p erhaps surprisingly , the pro of our non-embeddability result (Theorem 1.7) uses our embedding result (Theorem 1.5). 1.3 Preliminaries W e now review some basic definitions and notions which app ear throughout the pap er. Graphs and metrics. W e deal exclusively with finite graphs G = ( V , E ) which are free of lo ops and parallel edges. W e will also write V ( G ) and E ( G ) for the v ertex and edge sets of G , respectively . A metric gr aph is a graph G equipp ed with a non-negative length function on edges len : E → R + . W e will denote the pseudometric space associated with a graph G as ( V , d G ), where d G is the shortest path metric according to the edge lengths. Note that d G ( x, y ) = 0 ma y o ccur even when x 6 = y , and also if G is disconnected, there will b e pairs x, y ∈ V with d G ( x, y ) = ∞ . W e allow b oth p ossibilities throughout the pap er. An imp ortan t p oin t is that al l length functions in the p ap er ar e assume d to b e r e duc e d, i.e. they satisfy the prop ert y that for every e = ( u, v ) ∈ E , len ( e ) = d G ( u, v ). Giv en a metric graph G , we extend the length function to paths P ⊆ E by setting len ( P ) = P e ∈ P len ( e ). F or a pair of vertices a, b ∈ P , we use the notation P [ a, b ] to denote the sub-path 5 of P from a to b . W e recall that for a subset S ⊆ V , G [ S ] represen ts the induced graph on S . F or a pair of subsets S, T ⊆ V , w e use the notations E ( S, T ) = { ( u, v ) ∈ E : u ∈ S , v ∈ T } and E ( S ) = E ( S, S ). F or a vertex u ∈ V , we write N ( u ) = { v ∈ V : ( u, v ) ∈ E } . Graph minors. If H and G are t w o graphs, one says that H is a minor of G if H can b e obtained from G by a sequence of zero or more of the three op erations: edge deletion, vertex deletion, and edge contraction. G is said to be H -minor-fr e e if H is not a minor of G . W e refer to [Lov06, Die05] for a more extensive discussion of the v ast graph minor theory . Equiv alently , H is a minor of G if there exists a collection of disjoint sets { A v } v ∈ V ( H ) with A v ⊆ V ( G ) for each v ∈ V ( H ), such that each A v is connected in G , and there is an edge b etw een A u and A v whenev er ( u, v ) ∈ E ( H ). A metric space ( X, d ) is said to b e H -minor-fr e e if it is supp orted on some H -minor-free graph. T reewidth. The notion of tr e ewidth in volv es a representation of a graph as a tree, called a tree decomp osition. More precisely , a tr e e de c omp osition of a graph G = ( V , E ) is a pair ( T , χ ) in which T = ( I , F ) is a tree and χ = { χ i | i ∈ I } is a family of subsets of V ( G ) suc h that (1) S i ∈ I χ i = V ; (2) for eac h edge e = { u, v } ∈ E , there exists an i ∈ I such that b oth u and v b elong to χ i ; and (3) for all v ∈ V , the set of no des { i ∈ I | v ∈ χ i } forms a connected subtree of T . T o distinguish b et ween v ertices of the original graph G and v ertices of T in the tree decomp osition, w e call v ertices of T no des and their corresp onding χ i ’s b ags . The maximum size of a bag in χ minus one is called the width of the tree decomp osition. The tr e ewidth of a graph G is the minimum width ov er all p ossible tree decomp ositions of G . P athwidth. A tree decomp osition is called a p ath de c omp osition if T = ( I , F ) is a path. The p athwidth of a graph G is the minimum width o ver all p ossible path decomp ositions of G . W e will use the follo wing alternate characterization. Definition 1.8 (Linear comp osition sequence) . L et k b e a p ositive inte ger. A se quenc e of p airs ( G 0 , V 0 ) , ( G 1 , V 1 ) , . . . , ( G t , V t ) is a linear width- k comp osition sequence for G if G t = G , G 0 is a k - clique with vertex set V 0 , and ( G i +1 , V i +1 ) arises fr om ( G i , V i ) as fol lows: Attach a new vertex v i +1 to al l the vertic es of V i and cho ose V i +1 ⊆ V i ∪ { v i +1 } so that | V i +1 | = k . Observe that it is p ossible to have V i +1 = V i . We further note that for any j ∈ { 1 , . . . , t } , we have V ( G j ) = V 0 ∪ { v 1 , . . . , v j } . The follo wing lemma is straightforw ard to prov e. Lemma 1.9. A gr aph has p athwidth- k if and only if it is a sub gr aph of some gr aph p ossessing a line ar width- k c omp osition se quenc e. Pr o of sketch. A path decomp osition of width k can b e obtained from a width- k comp osition se- quence ( G 0 , V 0 ) , . . . , ( G t , V t ) b y setting for every i ∈ { 1 , . . . , t } , the i -th bag to b e V i − 1 ∪ { v i } . F or the other direction, one can alwa ys assume that a path width- k graph admits a path dep omp osition of width k suc h that ev ery bag has size exactly k + 1, and every tw o bags differ in exactly one v ertex. This immediately yields a linear width- k comp osition sequence. Asymptotic notation. F or tw o expressions E and F , we sometimes use the notation E . F to denote E = O ( F ). W e use E ≈ F to denote the conjunction of E . F and E & F . 