Dynamic Modeling and Statistical Analysis of Event Times

This review article provides an overview of recent work in the modeling and analysis of recurrent events arising in engineering, reliability, public health, biomedicine and other areas. Recurrent event modeling possesses unique facets making it diffe…

Authors: ** Edsel A. Peña (University of South Carolina, Department of Statistics) **

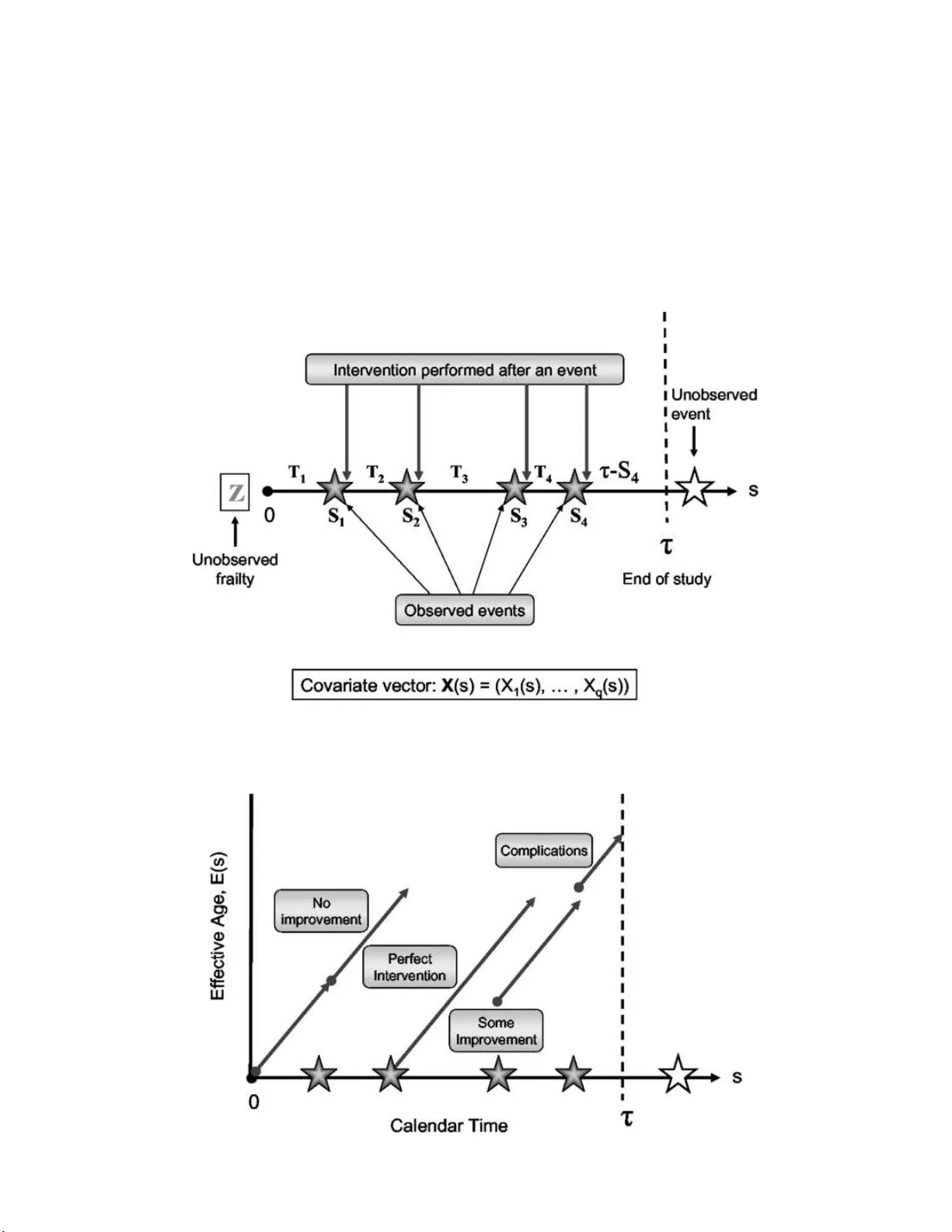

Statistic al Scienc e 2006, V ol. 21 , N o. 4, 487– 500 DOI: 10.1214 /0883423 06000000349 c Institute of Mathematical Statistics , 2006 Dynamic Mo deling and Statistical Analysis of Event Times Edsel A. P e˜ na Abstr act. This review article provi des an o ve rview of recen t work in the mo deling and analysis of recurrent ev en ts arising in engineering, reliabilit y , public healt h, b iomedicine and o ther areas. Recurren t ev en t mo deling p o ssesses unique facets m aking it differen t and m ore diffi- cult to handle than sin gle ev ent settings. F or instance, the imp act of an increasing n umber of ev en t o ccurrences needs to b e tak en in to ac- coun t, the effects of co v ariate s sh ould b e considered, p otent ial asso- ciatio n among the in terev en t times within a u nit cannot b e ignored, and the effects of p erformed in terv en tions after eac h even t o ccurrence need to b e factored in. A recen t general class of mo d els for recurr en t ev en ts wh ic h simult aneously a ccommo dates these aspects is describ ed. Statistica l inference metho ds for this cl ass of m o dels are presen ted and illustrated through applications to r eal data s ets. Some existing op en researc h problems are described . Key wor ds and phr as es: Coun ting p ro cess, hazard function, martin- gale, p artial lik elihoo d, generalized Nelson–Aale n estimator, general- ized p ro duct-limit estimator. 1. INTRODUCTION A decade ago in a Statistic al Scienc e article, Singpurwalla ( 1995 ) adv ocated the deve lopment, adoption and exploration of dynamic mo dels in the theory and practice of rel iabilit y . He also pinp oin ted that the u se of sto c hastic pr o cesses in the mo del- ing of comp onen t and system failure times offers a ric h envi ronment to meaningfully capture dynamic op erating conditions. In this article, we review r e- cen t researc h d ev elopmen ts in d ynamic fai lure-time mo dels, in the con text of b oth stochasti c mo del- ing and i nference concerning mo del parameters. Dy- namic mo dels are not limited in app licabilit y and relev ance to the engineering and relia bilit y areas. Edsel A. Pe˜ na is Pr ofessor, Dep artment of Statistics, University of South Car oli na, Columbia, South Car olina 29208 , USA e-mail: p ena@stat.sc.e du . This is an electronic reprint o f the original article published b y the Institute of Mathematical Statistics in Statistic al Scienc e , 200 6, V ol. 21, No. 4, 487 –500 . This reprint differs from the orig inal in pagination and t yp ogr aphic detail. They are also relev an t in other fields such as pu blic health, biomedicine, economics, so ciology and p oli- tics. This is b ec ause in man y studies in these v ar- ied a reas, it is often times of int erest to monitor the o ccurrences of an ev en t. Suc h an ev en t could b e the malfunctioning of a mec hanical or electronic system, encoun tering a b ug in computer soft wa re, the out- break of a disease, o ccurren ce of a migraine, reo c- currence of a tumor, a d rop of 200 p oin ts in the Do w Jones Ind ustrial Av erage du ring a trading d a y , com- mission of a criminal ac t in a cit y , serious disagree- men ts b et ween a married couple, or the replacemen t of a cabinet min ister/secreta ry in an administration. These ev en ts recur and s o it is of inte rest to de- scrib e their recurrence b eha vior through a sto c hastic mo del. I f suc h a mo del has excellen t predictiv e abil- it y for ev en t occurrences, then if ev ent o ccurrences lead to drastic and/or negativ e consequences, pre- v en tiv e inte rven tions may b e attempted to minimize damages, whereas if they lead to b eneficial and/or p ositiv e outcomes, certain actions may b e p erform ed to hasten ev en t occurrences. It is b ecause of p erformed in terv en tions after ev en t o ccurrences that dynamic mo dels b e come especially 1 2 E. A. PE ˜ NA p ertinent , sin ce through su c h inte rven tions, or some- times nonin terve nti ons, the sto chastic structure go v- erning future ev en t o ccurr ences is altered. This c hange in the mec hanism go v erning the even t o ccurr ences could also b e due to the induced c hange in the struc- ture f unction in a reliabilit y setting go v erning the system of in terest arising from an ev en t o ccurrence (cf. Hollander and P e ˜ na, 1995 ; Kv am and P e ˜ na, 2005 ; P e ˜ na and Slate, 2005 ). F urthermore, since sev eral ev en ts may occur within a un it, it is also imp ortan t to consider the asso ciation among the in terev en t times whic h ma y arise b ecause of unobserv ed ran- dom effects or frailties for the u nit. In addition, there is a need to tak e in to accoun t the p oten tial impact of environmen tal and other relev ant co v ari- ates, p o ssibly includ in g the accumulat ed n umber of ev en t o ccurrences, which could affect future even t o ccurrences. In this review article w e describ e a flexible and general class of dynamic sto c hastic mo dels for even t o ccurrences. This class of mod els wa s prop osed by P e ˜ na and Hollander ( 2004 ). W e also discuss infer- ence metho d s for this class of mo d els as deve lop ed in P e˜ n a, Str awderman and Hollander ( 2001 ), Pe˜ na, Slate and Gonz´ alez ( 2007 ) and Kv am and P e˜ na ( 2005 ). W e demonstrate their app licatio ns to real data s ets and ind icate some open researc h p roblems. 2. BA CK GROUND AND NOT A TION Rapid and general progress in eve nt time mo d- eling and inference has b enefited immensely from the adoption of the framewo rk of count ing pro cesses, martingales and sto c hastic integ ration as in tro du ced in Aalen’s ( 1978 ) pioneering work. The presen t re- view article adopts this mathematica l framewo rk. Excellen t references for this framewo rk are the mono- graph of Gill ( 1980 ), and the b o oks b y Fleming and Harrington ( 1991 ) and Andersen , Borgan, Gill and Keiding ( 1993 ). W e introd uce in this section some notation and v ery minimal bac kground in order to help the reader in the sequel, b u t advise the reader to consult the aforement ioned references to gain an in-depth knowle dge of this framew ork. W e denote b y (Ω , F , P ) the basic probabilit y space on wh ich all rand om en tities are defined . Since in - terest will b e on times b et we en ev ent o ccurrences or on the times of eve nt o ccurr ences, nonn egativ e- v al ued random v aria bles will b e of concern. F or a random v ariable T with range ℜ + = [0 , ∞ ), F ( t ) = F T ( t ) = P { T ≤ t } and S ( t ) = S T ( t ) = 1 − F ( t ) = P { T > t } will d enote its distribution and survivo r (also calle d reliabilit y) f u nctions, r esp ectiv ely . The indicator fun ction of the even t A will b e denoted b y I { A } . The cumula tiv e hazard function of T is defined according to Λ( t ) = Λ T ( t ) = I { t ≥ 0 } Z t 0 F ( d w ) S ( w − ) with the co nv en tion that S ( w − ) = lim t ↑ w S ( t ) = P { T ≥ w } and R b a · · · = R ( a,b ] · · · . F or a nondecreasing