6 2 W arm-up: Embedding path width-2 graphs in to trees In this section, we prov e that Pathwidth (2) T rees , as a warm up for the general case in Section 3. The pathwidth-2 case do es not p ossess man y of the difficulties of the general case; in particular, it do es not require us to b ound the stretch in m ultiple phases (for whic h w e in tro duce a rank parameter in the next section). But it does show the importance of using an inflation factor to blo wup small edges, in order for a certain geometric sum to conv erge. Let G = ( V , E ) b e a metric graph of path width 2. By Lemma 1.9, it suffices to giv e a probabilis- tic em b edding for a graph G p ossessing a linear width-2 comp osition sequence ( G 0 , e 0 ) , . . . , ( G t , e t ), where e i pla ys the role of V i in Definition 1.8. W e will inductively em b ed G into a distribution ov er its spanning trees. First, we put T 0 = e 0 . Now, let T i b e a spanning tree of G i , with e i ∈ E ( T i ). W e will pro duce a random spanning tree T i +1 of G i +1 with e i +1 ∈ E ( T i +1 ) as follo ws. Let e i = { u, v } , and let w ∗ b e the newly attac hed v ertex. W e also add the edges { u, w ∗ } , and { v , w ∗ } , so the resulting graph is not a tree. W e obtain a tree by randomly deleting either { u, w ∗ } , or { v , w ∗ } as follo ws. Let τ = 12; we refer to this constant as an “inflation factor.” There are t wo cases. 1. If e i = e i +1 , we delete { u, w ∗ } with probability len ( u,w ∗ ) len ( u,w ∗ )+ len ( v ,w ∗ ) , and otherwise we delete { w ∗ , v } . 2. If e i 6 = e i +1 , assume (without loss of generality) that e i +1 = { v , w ∗ } . In that case, we delete { u, w ∗ } with probability min τ len ( u, w ∗ ) len ( u, w ∗ ) + len ( u, v ) , 1 , (2) and otherwise w e delete { u, v } . It is easy to see that if T i w as a spanning tree, then so is T i +1 . F urthermore, by construction e i +1 ∈ E ( T i +1 ). Let T = T t b e the final tree, and set T i = T for i > t . It remains to b ound the exp ected stretch in T . F or every edge { x, y } ∈ E ( G i ) and i ≥ 0, define the v alue, K x,y i = max E d T ( x, y ) d T i ( x, y ) T i = Γ : P ( T i = Γ) > 0 . This is the maxim um exp ected stretch b et ween x and y incurred o v er all stages later than i , conditioned on the worst p ossible configuration for T i . F or each x ∈ V , define s ( x ) = − 1 for x ∈ V ( G 0 ), and otherwise it is the unique v alue s ≥ 0 suc h that x ∈ V ( G s +1 ) \ V ( G s ). Also define s ( x, y ) = max( s ( x ) , s ( y )). The next tw o lemmas form the core of our analysis. Lemma 2.1. If { x, y } ∈ E and s ( x, y ) = i , then E [ d T ( x, y )] ≤ 3 τ · K x,y i +1 · len ( x, y ) . (3) Pr o of. If x, y ∈ V ( G 0 ), then s ( x, y ) = − 1 and E [ d T ( x, y )] = K x,y 0 · len ( x, y ) by definition. Otherwise, assume without loss of generality that s ( x ) < s ( y ). In this case, it must b e that x ∈ e i = { u, v } and y = w ∗ . Supp ose that x = u . 7 If e i +1 = e i , an elemen tary calculation based on case (1) of our algorithm yields, E d T i +1 ( u, w ∗ ) len ( u, w ∗ ) T i ≤ 3 len ( v , w ∗ ) + len ( u, w ∗ ) len ( v , w ∗ ) + len ( u, w ∗ ) ≤ 3 , from whic h E [ d T ( u, w ∗ )] ≤ 3 K u,w ∗ i +1 · len ( u, w ∗ ) immediately follo ws. Similarly , if e i +1 = { v , w ∗ } , then the exp ected stretc h is inflated by at most a factor of τ , and therefore (3) again follo ws b y a similar calculation. Finally , if e i +1 = { u, w ∗ } , then { u, w ∗ } ∈ E ( T i +1 ), and therefore E [ d T ( u, w ∗ )] ≤ K u,w ∗ i +1 · len ( u, w ∗ ). Lemma 2.2. F or any { x, y } ∈ E ( G i ) , we have K x,y i ≤ max { 3 , K a,b i +1 } for some { a, b } ∈ E ( G i ) . Pr o of. Let Γ b e a tree on V ( G i ) which is a maximizer for K x,y i . Let Γ u and Γ v b e the subtrees of Γ \ e i ro oted at u and v respectively , where we recall that e i = { u, v } . If x and y are b oth either in Γ u , or in Γ v , then K x,y i = 1, since Γ u and Γ v remain intact in the final tree T , conditioned on T i = Γ. So, it suffices to consider the case x ∈ Γ u and y ∈ Γ v . Observe further that since the unique path b etw een x and y in Γ passes through { u, v } , and the x - u and y - v paths will b oth remain in T , we hav e E d T ( x, y ) d T i ( x, y ) T i = Γ ≤ E d T ( u, v ) d T i ( u, v ) T i = Γ ≤ K u,v i . Th us to pro v e the lemma, it suffices to show that K u,v i ≤ max { 3 , K u,v i +1 } . T o this end, let Γ b e the maximizer for K u,v i , and supp ose that T i = Γ. If e i +1 = e i , then the edge { u, v } remains intact (i.e. { u, v } ∈ E ( T i +1 )), and therefore K u,v i ≤ K u,v i +1 . Assume now that e i +1 6 = e i , whic h means that w e are in case (2) of the algorithm. Assume further, without loss of generality , that e i +1 = { v , w ∗ } . Recall that either { u, v } or { u, w ∗ } is deleted. Let A = len ( u, w ∗ ) , B = len ( u, v ) , C = len ( v , w ∗ ). With probability p = min { 1 , τ A A + B } , the edge { u, w ∗ } is deleted, in which case d T ( u, v ) = d T i ( u, v ). With probability 1 − p , the edge { u, v } is deleted, and the new path b etw een u and v in T i +1 is u - w ∗ - v , so the distance b etw een u and v is stretc hed to A + C ≤ 2 A + B , and is eligible to be stretched b y at most a factor K u,v i +1 in the future. Th us, if A ≥ B / ( τ − 1), w e hav e K u,v i = 1. W e can therefore assume A < B / ( τ − 1). Thus we can b ound, K u,v i ≤ τ A A + B + K u,v i +1 1 − τ A A + B 2 A + B B ≤ τ A B + K u,v i +1 1 − τ A 2 B 1 + 2 A B ≤ τ A B + K u,v i +1 1 − τ A 3 B , where w e hav e used 1 − τ A 2 B + 2 A B ≤ 1 − τ A 3 B since τ = 12. But now one sees that, K u,v i ≤ 3 τ A 3 B + K u,v i +1 1 − τ A 3 B ≤ max { 3 , K u,v i +1 } . 8 Figure 1: The graph H i with k = 5. Finally , the next lemma completes our analysis. Lemma 2.3. F or any x, y ∈ V , we have E [ d T ( x, y )] ≤ 9 τ · d G ( x, y ) . Pr o of. By the triangle inequalit y and linearit y of exp ectation, it suffices to pro ve the lemma for edges { x, y } ∈ E . W e will pro ve the follo wing by reverse induction on i : F or every { x, y } ∈ E and i ≥ s ( x, y ) + 1, we hav e K x,y i ≤ 3. Com bining this with Lemma 2.1 will complete the pro of. The claim is trivial for i = t since K x,y t = 1 for all { x, y } ∈ E . If t > i ≥ s ( x, y ) + 1, then { x, y } ∈ E ( G i ), and Lemma 2.2 immediately implies that K x,y i ≤ max { 3 , K a,b i +1 } for some a, b with i + 1 ≥ s ( a, b ) + 1. By induction, K a,b i +1 ≤ 3, hence K x,y i ≤ 3 as w ell. 3 Em b edding path width- k graphs in to trees W e no w turn to graphs of pathwidth k for some k ∈ N . Let G b e suc h a graph. By Lemma 1.9, w e ma y assume that G has a linear width- k comp osition sequence, ( G 0 , V 0 ) , . . . ( G t , V t ). F or i ≥ 1, we define b V i = V i − 1 ∪ { v i } . Our algorithm for embedding G in to a random tree pro ceeds inductively along the comp osition sequence. F or each i ∈ { 1 , . . . , t } we compute a subgraph H i of G i , whose only non-trivial 2-connected comp onent is a ( k + 1)-clique on b V i (see Figure 1). More sp ecifically , H 1 is just a clique on ˆ V 1 . Given H i , w e derive H i +1 b y adding all the edges b etw een v i +1 and V i , and remo ving all the edges, except for one, b etw een V i and the unique vertex in b V i \ V i . The main part of the algorithm inv olv es determining whic h edge in ( b V i \ V i ) × V i w e k eep in H i +1 . The high-level idea b ehind our approach is as follows. On one hand, w e wan t to keep short edges so that the distance b et ween b V i \ V i and V i is small. On the other hand, k eeping alw ays the shortest edge leads to accum ulation of the stretch for certain pairs (whose shortest-path k eeps getting longer, through a sequence of “short” edges). W e a void this obstacle via a randomized pro cess that assigns a r ank to eac h edge, which intuitiv ely means that edges of low er rank are more lik ely to b e deleted. More sp ecifically , at each step i , we pick a random threshold L and keep the highest ranked edge of length at most L , deleting the rest. W e also up date the ranks of the edges in the new graph appropriately . F ormally , let rank i : V ( G ) × V ( G ) → Z ≥ 0 b e an arbitrary symmetric function, with rank 1 ( u, v ) = 0, for eac h u, v ∈ V ( G ). Let E ( b V i ) = b V i 2 , i.e. the set of edges internal to b V i . F or u, v ∈ V ( H i ), let P u,v i b e the unique path b etw een u and v in H i that con tains at most one edge in E ( b V i ). Observe that P u,v i is w ell-defined since b V i forms a clique. F or an edge e ∈ E ( b V i ) w e set edge - rank i ( e ) = max u,v ∈ V ( H i ): e ∈ P u,v i rank i ( u, v ) 9 Figure 2: T ransitioning from H i to H i +1 . Here, w is the unique v ertex in b V i \ V i . The randomized pro cess for generating H i +1 and rank i +1 from H i and rank i is as follows. Let τ = 4 k b e our new “inflation factor.” Let w b e the unique vertex in b V i \ V i , and en umerate E ( w , V i ) = { e 1 , e 2 , . . . , e k } so that len ( e 1 ) ≤ len ( e 2 ) ≤ · · · ≤ len ( e k ). No w, let { σ j } k − 1 j =1 b e a family of indep endent { 0 , 1 } random v ariables with P [ σ j = 1] = min 1 , τ len ( e j ) len ( e j +1 ) , and define the set of eligible edges by E = ( e j : j − 1 Y i =1 σ i = 1 ) . In particular, e 1 ∈ E alwa ys. Let e ∗ ∈ E b e an y edge satisfying edge - rank i ( e ∗ ) = max e ∈E edge - rank i ( e ). Finally , we define H i +1 as the graph with v ertex set V ( G i +1 ) and edge set (see Figure 2), E ( H i +1 ) = { e ∗ } ∪ {{ v i +1 , u } : u ∈ V i } ∪ ( E ( H i ) \ E ( w , V i )) . W e also define rank i +1 as follo ws. F or any u, v ∈ V ( G ) rank i +1 ( u, v ) = ( rank i ( u, v ) if E ( P u,v i ) ∩ E = ∅ rank i ( u, v ) + 1 otherwise . In tuitively , rank i ( u, v ) counts how many times the path b et ween u and v was under risk to b e signific antly stretched until step i . If P u,v i do es not use an edge of E then the edge { u, v } will b e stretc hed, but the alternative path will, on a verage, b e “short enough” that we need not increase its rank (this is ho w the set E is defined). It remains to analyze the exp ected stretch incurred b y the ab o ve pro cess. First, we observe that the maxim um rank of an edge is O ( k 2 ). Lemma 3.1. F or every i = 1 , 2 , . . . , t and every e dge e ∈ E ( b V i ) , edge - rank i ( e ) ≤ k +1 2 . 10 Pr o of. F or each i = 1 , 2 , . . . , t , and each j = 1 , 2 , . . . , k +1 2 , let R i,j b e the j -th largest edge-rank of the edges in E ( b V i ). That is, for eac h i = 1 , 2 , . . . , t , R i, 1 ≤ R i, 2 ≤ . . . ≤ R i, ( k +1 2 ) . W e will pro v e by induction on i that for each i = 1 , 2 , . . . , t , for each 1 ≤ j ≤ k +1 2 , w e hav e R i,j ≤ j . F or i = 1, all the ranks are equal to 0, and the assertion holds trivially . Assume now that the assertion holds for i − 1. It is conv enient to analyze the transition from step i − 1 to step i in three phases. W e need to remov e the edges in E ( w , V i ) \ { e ∗ } and add the edges in E ( v i +1 , V i ), while up dating the ranks accordingly . F or notational simplicity , we assume that the rank of an edge that is remov ed is set to zero. Let e ∗ b e the maximum-rank edge in E . In the first phase, we set the rank of e ∗ to zero, and we increase the rank of all remaining edges in E b y one. Clearly , the resulting edge ranks satisfy the inductive in v arian t. In the second phase, for any edge e ∈ E ( w , V i ) \ { e ∗ } , we update the rank of an edge e 0 = e 0 ( e ) ∈ E ( b V i ) ∩ E ( b V i +1 ) to b e edge - rank ( e 0 ) = max { edge - rank ( e 0 ) , edge - rank ( e ) } , and we set the rank of e to zero. The p oin t here is that for any e ∈ E ( w , V i ), there is a unique edge e 0 ∈ E ( b V i ) ∩ E ( b V i +1 ) suc h that, for an y u, v ∈ V ( H i ), if e ∈ P u,v i then e 0 ∈ P u,v i +1 . In other w ords, the paths that use e will hav e to b e rerouted through a new path that uses e 0 . This explains how the edge-rank of e is “transferred” to e 0 . Clearly , after the second phase the ranks still satisfy the inductiv e inv arian t. Finally , in the third phase w e remov e the edges in E ( w , V i ), and w e add the edges in E ( v i +1 , V i ). All the remov ed edges ha v e at this p oint rank zero, and all new edges also hav e rank zero. Th us, the inductive in v ariant is satisfied. F or any i ∈ { 1 , . . . , t } , r ∈ { 0 , . . . , k +1 2 } , and an y edge { u, v } ∈ E ( G i ), w e put K u,v i ( r ) = max E d H t ( u, v ) d H i ( u, v ) H i = Γ , rank i ( u, v ) = ρ : (Γ , ρ ) ∈ Ω i ( u, v ; r ) , (4) where w e define Ω i ( u, v ; r ) = { (Γ , ρ ) : P ( H i = Γ , rank i ( u, v ) = ρ ) > 0 and ρ ≥ r } . In other w ords, K u,v i ( r ) is the maxim um exp ected stretc h for all stages after i , conditioned on the w orst p ossible configuration ov er subgraphs H i and rank functions satisfying rank i ( u, v ) ≥ r . W e further define K u,v i k +1 2 + 1 = 1. F or the next three lemmas and the corollary that follows, we fix an edge { u, v } ∈ E ( G i ), and a n umber r ∈ { 0 , . . . , k +1 2 } . Let (Γ , ρ ) ∈ Ω i ( u, v ; r ) b e a maximizer in (4), and write P ∗ [ · ] = P [ · | H i = Γ , rank i = ρ ] and E ∗ [ · ] = E [ · | H i = Γ , rank i = ρ ]. A ma jor p oin t is that the following calculations are oblivious to the conditioning, aside from the assumption that rank i ( u, v ) ≥ r . Lemma 3.2. Supp ose that e j ∈ E ( P u,v i ) for some j ∈ { 1 , 2 , . . . , k } . Then, K u,v i ( r ) ≤ P ∗ [ e j ∈ E ] 1 + 2 E ∗ [ len ( e ∗ ) | e j ∈ E ] len ( e j ) K u,v i +1 ( r + 1) + P ∗ [ e j / ∈ E ] 1 + 2 E ∗ [ len ( e ∗ ) | e j / ∈ E ] len ( e j ) K u,v i +1 ( r ) 11 Pr o of. W e ha ve, d H i +1 ( u,v ) d H i ( u,v ) ≤ 2 len ( e ∗ )+ len ( e j ) len ( e j ) . There are t wo p ossibilities: (1) e j ∈ E o ccurs, and the rank of { u, v } is increased by 1, (2) e j / ∈ E and the rank of { u, v } remains the same. This verifies the claimed inequalit y for r < k +1 2 . Note that, by Lemma 3.1, rank i ( u, v ) ≤ k +1 2 . Th us the lemma holds true even for r = k +1 2 , in whic h case e j ∈ E = ⇒ e j = e ∗ (since the rank of the pair u, v cannot increase an ymore). If this hap- p ens, then d H t ( u, v ) = d H i ( u, v ), again verifying the claimed inequality , since K u,v i +1 k +1 2 + 1 = 1 b y definition. Lemma 3.3. F or any j ∈ [ k ] , P ∗ [ e j ∈ E ] 1 + 2 E ∗ [ len ( e ∗ ) | e j ∈E ] len ( e j ) ≤ 3(4 k ) k − 1 len ( e 1 ) len ( e j ) . Pr o of. W e hav e P ∗ [ e j ∈ E ] E ∗ [ len ( e ∗ ) | e j ∈ E ] ≤ E ∗ [ len ( e ∗ )] = k X h =1 len ( e h ) P ∗ [ e ∗ = e h ] ≤ k X h =1 len ( e h ) P ∗ [ e h ∈ E ] ≤ k X h =1 len ( e h ) len ( e 1 ) len ( e h ) τ h − 1 ≤ 2 len ( e 1 ) τ k − 1 . Also, we hav e P ∗ [ e j ∈ E ] ≤ τ j − 1 len ( e 1 ) len ( e j ) ≤ τ k − 1 len ( e 1 ) len ( e j ) . Combining these estimates yields the claim, recalling that τ = 4 k . Lemma 3.4. F or any j ∈ [ k ] , P ∗ [ e j / ∈ E ] 1 + 2 E ∗ [ len ( e ∗ ) | e j / ∈E ] len ( e j ) ≤ 1 − len ( e 1 ) len ( e j ) . Pr o of. Let I = { h ∈ { 1 , 2 , . . . , j − 1 } : len ( e h +1 ) > τ · len ( e h ) } . Observ e that if h ∈ { 1 , 2 , . . . , j − 1 } \ I , then whenever e h ∈ E , we hav e also e h +1 ∈ E . F or each 12 h ∈ I , let k h = | I ∩ { 1 , 2 , . . . , h }| . P ∗ [ e j / ∈ E ] 1 + 2 E ∗ [ len ( e ∗ ) | e j / ∈ E ] len ( e j ) ≤ j − 1 X h =1 P ∗ [ e h ∈ E and e h +1 / ∈ E ] 1 + 2 len ( e h ) len ( e j ) = X h ∈ I P ∗ [ e h ∈ E and e h +1 / ∈ E ] 1 + 2 len ( e h ) len ( e j ) ≤ X h ∈ I τ k h − 1 len ( e 1 ) len ( e h ) 1 − τ len ( e h ) len ( e h +1 ) 1 + 2 len ( e h ) len ( e j ) ≤ X h ∈ I τ k h − 1 len ( e 1 ) len ( e h ) 1 − τ len ( e h ) len ( e h +1 ) + 2 len ( e h ) len ( e j ) = X h ∈ I τ k h − 1 len ( e 1 ) len ( e h ) 1 − τ len ( e h ) len ( e h +1 ) + len ( e 1 ) len ( e j ) X h ∈ I 2 τ k h − 1 ≤ 1 − τ | I | len ( e 1 ) len ( e j ) + len ( e 1 ) len ( e j ) (2 k τ | I |− 1 ) = 1 + len ( e 1 ) len ( e j ) 2 k τ | I |− 1 − τ | I | ≤ 1 − len ( e 1 ) len ( e j ) . Corollary 3.5. F or every { u, v } ∈ E ( G i ) and r ∈ { 0 , . . . , k +1 2 } , we have K u,v i ( r ) ≤ max n 3(4 k ) k − 1 K u,v i +1 ( r + 1) , K u,v i +1 ( r ) o . Pr o of. Supp ose that H i = Γ and rank i = ρ . If E ( P u,v i ) ∩ E ( ˆ V i ) is empt y , then K u,v i ( r ) = 1 b ecause the curren t u - v path in H i will b e preserved in H t . Otherwise, w e hav e E ( P u,v i ) ∩ E ( ˆ V i ) = { e j } for some j ∈ [ k ]. Apply Lemmas 3.2, 3.3, and 3.4 to conclude that K u,v i ( r ) ≤ len ( e 1 ) len ( e j ) 3(4 k ) k − 1 K u,v i +1 ( r + 1) + 1 − len ( e 1 ) len ( e j ) K u,v i +1 ( r ) ≤ max n 3(4 k ) k − 1 K u,v i +1 ( r + 1) , K u,v i +1 ( r ) o , completing the pro of. W e can now state and prov e our main theorem. Theorem 3.6. F or every k ≥ 1 , every metric gr aph of p athwidth k admits a sto chastic D -emb e dding into a distribution over tr e es with D ≤ (4 k ) k 3 . Pr o of. W e may assume that k ≥ 2 as the statement is trivial for k = 1. Let H t b e the random subgraph of G . Fix { u, v } ∈ E ( G ), and supp ose that i 0 is the smallest n umber for whic h u, v ∈ V ( G i 0 ). In this case, since { u, v } is an edge, we hav e d G i 0 ( u, v ) = d G ( u, v ), thus E [ d H t ( u, v )] ≤ K u,v i 0 (0) · len ( u, v ) . 