function G : ℜ + → ℜ + with G (0) = 0, its pro d uct- in tegral o v er (0 , t ] is defined via (cf. Gill and Jo- hansen, 1990 ; Andersen et al., 1993 ) Q t w =0 [1 − G ( dw )] = lim M →∞ Q M i =1 [1 − ( G ( t i ) − G ( t i − 1 ))], where as M → ∞ , the partition 0 = t 0 < t 1 < · · · < t M = t 0 satisfies max 1 ≤ i ≤ M | t i − t i − 1 | → 0. The survivo r fun c- tion in te rms o f the cumulat ive hazard fun ction b e- comes S ( t ) = I { t < 0 } + I { t ≥ 0 } t Y w =0 [1 − Λ( dw )] . (2.1) F or a discrete random v ariable T with j ump p o ints { t j } , the h azard λ j at t j is the conditional p robabil- it y that T = t j , giv en T ≥ t j , so Λ( t ) = P { j : t j ≤ t } λ j . If T is an absolutely con tin uous random v ariable with densit y fun ction f ( t ), its hazard rate function is λ ( t ) = f ( t ) /S ( t ) , so Λ( t ) = R t 0 λ ( w ) dw = − log S ( t ). The p ro duct-in tegral r epresen tation of S ( t ) ac cord- ing to wh ether T is purely discrete or p urely con tin- uous is S ( t ) = t Y w =0 [1 − Λ( dw )] (2.2) = Y t j ≤ t [1 − λ j ] , if T is discrete, exp − Z t 0 λ ( w ) dw , if T is con tin uous. A b enefit of using hazards or h azard rate functions in mo deling is that they provide qu alitati ve asp e cts of the ev ent o ccurr ence pro cess as time progresses. F or instance, if the hazard rate fu n ction is increas- ing (decreasing) then this indicate s that the ev en t o ccurrences are in creasing (decreasing) as time in- creases, and thus we ha ve th e n otion of increasing (decreasing) failure rate [IFR (DFR)] distribu tions. F or man y y ears, it was the fo cus of theoretical re- liabilit y researc h to deal with cl asses of distribu - tions suc h as IFR, DFR, increasing (decreasing) fail- ure rate on a v erage [IFRA (DFRA)], and so on, MODELING AND ANAL YSIS OF EVENT TIMES 3 sp ecifically with regard to their closure prop erties under certain reliabilit y op erations (cf. Barlo w and Prosc han, 1981 ). In monito ring an exp e rimenta l unit for the o c- currence of a recurrent ev ent , it is con v enien t and adv an tag eous to utilize a coun ting p ro cess { N ( s ) , s ≥ 0 } , wh ere N ( s ) denotes the num b er of times that the ev ent has o ccurred ov er the interv al [0 , s ]. The paths of this sto c hastic pro cess are step-fu n ctions with N (0) = 0 and with ju mps of un it y . If w e rep- resen t the calendar times of ev en t o ccurr ences b y S 1 < S 2 < S 3 < · · · with the con v en tion that S 0 = 0, then N ( s ) = P ∞ j =1 I { S j ≤ s } . Th e interev ent times are denoted b y T j = S j − S j − 1 , j = 1 , 2 , . . . . In sp e ci- fying the sto c hastic c haracteristic s of the ev en t o ccurrence pro c ess, one either sp eci fies all the finite- dimensional distributions of the pro cess { N ( s ) } , or sp ecifies the join t d istributions of the S j ’s or the T j ’s. F or example, a common sp ecification for even t o ccurrences is the assumption of a homogeneous P ois- son pro cess (HPP) w here the in terev en t times T j are indep end en t and iden tically distributed exp o nentia l random v aria bles w ith scale β . This is equiv alen t to s p ecifying th at, for any s 1 < s 2 < · · · < s K , the random v ectors ( N ( s 1 ) , N ( s 2 ) − N ( s 1 ) , . . . , N ( s K ) − N ( s K − 1 )) hav e indep endent comp onent s with N ( s j ) − N ( s j − 1 ) ha ving a Poisson d istribution with param- eter β ( s j − s j − 1 ). F rom this sp ec ification, the finite- dimensional distributions of ( N ( s 1 ) , N ( s 2 ) , . . . , N ( s K )) ca n b e obtained. An imp ortan t concept in dynamic mo deling is that of a history or a fi ltration, a family of σ -fields F = {F s : s ≥ 0 } w here F s is a sub- σ -field of F with F s 1 ⊆ F s 2 for ev ery s 1 < s 2 and with F s = T h ↓ 0 F s + h , a righ t-con tin uit y prop erty . On e int erprets F s as all information that accrued o v er [0 , s ]. When augmen ted in (Ω , F , P ), we obtain the fi ltered pr obabilit y space (Ω , F , F , P ). It is with resp ec t to suc h a filtered probabilit y space that a pr o cess { X ( s ) : s ≥ 0 } is said to b e adapted [ X ( s ) is measurable with resp ect to F s , ∀ s ≥ 0]; is said to b e a (sub)martingale [adapted, E | X ( s ) | < ∞ , and , ∀ s, t ≥ 0, E { X ( s + t ) |F s } ( ≥ ) = X ( s ) almost surely]. Do ob–Mey er’s decomp osition guaran tees that f or a submartingale Y = { Y ( s ) : s ≥ 0 } there is a unique increasing pr ed ictable (measur- able with resp ect to the σ -field generated by adapted pro cesses with left-c ont inuous paths) pro cess A = { A ( s ) : s ≥ 0 } , called the comp ensator, with A (0) = 0 suc h that M = { M ( s ) = Y ( s ) − A ( s ) : s ≥ 0 } is a martingale. Via Jensen’s inequalit y , then for a square-in tegrable martingale X = { X ( s ) : s ≥ 0 } , there is a unique comp ensator pro cess A = { A ( s ) : s ≥ 0 } su c h that X 2 − A is a martingale. Th is pro cess A , denoted b y h X i = {h X i ( s ) : s ≥ 0 } , is calle d the pre- dictable quadratic v ariation (PQV) pro cess of X . A useful heuristic, though somewhat impr ecise, wa y of presen ting the main prop erti es of martingales and PQV’s is through the follo wing different ial forms. F or a martingale M , E { dM ( s ) |F s − } = 0 , ∀ s ≥ 0; whereas for the PQV h M i , E { d M 2 ( s ) |F s − } = V ar { dM ( s ) |F s − } = d h M i ( s ) , ∀ s ≥ 0 . F or the HPP N = { N ( s ) : s ≥ 0 } w ith rate β and with F = {F s = σ { N ( w ) , w ≤ s } : s ≥ 0 } , N is a sub- martingale since its paths are n ondecreasing. Its com- p ensator pro cess is A = { A ( s ) = β s : s ≥ 0 } , so that M = { M ( s ) = N ( s ) − β s : s ≥ 0 } is a martingale. F urth erm ore, since N ( s ) is P oisson-distributed with rate β s , so that { M 2 ( s ) − A ( s ) = ( N ( s ) − β s ) 2 − β s : s ≥ 0 } is a martingale, the PQV pro cess of M is also A . T hrough the heur istic forms , w e h av e E { d N ( s ) |F s − } = dA ( s ) , s ≥ 0. Since dN ( s ) ∈ { 0 , 1 } , then w e obtain the probabilistic expression P { dN ( s ) = 1 |F s − } = dA ( s ) , s ≥ 0. Analogously , V ar { dN ( s ) | F s − } = E { [ dN ( s ) − dA ( s )] 2 |F s − } = dA ( s ) , s ≥ 0. These formula s hold for a general counti ng pr o cess { N ( s ) : s ≥ 0 } with compens ator pro cess { A ( s ) : s ≥ 0 } . In essence, cond itionally on F s − , dN ( s ) has a Bernoulli distribution with success probabilit y dA ( s ). Ov er the interv al [0 , s ], follo wing Jacod , the lik e- liho o d fun ction can b e written in pro duct-int egral form as L ( s ) = s Y w =0 { dA ( w ) } dN ( w ) { 1 − dA ( w ) } 1 − dN ( w ) (2.3) = ( s Y w =0 [ dA ( w )] dN ( w ) ) exp {− A ( s ) } , with the last equalit y holding when A ( · ) h as con tin- uous paths. Sto c hastic inte grals play a cru cial role in this stochas- tic pro cess framew ork for ev en t time mod eling. F or a square-in tegrable martingale X = { X ( s ) : s ≥ 0 } with PQV pro c ess h X i = {h X i ( s ) : s ≥ 0 } , and for a b ounded predictable pr o cess Y = { Y ( s ) : s ≥ 0 } , the sto c hastic in tegral of Y wit h resp e ct to X , de- noted by R Y dX = { R s 0 Y ( w ) dX ( w ) : s ≥ 0 } , is wel l defined. It is also a square-in tegrable martingale with PQV pro cess h R Y dX i = { R s 0 Y 2 ( w ) d h X i ( w ) : s ≥ 0 } . When X is asso ciated with a coun ting pro cess N , that is, X = N − A , the paths of the sto chasti c in- tegral R Y dX can b e tak en as path wise L eb esgue– Stieltjes inte grals. 