13 No w applying Corollary 3.5 inductively immediately yields the b ound, K u,v i 0 (0) ≤ 3(4 k ) k − 1 ( k +1 2 ) +1 , recalling that K u,v i k +1 2 + 1 = 1 for all i , and K u,v t ( r ) = 1 for all r . Finally , observe that the only non-trivial 2-connected comp onent of H t is a ( k + 1)-clique on b V t . Replacing b V t b y a minim um spanning tree yields a tree T with d T ( u, v ) ≤ ( k + 1) · d H t ( u, v ). This completes the pro of. 4 P athwidth ( k + 1) 6 Pathwidth ( k ) W e no w sho w that for any fixed k ≥ 1, and for any n ≥ 1, there exists an n -vertex graph of path width k + 1 for which an y sto c hastic D -embedding into graphs of pathwidth k has D ≥ Ω( n 2 − k ), where the Ω( · ) notation hides a m ultiplicativ e constant dep ending on k . In fact, our low er b ound holds ev en for trees of pathwidth k + 1. W e b egin by giving t wo structural lemmas that allo w us to decomp ose a tree of pathwidth ` into a path and a collection of trees of pathwidth at most ` − 1. Lemma 4.1. L et G 1 , G 2 , G 3 b e c onne cte d gr aphs of p athwidth k with disjoint vertex sets, and for i ∈ [3] , let v i ∈ V ( G i ) . L et G b e the gr aph obtaine d by intr o ducing a new vertex v ∗ , and c onne cting it to v 1 , v 2 , and v 3 . F ormal ly, V ( G ) = { v ∗ } ∪ S 3 i =1 V ( G i ) , and E ( G ) = S 3 i =1 E ( G i ) ∪ {{ v ∗ , v i }} . Then G has p athwidth k + 1 . Pr o of. It is easy to see that G has path width at most k + 1: F or each i ∈ [3] tak e a path decom- p osition of G i with bags C i, 1 , . . . , C i,` i . F or each i ∈ [3], j ∈ [ ` i ], let C 0 i,j = C i,j ∪ { v ∗ } . The bags C 0 1 , 1 , . . . , C 0 1 ,` 1 , C 0 2 , 1 , . . . , C 0 2 ,` 2 , C 0 3 , 1 , . . . , C 0 3 ,` 3 induce a path decomp osition of G with width at most k + 1. Assume no w for the sake of contradiction that the pathwidth of G is at most k . That is, there exists a path decomp osition of G with bags C 1 , . . . , C ` , such that: (i) for each i ∈ [ ` ], | C i | ≤ k + 1, (ii) for eac h { u, v } ∈ E ( G ) there exists i ∈ [ ` ] with u, v ∈ C i , and (iii) for each v ∈ V ( G ) there exists a subin terv al I ⊆ [ ` ] such that v ∈ C i iff i ∈ I . F or each i ∈ [3], let G 0 i b e the subgraph of G induced b y V ( G i ) ∪ { v ∗} . Let also A i = { j ∈ [ ` ] : C j ∩ V ( G 0 i ) 6 = ∅} . Note that since G 0 i is connected, it follows that A i is a subin terv al of [ ` ]. Pick i 1 , i 2 ∈ [3], such that 1 ∈ A i 1 , and ` ∈ A i 2 . Note that we might hav e i 1 = i 2 . Since V ( G 0 i 1 ) ∩ V ( G 0 i 2 ) 6 = ∅ , we hav e that A i 1 ∩ A i 2 6 = ∅ . In particular, A i 1 ∪ A i 2 = [ ` ]. Therefore, eac h bag C i con tains at least one v ertex either from G 0 i 1 , or G 0 i 2 . Let i 3 b e an element in [3] \ { i 1 , i 2 } . Remo ving V ( G 0 i 1 ) ∪ V ( G 0 i 2 ) from all the bags C i , we get a decomp osition of G \ ( G 0 i 1 ∪ G 0 i 2 ) = G i 3 with width at most k − 1, a con tradiction since G i 3 has path width k . The follo wing lemma is straightforw ard. Lemma 4.2. If H is a minor of G , then the p athwidth of H is at most the p athwidth of G . Lemma 4.3. L et T b e a tr e e of p athwidth ` ≥ 2 . Then, ther e exists a simple p ath P in T such that deleting the vertic es of P fr om T le aves a for est with e ach tr e e having p athwidth at most ` − 1 . 14 Pr o of. F or ev ery v ∈ V ( T ), let α ( v ) denote the num b er of connected comp onen ts of T \ { v } of path width ` . W e first argue that for any v ∈ V ( T ), w e ha ve α ( v ) ≤ 2. T o see that, assume for the sak e of con tradiction that there exists v ∈ V ( T ), suc h that T \ { v } contains connected comp onents C 1 , C 2 , C 3 , eac h of path width at least ` . Then, by Lemma 4.1 it follo ws that T must ha ve path width ` + 1, a contradiction. First, observe that if there exists v ∈ V ( T ) with α ( v ) = 0, then the path contaning only v satisfies the assertion. Next, w e consider the case where for every v ∈ V ( T ), α ( v ) = 1. W e construct a path Q = x 1 , . . . , x s as follows. W e set x 1 to b e an arbitrary leaf of T . Given x i , let y i b e the unique neighbor of x i in T , such that y i is contained in the unique connected comp onent of T \ { x i } of pathwidth ` . If there exists j < i , suc h that x j = y i , then we terminate the path Q at x i , and we set s = i . Otherwise, we set x i +1 = y i , and contin ue at x i +1 . W e now argue that Q satisfies the assertion. F or the sake of contradiction supp ose that T \ V ( Q ) con tains a connected comp onen t C of pathwidth ` . The comp onen t C must b e attached to Q via some edge { y , x r } , with y ∈ V ( C ). This implies how ever that y is chosen as y r when examining x r , and therefore y m ust b e in Q , a contradiction. Finally , it remains to consider the case where there exists at least one v ∈ V ( T ), with α ( v ) = 2. Let X = { v ∈ V ( T ) : α ( v ) = 2 } . Let H = T [ X ] b e the subgraph of T induced on X . W e first argue that H is connected. T o see this, let x, y ∈ X , and let L b e the unique path b et ween x and y in T . Since α ( x ) = α ( y ) = 2, it follows that there exist connected comp onen ts C x , C y of T \ V ( L ) with C x attac hed to x , and C y attac hed to y , such that b oth C x and C y ha ve pathwidth ` . Let z ∈ V ( L ). It follows that there exist comp onents C 0 x , C 0 y of T \ { z } , suc h that C x ⊆ C 0 x , and C y ⊆ C 0 y , which implies that α ( z ) = 2. Th us, z ∈ X . This implies that L ⊆ H , and therefore H must be connected. W e next sho w that H is a path. T o see this supp ose for the sak e of con tradiction that there exists v ∈ V ( H ) with distinct neigh b ors v 1 , v 2 , v 3 ∈ V ( H ). Since α ( v 1 ) = α ( v 2 ) = α ( v 3 ) = 2, it follo ws that there exist comp onen ts C 1 , C 2 , C 3 of T \ { v , v 1 , v 2 , v 3 } , with each C i adjacen t to v i , and such that each C i has pathwidth ` , for all i ∈ { 1 , 2 , 3 } . By Lemma 4.2 we ha v e that for any i ∈ { 1 , 2 , 3 } , the connected comp onent of T \ { v } containing v i has pathwidth at least ` . Applying Lemma 4.1, we obtain that T has pathwidth at least ` + 1, a con tradiction. Therefore, H is a path. Let w 1 , w 2 b e the tw o endp oints of the path H . W e remark that w e migh t hav e w 1 = w 2 , if there is only one vertex in H . Since α ( w 1 ) = 2, it follo ws that there exists a connected comp onent of C w 1 of T \ V ( H ) of path width ` whic h is attac hed to w 1 . Similarly , there exists a connected comp onen t C w 2 of T \ V ( H ) of pathwidth ` which is attached to w 2 . Note that ev en if w 1 = w 2 , since α ( w 1 ) = 2, the comp onents C w 1 , C w 2 can b e c hosen to b e distinct. Let w 0 1 , w 0 2 b e the neigh b ors of w 1 , and w 2 in C w 1 , and C w 2 resp ectiv ely . Let H 0 b e the path obtained b y adding w 0 1 , and w 0 2 to H . W e will show that Q = H 0 satisfies the assertion of the lemma. T o that end, it remains to sho w that any connected comp onent of T \ V ( H 0 ) has path width at most ` − 1. Let C b e a comp onen t of T \ V ( H 0 ), and supp ose for the sake of con tradiction that it has path width ` . Supp ose first that C is attached to a vertex v ∈ V ( H ). Since v ∈ V ( H ), it follo ws that α ( v ) = 2. By applying Lemma 4.1 on the clusters C , C w 1 , and C w 2 , w e obtain that T contains a minor of path width at least ` + 1, whic h combined with Lemma 4.2 leads to a contradiction. Finally , suppose that C is attached to a v ertex w ∈ { w 0 1 , w 0 2 } , and assume, without loss of generalit y , that w = w 0 1 . Then it follows that T \ { w } contains at least tw o components of path width ` (one con taining C , and another containing C w 2 ), and thus α ( w ) = 2, a contradiction since w / ∈ X . This concludes the pro of. 15 Figure 3: The tree Ψ 3 ,m . W e now state the main result of this Section. Theorem 4.4. F or any k ≥ 1 , and for any n ≥ 1 , ther e exists an n -vertex tr e e G of p athwidth k + 1 , such that any sto chastic D -emb e dding of G into metric gr aphs of p athwidth k , has D ≥ Ω( n 2 − k ) . In p articular, Pathwidth ( k + 1) ∩ T rees 6 Pathwidth ( k ) . The remainder of this Section is devoted to proving Theorem 4.4. W e first construct a graph that will b e used for the low er b ound. F or each i ≥ 1, let Φ i b e the unit-weigh ted graph consisting of a vertex v connected to i disjoint paths of length i . Observ e that Φ i is a tree with i leav es. W e consider Φ i as b eing ro oted at the vertex v . F or each i ≥ 1, and for eac h m ≥ 1, we define the graph Ψ i,m as follows. F or i = 1, we set Ψ 1 ,m = Φ d √ m e . F or i ≥ 2, let Ψ i,m b e the graph obtained by iden tifying the ro ot of a copy of Ψ i − 1 , √ m , with eac h leaf of Φ d √ m e . F or ` ≤ d √ m e , let Ψ i,m,` b e the tree obtained from Ψ i,m b y deleting d √ m e − d ` e children of the ro ot of Ψ i,m , along with ev erything underneath those c hildren. In particular, Ψ i,m, √ m = Ψ i,m . Lemma 4.5. F or e ach i ≥ 1 and m ≥ 3 2 i , Ψ i,m has p athwidth i + 1 . Pr o of. Note that for m ≥ 3 2 i , Ψ i,m con tains, as a minor, a full ternary tree T of depth i . Using Lemma 4.1 inductively shows that the path width of the depth i ternary tree is i + 1, hence Lemma 4.2 implies that the path width of Ψ i,m is at least i + 1. It is also easy to chec k by hand that the path width of Ψ i,m is at most i + 1, for ev ery m ≥ 1. Fix k ≥ 1, and let G = Ψ k,m . By Lemma 4.5, for m ≥ 3 2 k , G has path width k + 1. W e will sho w that for m large enough, any sto c hastic c -em b edding of ( V ( G ) , d G ) into a distribution ov er metric graphs of pathwidth k , has distortion c ≥ Ω( n 2 − k ), w ere n = | V ( G ) | . Assume there exists a sto chastic c -embedding of ( V ( G ) , d G ) into a distribution o ver metric graphs of pathwidth k . By comp osing this with the result of Theorem 3.6, we get a sto chastic c 0 -em b edding of ( V ( G ) , d G ) into the family of metrics supp orted on Pathwidth ( k ) ∩ T rees , with c 0 = O ( c ) (where the O ( · ) notation hides a constant dep ending on the fixed parameter k ). 