4 E. A. PE ˜ NA Martingale theory also pla ys a ma jor role in ob- taining asymp totic pr op erties of estimators as fir st demonstrated in Aalen ( 1978 ), Gill ( 1980 ) and An - dersen and Gill ( 1982 ). The main to ols used in asymp- totic analysis are Lenglart’s inequalit y (cf. Lenglart, 1977 ; Fleming and Harrington, 1991 ; And ersen et al., 1993 ) whic h is used in p ro ving consistency , and Reb olledo’s ( 1980 ) martingale central limit theorem (MCL T) (cf. Fleming and Harrington, 1991 ; Ander- sen et al., 1993 ) whic h is used f or obtaining weak con v ergence resu lts. W e refer the reader to Fl eming and Harrington ( 1991 ) and Andersen et al. ( 1993 ) for the in-depth theory and applications of these mo dern to ols in failure-time analysis. 3. CLASS OF D YNAMIC MODELS Let us n o w consider a unit b e ing monitored o v er time for th e o ccurrence of a recurrent ev en t. T he monitoring p erio d could b e a fi xed in terv al or it could b e a random in terv al, and for our purp oses w e denote this p erio d by [0 , τ ] , where τ is assumed to h av e some distribu tion G , which ma y b e degen- erate. With a slight notat ional c hange from Sec- tion 2 we denote by N † ( s ) the n um b er of ev en ts that h a v e o ccurr ed on or b efore time s , and b y Y † ( s ) an indicator pro cess wh ic h equals 1 w h en the unit is still under observ ation at time s , 0 otherwise. With S 0 = 0 and S j , j = 1 , 2 , . . . , denoting the su c- cessiv e calendar times of eve nt o ccurrences, and with T j = S j − S j − 1 , j = 1 , 2 , . . . , b e ing the in terev en t or gap times, observ e th at N † ( s ) = ∞ X j =1 I { S j ≤ m in( s, τ ) } and (3.4) Y † ( s ) = I { τ ≥ s } . Asso ciated with the unit is a, p ossibly time-dep en- den t, 1 × q co v ariate v ector X = { X ( s ) : s ≥ 0 } . In re- liabilit y engineering stud ies, the comp onen ts of this co v ariate vect or could b e related to environmen tal or op erat ing condition charact eristics; in biomedical studies, they could b e blo o d pr essure, treatmen t as- signed, initial tumor size, and so on; in a so ciologic al study of marital d isharmon y , they could b e length of marr iage, family income lev el, n um b e r of children residing with the couple, ages of children, and so on. Usually , after eac h ev ent o ccurrence, some form of in terv en tion is applied or p erformed, such as replac- ing or repairing failed comp onent s in a r eliabilit y system, or reducing or increasing physical activit y after a heart attac k in a medical setting. These in ter- v en tions will t ypically imp act the next o ccurr ence of the ev en t. Th ere is fur th ermore recognition that for the unit the inte reve nt times are asso ciated or cor- related, p ossibly b ecause of unobserved random ef- fects or so-ca lled frailties. A pictorial r epresen tation of these asp ec ts is giv en in Figure 1 . Ob serv e that b ecause of the finiteness of th e monitoring p erio d, whic h leads to a su m-quota acc ru al sc heme, there will alwa ys be a right- censored in terev en t time. The observ ed num b er of ev en t occur r ences o v er [0 , τ ], K = N † ( τ ), is also informativ e ab out the sto chas- tic mec hanism go v erning ev en t o ccurrences. In fact, since K = max { k : P k j =1 T j ≤ τ } , then, conditionally on ( K, τ ), the v ector ( T 1 , T 2 , . . . , T K ) has d ep endent comp onen ts, ev en if at the outset T 1 , T 2 , . . . are in- dep endent. Recognizing these different asp ects in recurrent ev en t settings, P e ˜ na and Hollander ( 2004 ) prop osed a general class of mo dels that sim ultaneously incor- p orates all of these asp ects. T o describ e this class of mo d els, w e sup p ose that there is a filtration F = {F s : s ≥ 0 } su ch that for eac h s ≥ 0, σ { ( N † ( v ) , Y † ( v +) , X ( v + ) , E ( v +)) : v ≤ s } ⊆ F s . W e also assume that there exists an unobserv able p ositiv e r and om v aria ble Z , called a frailt y , whic h induces the cor- relation among the in ter-ev en t times. The class of mo dels of Pe˜ na and Hollander ( 2004 ) can now b e describ ed in differen tial f orm via P { dN ( s ) = 1 |F s − , Z } = Z Y † ( s ) λ 0 [ E ( s )] (3.5) · ρ [ N † ( s − ); α ] ψ ( X ( s ) β ) ds, where λ 0 ( · ) is a baseline hazard rate fu n ction; ρ ( · ; · ) is a nonnegativ e function with ρ (0; · ) = 1 and with α b eing some parameter; ψ ( · ) is a nonnegativ e link function with β a q × 1 regression p arameter v ector; and Z is a frailt y v ariable. The at-risk pr o cess Y † ( s ) indicates that the conditional probabilit y of an ev ent o ccurring b ec omes zero wheneve r the unit is not un- der observ ati on. Possible c hoices of the ρ ( · ; · ) and ψ ( · ) fun ctions are ρ ( k ; α ) = α k and ψ ( w ) = exp( w ), resp ectiv ely . F or the geo metric c hoice of ρ ( · ; · ), if α > 1 the effect of accumula ting ev en t o ccurrences is to accelerate ev ent o ccurrences, w hereas if α < 1 the ev en t o c curren ces d ecelerat e, the latter situa- tion appropriate in soft w are debu gging. T h e p ro cess E ( · ) app earing as argum ent in the baseline hazard rate function, called the effectiv e age p ro cess, is pre- dictable, observ able, nonn egativ e and pathwise al- most surely d ifferentia ble with deriv ativ e E ′ ( · ). Th is MODELING AND ANAL YSIS OF EVENT TIMES 5 effectiv e age pro cess m o dels th e impact of p erformed in terv en tions after eac h ev en t o ccurrence. A picto- rial depiction of this effect ive age pro cess is in Fig- ure 2 . In th is plot, after the first ev ent , the p e r- formed in terv ent ion has the effect of rev erting the unit to an effectiv e age equal to the age ju st b e- fore the ev ent o ccurrence (called a minimal repair or interv en tion), while after the second eve nt, th e p erformed inte rven tion h as the effect of rev erting the effecti ve age to that of a new unit (hen ce this is ca lled a p erfect in terv en tion or repair). After the third even t, the in terv ent ion is neither m in imal n or Fig. 1. Pictorial depiction of the r e curr ent event data ac crual for a unit il l ustr ating the window of observat ion [0 , τ ] , inter- vention p erforme d after an event o c curr enc e, an unobserve d fr ailty Z , the pr esenc e of a ve ctor of c ovar iates X , the inter event times T j and the c alendar times of event o c curr enc es S j . Fig. 2. An example of an effe ctive age pr o c ess, E ( s ) , for a unit enc ountering suc c essive o c curr enc es of a r e curr ent event. 6 E. A. PE ˜ NA p erfect and it has the effect of restarting the effectiv e age at a v alue b et wee n zero and that ju st b e fore the ev en t occurred; while for the four th ev en t, the inter- v en tion is detrimenta l in that the restarting effectiv e age exceeds that just b efore the even t o c curred . The effect iv e age pro c ess could o ccur in man y forms, and the idea is this sh ould b e determined in a dynamic fashion in conjunction with interv en- tions that are p erformed. As suc h the determination of this pro cess should preferably b e through con- sultations with exp erts of the sub ject matter u nder consideration. Common forms of this effecti ve age pro cess are: Minimal Interv en tion or Repair: (3.6) E ( s ) = s, P erfect Interv en tion or Repair: (3.7) E ( s ) = s − S N † ( s − ) , BBS Mo del: (3.8) E ( s ) = s − S Γ η ( s − ) , where in ( 3.8 ) with I 1 , I 2 , . . . b eing indep enden t Bernoulli random v ariables with I k ha ving success probabilit y p ( S k ) with p : ℜ + → [0 , 1], w e defi n e η ( s ) = P N † ( s ) i =1 I i and Γ 0 = 0, Γ k = min { j > Γ k − 1 : I j = 1 } , k = 1 , 2 , . . . . Thus, in ( 3.8 ), E ( s ) represen ts the time measured from s since the last p erfect re- pair. T h is effectiv e age is from Blo ck, Borge s and Sa vits ( 1985 ), w hereas when p ( s ) = p for some p ∈ [0 , 1], w e obtain the effectiv e age pro cess for the Bro wn and Prosc han ( 1983 ) minimal repair mo del. Clearly , the effectiv e age functions ( 3.6 ) and ( 3.7 ) are sp ecial cases of ( 3.8 ). Other effect iv e age pro- cesses that could b e u tilized are those associated with the general repair mo del of Kijima ( 1989 ), Stadje and Zuc ke rman ( 1991 ), Baxter, Kijima and T ortorella ( 1996 ), Dorado, Hollander and Sethuraman ( 1997 ) and Last and Szekli ( 1998 ). See also Lindqvist ( 199 9 ) and Lindqvist, Elve bakk and Heggland ( 2003 ) for a review of some of th ese mo del s p ertaining to re- pairable systems, and Gonz´ alez, Pe˜ na and Slate ( 2005 ) for an effe ctiv e age pro cess suitable f or cancer stud- ies. A cru cial prop e rty arising fr om the inte nsity sp ec - ification in ( 3.5 ) is it amounts to p ostulating that, with A † ( s ; Z, λ 0 ( · ) , α, β ) = Z Z s 0 Y † ( w ) λ 0 [ E ( w )] (3.9) · ρ [ N † ( w − ); α ] ψ ( X ( w ) β ) dw, then, conditionally on Z , the p ro cess { M † ( s ; Z, λ 0 ( · ) , α, β ) (3.10) = N † ( s ) − A † ( s ; Z, λ 0 ( · ) , α, β ) : s ≥ 0 } is a square-in tegrable martingale with PQV p ro cess A † ( · ; Z, λ 0 ( · ) , α, β ). The class of mo dels is general and flexible and su bsumes man y curren t mo dels for recurrent ev en ts utilized in surviv al analysis and reli- abilit y . In p articular, it includ es those of Jelinski and Moranda ( 1972 ), Gail, San tner and Bro wn ( 198 0 ), Gill ( 1981 ), Pr entice , Williams and P eterson ( 1981 ), La wless ( 1987 ), Aalen and Hus eb y e ( 1991 ), W ang and Chang ( 1999 ), Pe˜ na, Strawderman and Hollan- der ( 2001 ) a nd Kv am and P e ˜ na ( 200 5 ). W e demon- strate the class of mo d els via some concrete exam- ples. Example 1. The fi rst exa mple concerns a load- sharing K -comp onent parallel system with ident i- cal comp o nents. The recurr en t ev ent of in terest is comp onen t f ailure and f ailed comp onen ts are not re- placed. When a comp o nent fails, a redistribution of the system load o ccurs among the remaining fun c- tioning comp onents, and to mo del this system in a general w a y , we let α 0 = 1 and α 1 , . . . , α K − 1 b e p ositiv e co nstants, referred to as load-share param- eters. One p ossible sp ecificatio n of these p arameters is α k = K / ( K − k ) , k = 0 , 1 , 2 , . . . , K − 1, though they could b e un k n o wn constan ts, p ossibly ord ered. The hazard rate of ev en t o ccurrence at cale ndar time s , pro vided that the system is still under observ ation, is λ ( s ) = λ 0 ( s )[ K − N † ( s − )] α N † ( s − ) , where λ 0 ( · ) is the common h azard rate function of eac h comp o- nen t and N † ( s ) is the n umb er of comp onent fail- ures observ ed on or b efore ti me s . This is a sp ecial case of the general class of mo dels with E ( s ) = s , ρ ( k ; α 1 , . . . , α K − 1 ) = [ K − k ] α k , and ψ ( w ) = 1 . This is the equal load-sharing mo d el in Kv am and P e ˜ na ( 2005 ). More generally , this could accommo date en- vironmen tal or op erating condition co v ariates for the system, and even an unobserv ed frailt y comp o- nen t. Example 2. Assume in a soft w are reliabilit y m o del that there are α bugs at the b eginning of a debug- ging pro cess and the ev en t of inte rest is encoun ter- ing a bug. A p ossible mo del is these α bugs are MODELING AND ANAL YSIS OF EVENT TIMES 7 comp eting to b e encoun tered, and if eac h of them has h azard rate of λ 0 ( s ) o f b eing encounte red at time s , then the total hazard rate at time s of the soft w are failing is λ 0 ( s ) α . Up on encoun tering a bug at time S 1 , this bug is eliminated, th us d ecreasing the num b er of remaining bu gs b y one. T he debu g- ging p ro cess is then restarted at time jus t after S 1 (assuming it tak es zero time to eliminat e the bug, clearly a n o v ersimplification). In general, supp ose that just b efore calendar time s , N † ( s − ) bugs ha v e b een remo v ed, and the la st bug w as encountered at calendar time S N † ( s − ) . Then, the o ve rall h azard of encount ering a b ug at calendar time s with s > S N † ( s − ) is λ 0 ( s − S N † ( s − ) )[ α − N † ( s − )]. T h us, pro- vided that the debugging pro cess is still in progress at time s , then the hazard of en countering a bug at time s is λ ( s ) = λ 0 ( s − S N † ( s − ) ) max[0 , α − N † ( s − )]. Again, this is a sp ecial case of the general class of mo dels with E ( s ) = s − S N † ( s − ) , a consequence of the r estart of the debu gging pro cess, ρ ( k ; α ) = max { 0 , α − k } and ψ ( w ) = 1. This soft ware debug- ging mo del is th e mo del of Jelinski and Moranda ( 1972 ) and it w as also p rop osed by Gail, San tner and Bro wn ( 1980 ) as a carcinogenesis mo del. See also Agustin and P e˜ n a ( 1999 ) for another m o del in soft w are d ebugging wh ic h is a sp ecial case of the general class of mo dels. Co x’s ( 1972 ) p r op ortional hazards mo del is one of the most used mo d els in biomedical and p u blic health settings. Extensions of this mo del ha v e b een used in recurrent ev en t settings, and Th ern eau and Gram bsc h ( 2000 ) discuss some of these Co x-based mo dels suc h as the indep enden t incremen ts mo del of Andersen and Gill ( 1 982 ), the conditional mo del of Prentic e, Willi ams and Pete rson ( 1981 ) and the marginal mod el of W ei, Lin and W eissfeld ( 1989 ). The indep endent incremen ts mo d el is a sp ecial case of the general class of mo d els obtained b y ta king ei- ther E ( s ) = s or E ( s ) = s − S N † ( s − ) with ρ ( k ; α ) = 1 and ψ ( w ) = exp( w ) . The marginal mod el strati- fies according to the ev en t num b er and assumes a Co x-t yp e mo del for eac h of these strata, with the j th int erev ent time in the i th unit h a ving in tensit y Y ij ( t ) λ 0 j ( t ) exp { X i ( t ) β j } , where Y ij ( t ) equals 1 un- til the o ccurr ence of the j th even t or wh en the unit is ce nsored. The conditional mo del is similar to the marginal mo del except that Y ij ( t ) b ecomes 1 only after the ( j − 1)st ev en t h as o ccurred. 4. ST A TIS TICAL INFERENCE The relev ant parameters for the mo del in ( 3.5 ) are λ 0 ( · ), α , β and the parameter associated with the distribution of the fr ailt y v ariable Z . A v ariet y of forms for this frailt y distribu tion is p ossible, but w e restrict to the case where Z has a gamma distribu- tion with mean 1 and v aria nce 1 /ξ . The parame- ter associated with G , the d istribution of τ , is usu- ally viewed as a n uisance, though in curren t join t researc h w ith Akim Adekp edjou, a Ph .D. student at th e Univ ersit y of South C arolina, the situation where G is informativ e ab out the d istributions of the int ereve nt time s is b eing explored. Kno wing the v alues of the mo del p arameters is im- p ortan t b ecause the m o del can b e utilized to p redict future occurr ences of the ev en t, an imp ortan t issue esp ecially if an ev ent o ccurrence is detrimen tal. T o gain kn o wledge ab out these parameters, a stu d y is p erformed to pro d uce sample data w hic h is the ba- sis of inference ab out the parameters. W e co nsid er a study wh ere n ind ep endent units are observed and with the observ ables o ve r (calendar) time [0 , s ∗ ] d e- noted by D A T A n ( s ∗ ) = { [( X i ( v ) , N † i ( v ) , Y † i ( v ) , E i ( v )) , v ≤ s ∗ ] , (4.11) i = 1 , 2 , . . . , n } . Observe th at D A T A n ( s ∗ ) provides information ab out the τ i ’s. More generally , w e observ e the fi l- trations { ( F iv , v ≤ s ∗ ) , i = 1 , 2 , . . . , n } or the ov erall filtration F s ∗ = {F v = W n i =1 F iv , v ≤ s ∗ } . The goals of statistical inf eren ce are to obtain p oin t or in ter- v al estimate s and/or test hypotheses ab out mo d el parameters, as we ll as to predict the ti me of occur- rence of a fu tu r e ev en t, wh en D A T A n ( s ∗ ) or F s ∗ is a v ai lable. W e fo cus on th e estimation problem b e- lo w, though w e note that the prediction problem is of great practica l imp ortance. Conditional on Z = ( Z 1 , Z 2 , . . . , Z n ), from ( 2.3 ) the lik eliho o d pro cess for ( λ 0 ( · ) , α, β ) is L C ( s ; Z , λ 0 ( · ) , α, β ) = n Y i =1 ( Z N † i ( s ) i ( s Y v =0 [ B i ( v ; λ 0 ( · ) , α, β ) ] dN † i ( v ) ) (4.12) · exp − Z i Z s 0 B i ( v ; λ 0 ( · ) , α, β ) dv ) , where B i ( v ; λ 0 ( · ) , α, β ) = Y † i ( v ) λ 0 [ E i ( v )] ρ [ N † i ( v − ); α ] ψ [ X i ( v ) β ]. Ob s erve that the like liho o d pro cess when 8 E. A. PE ˜ NA the mod el d o es not inv olv e an y frailties is obtai ned from ( 4.12 ) by setting Z i = 1 , i = 1 , 2 , . . . , n , wh ic h is equiv alent to letting ξ → ∞ . The resulting no-frailt y lik eliho o d pro cess is L ( s ; λ 0 ( · ) , α, β ) = n Y i =1 (( s Y v =0 [ B i ( v ; λ 0 ( · ) , α, β ) ] dN † i ( v ) ) (4.13) · exp − Z s 0 B i ( v ; λ 0 ( · ) , α, β ) dv ) . This lik elihoo d pro cess is the basis of inference ab out ( λ 0 ( · ) , α, β ) in th e absence of frailties. Going bac k to ( 4.12 ), by marginalizing ov er Z und er the gamma frailt y assumption, the lik eliho o d pro cess for ( λ 0 ( · ) , α, β , ξ ) b ecomes L ( s ; λ 0 ( · ) , α, β , ξ ) = n Y i =1 ( ξ ξ + R s 0 B i ( w ; λ 0 ( · ) , α, β ) dw ξ (4.14) · s Y v =0 ( N † i ( v − ) + ξ ) B i ( v ; λ 0 ( · ) , α, β ) · ξ + Z s 0 B i ( w ; λ 0 ( · ) , α, β ) dw − 1 dN † i ( v ) ) . There are t w o p ossib le sp ecifications f or the base- line hazard rate fu nction λ 0 ( · ): p arametric or non- parametric. If parametrically sp ecified, then it is p ostulated to b elong to some parametric family of hazard r ate functions, suc h as the W eibull or gamma family , that dep end s on an unkno wn p × 1 param- eter v ecto r θ . In this situation, a p ossible estima- tor of ( θ , α, β , ξ ), giv en F s ∗ , is the m aximum lik e- liho o d estimator ( ˆ θ , ˆ α, ˆ β , ˆ ξ ) , the maximize r of the mapping ( θ , α, β , ξ ) 7→ L ( s ∗ ; λ 0 ( · ; θ ) , α, β , ξ ) . Sto c ke r ( 2004 ) studied the finite- and large-sample p rop- erties, and asso ciated compu tational issues, of this parametric ML estimato r in his dissertation researc h. In particular, follo wing the approac h of Nielsen, Gill, Andersen and Sørensen ( 1992 ), he implemen ted an exp ectation–maxi mization (EM ) algorithm (c f. Dempster, Laird and Rubin , 1977 ) for obtaining the ML estimate. In this EM implement ation the frailt y v aria tes Z i are view ed as missing and a v arian t of the no-frailt y like liho o d pro cess in ( 4.13 ) is used for the maximizati on step in this algorithm. W e re- fer to Sto c k er ( 20 04 ) for details of this computa- tional implemen tation. F or large n , and under cer- tain regularit y conditions, it can also b e sho wn th at ( ˆ θ , ˆ α, ˆ β , ˆ ξ ) is approximat ely m ultiv ariat e normally distributed with mean ( θ , α, β , ξ ) and co v ariance ma- trix 1 n I − 1 ( ˆ θ , ˆ α, ˆ β , ˆ ξ ) , where I ( θ , α, β , ξ ) is the ob- serv ed Fisher information asso ciated with the lik e- liho o d function L ( s ∗ ; λ 0 ( · ; θ ) , α, β , ξ ) . That is, with Θ = ( θ , α, β , ξ ) t , I ( θ , α, β , ξ ) = −{ ∂ 2 /∂ Θ ∂ Θ t } · l ( s ∗ ; λ 0 ( · ; θ ) , α, β , ξ ) , where l ( s ; λ 0 ( · ; θ ) , α, β , ξ ) is the log-lik el iho o d pro cess give n by l ( s ; λ 0 ( · ; θ ) , α, β , ξ ) = n X i =1 ( ξ log ξ ξ + R s 0 B i ( w ; λ 0 ( · ; θ ) , α, β ) dw + Z s 0 log ( N † i ( v − ) + ξ ) (4.15) · B i ( v ; λ 0 ( · ; θ ) , α, β ) · ξ + Z s 0 B i ( w ; λ 0 ( · ; θ ) , α, β ) dw − 1 dN † i ( v ) ) . T ests of hyp otheses and construction of co nfi dence in terv als ab out mo d el parameters can b e dev elop ed using the asymptotic pr op erties of the ML estima- tors. F or small samples, they can b e based on thei r appro ximate sampling distributions obtained through computer-in tensiv e methods s u c h as b o otstrapping. It is usually th e case that a p arametric sp ecifica- tion of λ 0 ( · ) is more suitable in the reliabilit y and engineering situations. In biomedical and public health settings, it is typ- ical to sp ecify λ 0 ( · ) n onparametrically , that is, to simply assume that λ 0 ( · ) b elongs to the class of haz- ard rate fu nctions with s u pp ort [0 , ∞ ). This leads to a semiparametric mo del, with infinite-dimensional parameter λ 0 ( · ) and fin ite-dimensional parameters ( α, β , ξ ) . Inference for this semiparametric mo del w as considered in P e ˜ na, Slate and Gonz´ alez ( 2007 ). In this setting, in terest is fo cused on the finite-dimensional parameters ( α, β , ξ ) and the in fi nite-dimensional pa- rameter Λ 0 ( · ) = R · 0 λ 0 ( w ) dw and its surviv or func- tion S 0 ( · ) = Q · w =0 [1 − Λ 0 ( dw )]. A d ifficult y encoun- tered in estimati ng Λ 0 ( · ) is that in the int ensit y sp ecification in ( 3.5 ), the argum en t of λ 0 ( · ) is the ef- fectiv e age E ( s ), not s , and our in terest is in Λ 0 ( t ) , t ≥ 0. This p oses difficulties, esp ecially in establishing asymptotic pr op erties, b ecause the usual martin- gale approac h as pioneered by Aalen ( 1978 ), Gill ( 1980 ) and Andersen and Gill ( 1982 ) (see also An- dersen et al., 1993 and Fleming and Harr in gton, 1991 ) does not directly carry through. In the s im- ple i.i. d. renew al setting wh ere E ( s ) = s − S N † ( s − ) , ρ ( k ; α ) = 1 and ψ ( w ) = 1 , P e ˜ na, Strawderman and MODELING AND ANAL YSIS OF EVENT TIMES 9 Hollander ( 2000 , 2001 ), follo wing ideas of Gill ( 1981 ) and S ellk e ( 1988 ), imp lemented an ap p roac h using time transformations to obtain estimators of Λ 0 ( · ) and S 0 ( · ). In an indirect wa y , w ith partial use of Lenglart’s inequalit y and Reb olledo’s MCL T, they obtained asymp totic pr op erties of these estimators, suc h as their consistency and their weak con v er- gence to Gaussian pro cesses. This approac h in P e ˜ na, Stra wderman and Hollander ( 2001 ) wa s also utilized in P e ˜ na, Slate and Gonz´ alez ( 2007 ) to obtain the es- timators of the mo del p arameters in the more gen- eral mo del. The id ea b ehind this approac h is to defi ne the predictable (with resp ect to s f or fi xed t ) doub ly in- dexed pro cess C i ( s, t ) = I {E i ( s ) ≤ t } , i = 1 , 2 , . . . , n , whic h indicates whether at calendar time s the unit’s effectiv e age is at most t . W e then d efine the pr o- cesses N i ( s, t ) = R s 0 C i ( v , t ) N † i ( dv ), A i ( s, t ) = R s 0 C i ( v , t ) · A † i ( dv ), and M i ( s, t ) = N i ( s, t ) − A i ( s, t ) = R s 0 C i ( v , t ) M † i ( dv ). Because for eac h t ≥ 0, C i ( · ; t ) is a predictable and a { 0 , 1 } -v al ued pro cess, then M i ( · , t ) is a squ are-in tegrable martinga le with PQV A i ( · , t ). Ho w ev er, observe that for fixed s , M i ( s, · ) is not a martingale though it still satisfies E { M i ( s, t ) } = 0 f or eve ry t . Th e next step is to ha v e an alter- nativ e expression for A i ( s, t ) su c h that Λ 0 ( · ) ap- p ears with an argument of t instead of E i ( v ). With E ij − 1 ( v ) = E i ( v ) I { S ij − 1 < v ≤ S ij } on I { Y † i ( v ) > 0 } , this is ac hiev ed as follo ws: A i ( s, t ; Λ 0 ( · ) , α, β ) = Z s 0 Y † i ( v ) ρ [ N † i ( v − ); α ] · ψ ( X i ( v ) β ) I {E i ( v ) ≤ t } λ 0 [ E i ( v )] dv (4.16) = N † i ( s − ) X j =1 Z S ij S ij − 1 Y † i ( v ) ρ [ N † i ( v − ); α ] · ψ ( X i ( v ) β ) I {E ij − 1 ( v ) ≤ t } · λ 0 [ E ij − 1 ( v )] dv + Z s S iN † i ( s − ) Y † i ( v ) ρ [ N † i ( v − ); α ] · ψ ( X i ( v ) β ) I {E iN † i ( s − ) ( v ) ≤ t } · λ 0 [ E iN † i ( s − ) ( v )] dv . Letting ϕ ij − 1 ( v ; α, β ) = ρ [ N † i ( v − ); α ] ψ ( X i ( v ) β ) E ′ ij − 1 ( v ) I { S ij − 1 < v ≤ S ij } , and d efining the new “at-risk” pro cess Y i ( s, t ; α, β ) = N † i ( s − ) X j =1 I { t ∈ ( E ij − 1 ( S ij − 1 +) , E ij − 1 ( S ij )] } · ϕ ij − 1 [ E − 1 ij − 1 ( t ); α, β ] (4.17) + I { t ∈ ( E iN † i ( s − ) ( S iN † i ( s − ) +) , E iN † i ( s − ) ( s ∧ τ i )] } · ϕ iN † i ( s − ) [ E − 1 iN † i ( s − ) ( t ); α, β ] , then, after a v ariable transformation w = E ij − 1 ( v ) for eac h sum mand in ( 4.16 ), w e obtain an alterna- tiv e form of A i ( s, t ) giv en by A i ( s, t ; Λ 0 ( · ) , α, β ) = R t 0 Y i ( s, w ; α, β )Λ 0 ( dw ). The utilit y of this alterna- tiv e form is that Λ 0 ( · ) app ears with the correct ar- gumen t for estimating it. If, for the moment, w e as- sume that w e kno w α and β , b y virtue of the fact that M i ( s, t ; α, β ) h as zero mean, then using the idea of Aalen ( 1978 ), a method-of-moments “e stimator” of Λ 0 ( t ) is ˆ Λ 0 ( s ∗ , t ; α, β ) (4.18) = Z t 0 I { S 0 ( s ∗ , w ; α, β ) > 0 } S 0 ( s ∗ , w ; α, β ) n X i =1 N i ( s ∗ , dw ) , where S 0 ( s, t ) = P n i =1 Y i ( s, t ; α, β ). This “estimator” of Λ 0 ( · ) ca n b e plugged in to the like liho o d function o v er [0 , s ∗ ] to obtain the p r ofile lik eliho o d of ( α, β ), giv en b y L P ( s ∗ ; α, β ) = n Y i =1 N † i ( s ∗ ) Y j =1 [ ρ ( j − 1; α ) ψ [ X i ( S ij ) β ] (4.19) · ( S 0 ( s ∗ , E i ( S ij ); α, β ]) − 1 ] dN † i ( S ij ) . This p rofile lik eliho o d is reminiscen t of the partial lik eliho o d of Co x ( 1972 ) and Andersen and Gill ( 1982 ) for making in ference ab out the finite-dimensional parameters in the Cox prop ortional hazards mo del and the multi plicativ e in tensit y m o del. The estima- tor of ( α, β ) , denoted by ( ˆ α, ˆ β ), is the maximizer of the mappin g ( α, β ) 7→ L P ( s ∗ ; α, β ). Algorithms and 10 E. A. PE ˜ NA soft w are for compu ting the estimate ( ˆ α, ˆ β ) w ere de- v elop ed in Pe˜ na, Slate and Gonz´ alez ( 2007 ). The estimator of Λ 0 ( t ) is obtained by sub stituting ( ˆ α, ˆ β ) for ( α, β ) in ˆ Λ 0 ( s ∗ , t ; α, β ) to yield the generalize d Aalen–Breslo w –Nelson estimator ˆ Λ 0 ( s ∗ , t ) = Z t 0 I { S 0 ( s ∗ , w ; ˆ α, ˆ β ) > 0 } S 0 ( s ∗ , w ; ˆ α, ˆ β ) (4.20) · n X i =1 N i ( s ∗ , dw ) . By in v oking the pr o duct-in tegral repr esen tation of a survivor function, a generalized pro duct-limit es- timator of the baseline s urviv or function S 0 ( t ) is ˆ S 0 ( s ∗ , t ) = Q t w =0 [1 − ˆ Λ 0 ( s ∗ , dw )]. P e ˜ na, Slat e and Gonz´ alez ( 2007 ) also d iscussed the estimation of Λ 0 ( · ) and the fin ite-dimensional parameters ( α, β , ξ ) in the presence of gamma-dis- tributed frailties. The ML estimato rs of these pa- rameters maximize the like liho o d L ( s ∗ ; Λ 0 ( · ) , α, β , ξ ) in ( 4.14 ), with the pro viso that the maximizing Λ 0 ( · ) jumps only at observ ed v alues of the E i ( S ij )’s. An EM algorithm finds these maximizers and its imp le- men tation is describ ed in detail in Pe˜ na, Slate and Gonz´ alez ( 2007 ). W e briefly describ e the basic in- gredien ts of this algorithm here. With θ = (Λ 0 ( · ) , α, β , ξ ), in the exp ectation step of the algorithm, expr essions for E { Z i | θ , F s ∗ } and E { log Z i | θ , F s ∗ } , which are easy to obtain un d er gamma frailties, are needed. F or the maximization step, with E Z | θ (0) denoting exp ectation w ith resp ect to Z when the p arameter v ector θ equals θ (0) = (Λ (0) 0 ( · ) , α (0) , β (0) , ξ (0) ), w e require Q ( θ ; θ (0) , F s ∗ ) = E Z | θ (0) { log L C ( s ∗ ; Z , θ (0) } , w here L C ( s ; Z , θ ) is in ( 4.12 ). T his Q ( θ ; θ (0) , F s ∗ ) is maximized with re- sp ect to θ = (Λ 0 ( · ) , α, β , ξ ). This maximization can b e p erformed in t wo steps: first, maximize with re- sp ect to (Λ 0 ( · ) , α, β ) using the pr o cedure in the case without frailties except that S 0 ( s, t ; α, β ) is replaced b y S 0 ( s, t ; Z , α, β ) = P n i =1 Z i Y i ( s, t ; α, β ); and second, maximize w ith resp ect to ξ a gamma log-lik eliho o d with estimated log Z i and Z i . T o sta rt the iteration pro cess, a seed v alue for Λ 0 ( · ) is n eeded, whic h can b e the estimate of Λ 0 ( · ) with no frailties. Seed v al - ues for ( α, β , ξ ) are also required. Through this E M implemen tation, estimates of (Λ 0 ( · ) , α, β , ξ ) are ob- tained and , through the pro d uct-in tegral r epresen- tation, an estimate of the baseli ne survivor fu n ction S 0 ( · ). 5. ILLUSTRA TIVE EXAMPLES The applicabilit y of these d ynamic models still needs further and deep er in v estigation. W e provide in this section illustrativ e examples to d emonstrate their p oten tial app licabilit y . Example 3. The firs t example deals with a d ata set in Kumar and Klefsj¨ o ( 1992 ) whic h co nsists of failure times for h ydraulic systems of load-haul-dump (LHD) mac hines used in mining. T he data set has six mac hines with t w o mac hines eac h classified as old, medium and new. F or eac h mac hine th e suc- cessiv e failure times w ere observed and the result- ing data is d epicted in Fig ur e 3 . Using an effec- tiv e age pro cess E ( s ) = s − S N † ( s − ) , this w as ana- lyzed in Sto ck er ( 200 4 ) (see also Sto ck er and Pe˜ na, 2007 ) u s ing the general class of mo dels when the baseline hazard fun ction is p ostulated to b e a t wo - parameter W eibull hazard fun ction Λ 0 ( t ; θ 1 , θ 2 ) = ( t/θ 2 ) θ 1 , and in P e ˜ na, Slate and Gonz´ alez ( 2007 ) when the baseline hazard fun ction is nonparametri- cally sp ecified. Th e age co v aria te was co ded accord- ing to the dummy v ariables ( X 1 , X 2 ) taking v alues (0 , 0) for the oldest mac hines, (1 , 0) for the m edium- age mac hines and (0 , 1) for the n ewest mac hines. The parameter estimates obtained for a nonpara- metric and a paramet ric baseline hazard fun ction sp ecification are con tained in T able 1 , where the estimates for th e parametric sp ecification are from Sto c k er ( 2004 ). The estimates of the baseline sur- viv or fun ction S 0 ( · ) und er the nonp arametric and parametric W eibull sp ecifications are o v erlaid in Fig- ure 4 . F rom this table of estimates, observ e that a frailt y comp onen t is not needed for b oth nonpara- metric and parametric sp ecifications since the esti- mates of the frailt y parameter ξ are v ery large in b oth cases. Both estimates of th e β 1 and β 2 co effi- cien ts are negativ e, ind icating a p oten tial imp ro v e- men t in the lengths of the working p erio d of the mac hines when they are of medium age or new er, though an examination of the stand ard errors re- v eals that w e cannot conclude that the β -co efficien ts are significan tly d ifferen t from zero. On the other hand, the estimates of α for b oth sp ecifications are significan tly greater than 1, indicating the p oten- tial wea ke ning effects of accum ulating ev ent o ccur- rences. F rom Figure 4 w e also observe that the t w o- parameter W eibull app ears to b e a go o d p arametric mo del for the baseline hazard fun ction as the n on- parametric and parametric baseline hazard fun ction estimates are qu ite close to eac h other. Ho w eve r, a MODELING AND ANAL YSIS OF EVENT TIMES 11 T able 1 Par amete r es timates for the LHD hydr auli c data f or a nonp ar ametric and a p ar ametric (Weibul l ) sp e cific ation of the b aseline hazar d function Pa rameter With a n onparametric sp ecification With a parametric sp ecification, estimated of Λ 0 ( t ) Λ 0 ( t ) = ( t / θ 2 ) θ 1 α 1.03 1 . 03 (0 . 01) β 1 − 0.09 − 0 . 14 (0 . 20) β 2 − 0.05 − 0 . 08 (0 . 20) ξ 1 . 54 × 10 63 164198 (1307812 ) θ 1 NA 0 . 97 (0 . 075) θ 2 NA 0 . 006 (0 . 001 ) The va lues in paren theses in the third col umn are the approximate standard errors. formal p ro cedure for v alidating th is claim still needs to b e deve lop ed. Th is is a problem in go o dness-of-fit whic h is curren tly b eing pur sued. Example 4. The seco nd example is pr o vided b y fi tting the general class of m o dels to the blad- der cancer data in W ei, Lin and W eissfeld ( 1989 ). A pictorial depiction of this data set can b e foun d in P e ˜ na, Slate and Gonz´ alez ( 2007 ), where it w as analyzed usin g a n onp arametric sp ecification of the baseline hazard function. This data set consists of 85 su b jects and provides times to recurrence of blad- der cancer. The co v ariates included in the analysis are X 1 , the treatmen t indicator (1 = p laceb o, 2 = thiotepa); X 2 , the siz e (in cm) of the largest initial tumor; and X 3 , the num b er of initia l tumors. In fit- ting the general mo d el in ( 3.5 ) we u sed ρ ( k ; α ) = Fig. 3. Pictorial depiction of the LHD data set fr om Kumar and Klefsj¨ o ( 1992 ) which shows the suc c essive failur e o c curr enc es for e ach of the six machines. Machines 1 and 2 have ( X 1 , X 2 ) = (0 , 0) , machines 3 and 4 have ( X 1 , X 2 ) = (1 , 0) and machines 5 and 6 have ( X 1 , X 2 ) = (0 , 1) . 12 E. A. PE ˜ NA T able 2 Summary of estimates for the bladder data set fr om the Ande rsen–Gil l (A G), Wei, Lin and Weissfeld (WL W) and Pr entic e, Wil liams and Peterson (PWP) metho ds as r ep orte d in Therne au and Gr ambsch ( 2000 ), to gether with the estimates obtaine d fr om the gener al mo del using two effe ctive ages c orr esp onding to “ p erfe ct ” and “ minim al ” intervent ions Co v ariate Pa rameter A G WL W marginal PWP conditional General mo del Perfect Minimal log N ( t − ) α — — — 0.98 (0.07) 0.79 (0.13) frailt y ξ — — — ∞ 0.9 7 rx β 1 − 0.47 (0.20) − 0.58 (0.20) − 0.33 (0.21) − 0.32 (0.21) − 0.57 (0.36) size β 2 − 0.04 (0.07) − 0.05 (0.07) − 0.01 (0.07) − 0.02 (0.07) − 0.03 (0.10) num b er β 3 0.18 (0.05) 0.21 (0.05) 0.12 (0.05) 0.14 (0.05) 0.22 (0.10) α k . F u rthermore, sin ce the d ata set do es not con- tain in f ormation ab out the effectiv e age, we co n- sidered tw o situations f or demonstration purp oses: (i) p erfect interv en tion is alw a ys p erf ormed [ E i ( s ) = s − S iN † i ( s − ) ]; and (ii) min imal in terv ent ion is alwa ys p erformed [ E i ( s ) = s ]. The paramete r estimates ob- tained by fitting the mo d el with frailties , and other estimates using pr o cedures discussed in the litera- ture, are presen ted in T able 2 . The estimate s of their standard errors (s.e.) are in paren theses, with the s.e.’s under the minimal repair in terve nti on mo del obtained th r ough a jackknife pr o cedure. T he other parameter estimate s in the table are those from the marginal method of W ei, Lin and W eissfeld ( 1989 ), the conditional m etho d of Pr en tice, Williams and P eterson ( 1981 ) and the Andersen and Gill ( 1982 ) metho d, whic h were men tioned earlier (cf. Thern eau and Gram bsc h, 2000 ). Estimates of the survivor fun c- tions at the mean co v ariate v alues are in Figure 5 . Observe from this figur e that the thiotepa group p ossesses higher survivor probabilit y estimates com- pared to the placeb o group in either sp ecification of the effecti ve age p r o cess. Examining T able 2 , note the imp ortan t role the effectiv e ag e p r o cess p ro vides in reco nciling differences among the estimates from the other metho ds. When the effectiv e age pro cess corresp onds to p erfect inte rven tio n, the resulting es- timates from the general mo del are quite close to those obtained from the Pren tice, Williams and P e- terson ( 1981 ) conditional m etho d; wh ereas when a minimal in terv en tion effectiv e age is assumed, then the general mo del estimates are close to those from the marginal method of W ei, Lin and W eissfeld ( 1989 ). Th us, the differences among these existing method s Fig. 4. Estimates of the b ase line survivor function S 0 ( t ) under a nonp ar ametric and a p ar ametric (Weibul l ) sp e cific ation for the LHD hydr aulic data of Kumar and Klefsj¨ o ( 1992 ). MODELING AND ANAL YSIS OF EVENT TIMES 13 are p erhaps attributable to the t yp e of effectiv e age pro cess u sed. Th is indicates the imp ortance of the effectiv e age in mo deling r ecur r en t ev en t data. If p ossible, it th erefore b eho ov es one to monitor and assess this effect ive p ro cess in real applications. 6. OPEN PROBLEMS AND CONCLUDING REMARKS There are sev eral op en researc h issu es p ertaining to this general mo del for recurr en t ev ents. First is to ascertain asymptotic prop erties of the estimators of mo del parameters under the frailt y mo del when the baseline hazard rate fu n ction Λ 0 ( · ) is nonp aramet- rically sp ecified. A second pr ob lem, wh ic h arises af- ter fitting this general cla ss of mo dels, is to v alidate its appropriateness and to determine the p resence of outlying and/or influentia l observ atio ns. This is cur- ren tly b eing p erformed join tly with Jonathan Quiton, a Ph.D. student at the Univ ersit y of South Carolina. Of p articular issue is the imp act of the sum-quota accrual scheme, leading to the issue of determin- ing the prop er sampling distribution for assessing v al ues of test statistics. This v alidation issu e also leads to goo d ness-of-fit problems. It migh t, for in- stance, be of in terest to test the hyp othesis that the unkn own baseline hazard fu nction Λ 0 ( · ) b elongs to the W eibull class of hazard fun ctions. In cur- ren t researc h w e are exploring smooth go o dness-of- fit tests paralleling those in Pe˜ na ( 1998a , 1998 b ) and Agustin and Pe˜ na ( 200 5 ) whic h build on w ork b y Neyman ( 1937 ). T his will lead to notions of gener- alized residu als from this general class of mo dels. Another problem is a nonparametric Ba y esian ap- proac h to failure time mo deling. Not muc h has b een done for this app roac h in this area, though the com- prehensive pap er of Hjort ( 1990 ) pro vides a solid con tribution for the multiplic ativ e in tensit y m o del. It is certa inly of in terest to implemen t this Ba y esian paradigm for the general class of mo dels for recur- ren t even ts. T o conclude, this articl e p r o vides a select iv e re- view of rece nt resea rch dev elo pments in the m o del- ing and analysis of recurrent ev en ts. A general class of mod els acco unting for imp ortan t facets in recur- ren t even t mo deling was d escrib ed. Method s of in- ference for this class of mo dels w ere a lso describ ed, and illustrativ e examples w ere pr esented. Some op en researc h problems w ere al so men tioned. A CKNO WLEDGMENTS The author ac kno wledges the researc h supp ort pro- vided b y NIH Gran t 2 R01 GM56182 and NIH COBRE Gran t RR17698. He is very grateful to Dr. Sallie Keller-McNult y , Dr. Alyson Wilson and Dr. Chr is- tine Anderson-Co ok for inviting him to con tribute an article to this sp ecial issue of Statistic al Scienc e . He ac kno wledges his researc h collab orators, Dr. J. Gonz´ alez, Dr. M. Hollander, Dr. P . Kv am, Fig. 5. Estimates of the survivor f unctions evaluate d at the me an values of the c ovar iates. The solid curves ar e f or the p erfe ct intervention effe ctive age pr o c ess, wher e as the dashe d curves ar e for the minimal interve ntion effe ctive age pr o c ess . 14 E. A. PE ˜ NA Dr. E . Slate, Dr. R. Sto c k er and Dr. R. Stra wder- man, for their con tributions in join t researc h pap ers on w hic h some p ortions of this review article are based. He thanks Dr. M. Pe˜ na for the imp r o v ed art- w ork and Mr. Akim Adekp edjou and Mr. J. Qu iton for their care ful reading of the manuscript. REFERENCES Aalen, O. (1978). Nonparametric inference for a family of counting processes. A nn. Statist . 6 701–726 . MR049154 7 Aalen, O. and Husebye, E. (1991). Statistical analysis of rep eated events forming renew al pro cesses. Statist ics i n Me dicine 10 1227–1240. Agustin, M. A. and Pe ˜ na, E. A. (1999). A d ynamic com- p eting risks mo del. Pr ob ab. Engr g. Inform. Sci. 13 333–358. MR169512 4 Agustin, Z. and Pe ˜ na, E. (2005). A basis approach to goo dness-of-fit testing in recurrent even t models. J. Statist. Plann. Infer enc e 133 285–303. MR219447 9 Andersen, P., Borgan, Ø., Gill, R. and Keidi ng, N. (1993). Statistic al Mo dels Base d on Counting Pr o c esses . Springer, New Y ork. MR119888 4 Andersen, P. and Gi ll, R. (1982). Co x’s regression mo del for counting pro cesses: A large sample study . Ann. Statist. 10 1100–1 120 . MR067364 6 Barlo w, R. and Pro schan, F. (1981). Statistic al The ory of R eliabili ty and Life T esting : Pr ob ability M o dels . Holt, Rinehart and Winston, New Y ork. MR043862 5 Baxter, L., Kijima, M. and T or torella, M. (1996 ). A p oin t pro cess model for the reliabilit y of a maintained sys- tem sub ject to general repair. Comm. Statist. Sto chastic Mo dels 12 37–65. MR137487 0 Block, H., Borges, W. and Sa v i ts, T. (1985). Age- dep endent minimal repair. J. Appl. Pr ob ab. 22 370–385. MR078936 0 Bro wn, M. and Pro schan, F. (19 83). Imperfect repair. J. Appl. Pr ob ab. 20 851 –859. MR072047 6 Co x, D. (1972). Regression mo dels and life-tables (with discussion). J. R oy. Statist. So c. Ser. B 34 187 –220. MR034175 8 Dempster, A., Laird, N. and Rubin, D. (1977). Maximum lik eliho od estimation from incomplete data via t h e EM al- gorithm (with discussi on). J. R oy. Statist. So c. Ser. B 39 1–38. MR050153 7 Dorado, C., H ollander, M. and Sethuram an, J. (1997). Nonparametric estimation for a general repair mo del. Ann. Statist. 25 1140–116 0. MR144774 4 Fleming, T. and Ha rrington, D. (1991). Counting Pr o c esses and Survival Analysis . Wiley , New Y ork. MR110092 4 Gail, M., S antner, T. and Bro wn, C. ( 1980). An analysis of comparative carcinogenesis exp eriments based on m ulti- ple times to tumor. Biometrics 36 255–266. MR067232 5 Gill, R. (1980 ). Censoring and St o chastic Inte gr als . Mathe- matisc h Centrum, Amsterdam. MR059681 5 Gill, R. D. (1 981). T esting with replacement and the pro duct- limit estimator. A nn. Statist. 9 853–860 . MR061928 8 Gill, R. D. and Johansen, S. (1990). A surv ey of pro duct- integ ration with a view to ward application in surviv al anal- ysis. Ann. Statist. 18 1501–155 5. MR1074422 Gonz ´ alez, J., P e ˜ na, E. and Sla te, E. (2005). Mod - elling interv enti on effects after cancer relapses. Statistics in Me dici ne 24 3959–3 975. MR2221978 Hjor t, N. L. (1990). Nonparametric Bay es estimators based on b eta pro cesses in mod els for life history data. A nn. Statist. 18 1259–129 4. MR1062708 Hollander, M. and Pe ˜ na, E. A. (1995). Dynamic reliabil- it y mo dels with conditional prop ortional hazards. Lifetime Data Anal. 1 377–401. MR1371991 Jelinski, Z. and Moranda, P. (1972). Soft ware rel iability researc h. In Statistic al Computer Performanc e Eva luation (W. F reiberger, ed.) 465 –484. Academic Press, New Y ork. Kijima, M. (1989). Some results for repairable systems with general repair. J. Appl. Pr ob ab. 26 89–102 . MR0981254 Kumar, U. and Klefsj ¨ o, B. (1992). Reliabil ity analysis of hydraulic systems of LHD mac hines using the pow er la w process mo d el. R el iability Engine ering and System Safety 35 217–22 4 . Kv am, P. and Pe ˜ na, E. (2005). Estimating load-sharing prop erties in a dy namic reliabilit y system. J. Amer. Statist. Asso c. 100 262 –272 . MR2156836 Last, G. and Szekli, R. (1998). Asymptotic and monotonic- it y p roperties of some repairable sy stems. A dv. in Appl. Pr ob ab. 30 1089–1 110. MR167109 7 La wless, J. (198 7). Regression methods for Pois son pro cess data. J. A mer. Statist . Asso c. 82 808–815. MR090998 6 Lenglar t, E. (1977). R elation de domination entre deux pro- cessus. Ann. Inst. H. Poinc ar´ e Se ct. B ( N. S. ) 13 171–179 . MR047106 9 Lindqvist, B . (1999). Repairable systems with general re- pair. In Pr o c. T enth Eur op e an Conf er enc e on Safety and R eliability, ESREL ’ 99 (G. Sc hueller and P . Kafk a, eds.) 43–48. Balk ema, Rotterdam. Lindqvist, B. H., El vebakk, G. and Heggland, K. (2003). The trend-renewa l pro cess for statistical analysis of re- pairable sy stems. T e chnometrics 45 31–44. MR1956189 Neyman, J. (1937). “Smo oth” test for go od n ess of fit. Skand. Ak tuarietidskrift 20 149–199. Nielsen, G., Gill, R., Andersen, P. and Sørensen , T. (1992). A counting pro cess approac h to maximum lik eli- hoo d estimation in frailty mo dels. Sc and. J. Statist. 19 25– 43. MR117296 5 Pe ˜ na, E. A. (1998a). Smo oth go odn ess-of-fit t ests for com- p osite hypothesis in hazard b ased mo d els. Ann. Statist. 26 1935–1 971. MR16732 85 Pe ˜ na, E. A. (1998 b). Smo oth go od ness-of-fit tests for the baseline hazard in Co x’s proportional hazards mo del. J. Amer . Statist. Asso c. 93 67 3–692. MR1631 357 Pe ˜ na, E. and H ollander, M. (2004). Models for recurren t even ts in reliability and surviv al analysis. In Mathematic al R eliability : A n Exp ository Persp e ctive (R. So yer, T. Maz- zuchi and N . Singpu rw alla, eds.) 105–123. Kluw er, Boston. MR206500 1 Pe ˜ na, E. and Sla te, E. (2005). Dynamic modeling in reliabilit y and surviv al analysis. In Mo dern Statist ic al and Mathematic al Metho ds in R eliabili ty (A. Wilson, N. MODELING AND ANAL YSIS OF EVENT TIMES 15 Limnios, S. Keller-McNulty and Y. Armijo, eds.) 55–71. W orld Scientific, Singap ore