16 By av eraging, there exists a metric tree T of path width k and a single non-con tractiv e mapping f : V ( G ) → V ( T ) which satisfies, 1 | E ( G ) | X { u,v }∈ E ( G ) d T ( f ( u ) , f ( v )) ≤ c 0 . Th us it suffices to prov e a low er b ound on this quan tity . In fact w e will prov e a somewhat stronger statemen t; w e will giv e a low er b ound on the av erage stretc h of an y non-con tractiv e em b edding of Ψ k,m, √ m/ 2 . W e first prov e an auxiliary lemma. Lemma 4.6. L et S b e an unweighte d tr e e with r ∈ V ( S ) , and let L ≥ 0 . L et ` ≥ 0 , and let S 1 , . . . , S ` b e vertex-disjoint subtr e es of S such that for e ach i ∈ [ ` ] , S i is attache d to r via a p ath Q i of length at le ast L , and for e ach i 6 = j ∈ [ ` ] , the p aths Q i and Q j interse ct only at r . We r emark that e ach S i might c ontain only a single vertex. L et g : V ( S ) → V ( T ) b e a non-c ontr active emb e dding of S into a metric tr e e T , and let P b e a simple p ath in T . If I = { i ∈ [ ` ] : d T ( g ( S i ) , P ) < L/ 2 } , then X { u,v }∈ E ( S ) d T ( g ( u ) , g ( v )) ≥ | I | 2 L 16 . Pr o of. F or each i ∈ I , let z i = argmin v ∈ P d T ( v , g ( S i )), and B i = { x ∈ V ( P ) : d T ( z i , x ) ≤ L/ 2 } . Since g is non-con tractive, we hav e that for eac h i, j ∈ I with i 6 = j , d T ( g ( S i ) , g ( S j )) ≥ 2 L , and therefore d T ( z i , z j ) ≥ d T ( g ( S i ) , g ( S j )) − d T ( g ( S i ) , z i ) − d T ( g ( S j ) , z j ) = 2 L − d T ( S i , P ) − d T ( S j , P ) > L, whic h implies B i ∩ B j = ∅ . By reordering, we assume that I = { 1 , 2 , . . . , | I |} , and that for each i, j ∈ I with i < j , B i app ears to the left of B j in P , after fixing some orientation of P . F urthermore, b y choosing the prop er orientation, we may assume that there is a vertex u 0 ∈ P suc h that u 0 is contained in, or app ears to the left of B d| I | / 2 e in P , and g ( r ) and u 0 are in the same subtree of T \ E ( P ). F or each i ∈ { 1 , . . . , | I |} , let w i = argmin v ∈ V ( S i ) d S ( v , r ). It follows that for each i ∈ {d| I | / 2 e + 1 , . . . , | I |} , d T ( g ( r ) , g ( w i )) ≥ ( i − d| I | / 2 e ) L. F urthermore, for every i ∈ [ ` ], clearly d T ( g ( r ) , g ( w i )) ≥ L b y non-contractiv eness. Therefore, X { u,v }∈ E ( S ) d T ( g ( u ) , g ( v )) ≥ X i ∈{d 1 ,..., | I |} X { u,v }∈ E ( Q i ) d T ( g ( u ) , g ( v )) ≥ X i ∈{d 1 ,..., | I |} d T ( g ( r ) , g ( w i )) ≥ | I | 2 L + X i ∈{d| I | / 2 e +1 ,..., | I |} i − | I | 2 L > | I | 2 L 16 . 17 The pro of of the low er b ound pro ceeds by induction on k . W e first pro ve the base case for em b edding into trees of pathwidth one. Lemma 4.7. L et g : V (Ψ 1 ,m, √ m/ 2 ) → V ( T ) b e a non-c ontr acting emb e dding into a metric tr e e T of p athwidth one. Then, 1 | E (Ψ 1 ,m, √ m/ 2 ) | X { u,v }∈ E (Ψ 1 ,m, √ m/ 2 ) d T ( g ( u ) , g ( v )) ≥ √ m 2 10 . Pr o of. Since the tree T has path width one, it consists of a path P = { v 1 , . . . , v t } , and a collection of v ertex-disjoint stars T 1 , . . . , T t , with eac h T i b eing ro oted at v i . Note that T i migh t contain only the v ertex v i . Recall that Ψ 1 ,m, √ m/ 2 consists of b √ m/ 2 c disjoin t paths Q 1 , . . . , Q b √ m/ 2 c , with Q i = { r , q i, 1 , . . . , q i, d √ m e } , where r is the ro ot of Ψ 1 ,m, √ m/ 2 . F or eac h i ∈ [ b √ m/ 2 c ] let Q 0 i b e the subpath of Q i of length b √ m/ 2 c with Q 0 i = n q i, d √ m/ 2 e , . . . , q i, d √ m e o . Let I 1 = { i ∈ [ b √ m/ 2 c ] : d T ( g ( Q 0 i ) , P ) ≥ √ m/ 4 } , and let I 2 = [ b √ m/ 2 c ] \ I 1 . By Lemma 4.6, X { u,v }∈ E (Ψ 1 ,m, √ m/ 2 ) d T ( g ( u ) , g ( v )) ≥ | I 2 | 2 √ m 32 . Since | E (Ψ 1 ,m ) | ≤ 2 m , w e are done if | I 2 | ≥ √ m/ 4. It remains to consider the case | I 1 | ≥ b √ m/ 4 c . Observe that for each i ∈ I 1 , all the edges of Q 0 i ha ve their endp oints mapp ed to distinct leav es of the stars T 1 , . . . , T t , with the edge adjacent to eac h such leaf having length at least √ m/ 4, by non-con tractiveness of g . Therefore, each edge of suc h a Q 0 i is stretc hed by a factor of √ m/ 2 in T . In other words, 1 | E (Ψ 1 ,m, √ m/ 2 ) | X { u,v }∈ E (Ψ 1 ,m, √ m/ 2 ) d T ( g ( u ) , g ( v )) ≥ 1 2 m · | I 1 | · √ m 2 √ m 2 = √ m 4 √ m 4 √ m 2 ≥ √ m 32 , with the latter b ound holding for m ≥ 4. Observe that the LHS is alwa ys at least 1, yielding the desired result for m ≤ 4 as well, and completing the pro of. W e are now ready to prov e the main inductiv e step. Lemma 4.8. L et k ≥ 1 , a ∈ N , m = (2 a ) 2 k , and let g : V (Ψ k,m, √ m/ 2 ) → V ( T ) b e a non-c ontr active emb e dding of Ψ k,m, √ m/ 2 into a metric tr e e T of p athwidth k . Then, 1 | E (Ψ k,m, √ m/ 2 ) | X { u,v }∈ E (Ψ k,m, √ m/ 2 ) d T ( g ( u ) , g ( v )) ≥ m 2 − k 2 7+3 k . 18 Pr o of. W e pro ceed by induction on k . The base case k = 1 is given b y Lemma 4.7, so we can assume that k ≥ 2, and that the assertion is true for k − 1. Since the tree T has pathwidth k ≥ 2, by Lemma 4.3 it follows that it consists of a path P , and a collection of trees T 1 , . . . , T t of pathwidth at most k − 1, with each T i b eing ro oted at some v ertex v i , and v i b eing attached to P via an edge. Recall that Ψ k,m, √ m/ 2 consists of a ro ot r and √ m/ 2 subtrees Q 1 , . . . , Q √ m/ 2 , with eac h Q i ha ving a copy Q 0 i of Ψ k − 1 , √ m that is connected to r via a path of length √ m . Let I 1 = { i ∈ [ √ m/ 2] : d T ( g ( Q 0 i ) , P ) ≥ √ m/ 2 } , and let I 2 = [ √ m/ 2] \ I 1 . By Lemma 4.6, X { u,v }∈ E (Ψ k,m, √ m/ 2 ) d T ( g ( u ) , g ( v )) ≥ | I 2 | 2 √ m 16 . Since | E (Ψ k,m ) | ≤ k m , this yields the desired result for | I 2 | ≥ √ m/ 4. It remains to consider the case | I 1 | ≥ √ m/ 4. Let I 1 , 1 b e the subset of I 1 con taining all indices i ∈ I 1 suc h that for some j ∈ [ t ], T j con tains the image of a copy of Ψ k − 1 ,m 1 / 2 ,m 1 / 4 / 2 from Q 0 i . Let also I 1 , 2 = I 1 \ I 1 , 1 . By the induction hypothesis it follows that for any i ∈ I 1 , 1 , X { u,v }∈ E ( Q 0 i ) d T ( g ( u ) , g ( v )) ≥ m 1 / 2 · ( k − 1) · ( m 1 / 2 ) 2 1 − k 2 7+3( k − 1) = m 1 / 2 · ( k − 1) · m 2 − k 2 4+3 k . (5) Consider now i ∈ I 1 , 2 . Let r i b e the ro ot of Q 0 i and let W i, 1 , . . . , W i,m 1 / 4 b e the copies of Ψ k − 1 ,m 1 / 2 , 1 in Q 0 i , intersecting only at r i . By the definition of I 1 , 2 w e ha ve that for an y J ⊂ [ m 1 / 4 ] with | J | = m 1 / 4 / 2, and for any i 0 ∈ [ t ], S j ∈ J g ( W i,j ) * T i 0 . Assume that the image of r i is con tained in T τ , for some τ ∈ [ t ]. It follo ws that there exists R ⊆ [ m 1 / 4 ], with | R | ≥ m 1 / 4 / 2, suc h that for each j ∈ R , the image of W i,j in tersects some tree T σ j , with σ j 6 = τ . Since r i ∈ V ( W i,j ) it follows that there exists an edge e i,j ∈ E ( W i,j ) ∪ E ( Z i,j ) that is stretched by a factor of at least m 1 / 2 . It follo ws that for an y i ∈ I 1 , 2 , X { u,v }∈ E ( Q 0 i ) d T ( g ( u ) , g ( v )) ≥ m 1 / 4 2 · m 1 / 2 . (6) By (5) w e get a lo wer b ound for the a verage stretc h of the edges of ev ery Q 0 i , with i ∈ I 1 , 1 . Similarly , b y (6) w e get a low er b ound for the av erage stretch of the edges of every Q 0 i , with i ∈ I 1 , 2 . Th us, com bining (5) and (6) we get 1 | E (Ψ k,m, √ m/ 2 ) | X { u,v }∈ E (Ψ k,m, √ m/ 2 ) d T ( g ( u ) , g ( v )) ≥ 1 k · m · | I 1 | · m 1 / 2 · ( k − 1) · m 2 − k 2 4+3 k > m 2 − k 2 7+3 k , as desired. This concludes the pro of of Theorem 4.4. 19 Ac knowledgemen ts W e thank Andrea F ranck e and Alexander Jaffe for a careful reading of our argumen ts, and numerous v aluable suggestions. W e are also grateful to the anon ymous referees for man y insigh tful commen ts. References [AR98] Y onatan Aumann and Y uv al Rabani. An O (log k ) appro ximate min-cut max-flow theo- rem and approximation algorithm. SIAM J. Comput. , 27(1):291–301 (electronic), 1998. [Bar96] Y air Bartal. Probabilistic appro ximations of metric space and its algorithmic applica- tion. In 37th Annual Symp osium on F oundations of Computer Scienc e , pages 183–193, Octob er 1996. [Bar98] Y air Bartal. On approximating arbitrary metrics by tree metrics. In Pr o c e e dings of the 30th A nnual A CM Symp osium on The ory of Computing , pages 183–193, 1998. [CG04] D. Carroll and A. Go el. Lo w er b ounds for embedding into distributions ov er excluded minor graph families. In Pr o c e e dings of the 12th Eur op e an Symp osium on A lgorithms , 2004. [CGN + 06] Chandra Chekuri, Anupam Gupta, Ilan Newman, Y uri Rabino vich, and Alistair Sin- clair. Em b edding k -outerplanar graphs into l 1 . SIAM J. Discr ete Math. , 20(1):119–136 (electronic), 2006. [CJL V08] Amit Chakrabarti, Alexander Jaffe, James R. Lee, and Justin Vincen t. Embeddings of top ological graphs: Lossy inv ariants, linearization, and 2-sums. In IEEE Symp osium on F oundations of Computer Scienc e , 2008. [CKR10] Eden Chlam tac, Robert Krauthgamer, and Prasad Ragha vendra. Approximating spars- est cut in graphs of b ounded treewidth. In APPRO X-RANDOM , pages 124–137, 2010. [CSW10] Chandra Chekuri, F. Bruce Shepherd, and Christophe W eib el. Flow-cut gaps for integer and fractional m ultiflows. In Pr o c e e dings of the 21st Annual A CM-SIAM Symp osium on Discr ete Algorithms , pages 1198–1208, 2010. [Die05] Reinhard Diestel. Gr aph the ory , volume 173 of Gr aduate T exts in Mathematics . Springer-V erlag, Berlin, third edition, 2005. [FF56] L. R. F ord and D. R. F ulk erson. Maximal flo w through a netw ork. Canadian Journal of Mathematics , 8:399–404, 1956. [FR T04] Jittat F akc haro enphol, Satish Rao, and Kunal T alwar. A tight b ound on appro ximating arbitrary metrics b y tree metrics. J. Comput. Syst. Sci. , 69(3):485–497, 2004. [GNRS04] Anupam Gupta, Ilan Newman, Y uri Rabinovic h, and Alistair Sinclair. Cuts, trees and l 1 -em b eddings of graphs. Combinatoric a , 24(2):233–269, 2004. [IS07] Piotr Indyk and Anastasios Sidirop oulos. Probabilistic embeddings of b ounded genus graphs in to planar graphs. In Pr o c e e dings of the 23r d Annual Symp osium on Computa- tional Ge ometry . ACM, 2007. 20 [Kar89] R. M. Karp. A 2 k -comp etitive algorithm for the circle. Manuscript, 1989. [LLR95] N. Linial, E. London, and Y. Rabino vich. The geometry of graphs and some of its algorithmic applications. Combinatoric a , 15(2):215–245, 1995. [Lo v06] L´ aszl´ o Lo v´ asz. Graph minor theory . Bul l. Amer. Math. So c. (N.S.) , 43(1):75–86 (elec- tronic), 2006. [LR99] T om Leighton and Satish Rao. Multicommodity max-flo w min-cut theorems and their use in designing approximation algorithms. J. ACM , 46(6):787–832, 1999. [LR10] James R. Lee and Prasad Ragha vendra. Coarse differen tiation and m ulti-flo ws in planar graphs. Discr ete Comput. Ge om. , 43(2):346–362, 2010. [LS09] J. R. Lee and A. Sidirop oulos. On the geometry of graphs with a forbidden minor. In 41st A nnual Symp osium on the The ory of Computing , 2009. [OS81] Haruk o Ok am ura and P . D. Seymour. Multicommo dit y flows in planar graphs. J. Combin. The ory Ser. B , 31(1):75–81, 1981. [RR98] Y. Rabinovic h and R. Raz. Low er b ounds on the distortion of embedding finite metric spaces in graphs. Discr ete Comput. Ge om. , 19(1):79–94, 1998. [RS83] Neil Rob ertson and P . D. Seymour. Graph minors. I. Excluding a forest. J. Combin. The ory Ser. B , 35(1):39–61, 1983. 21

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment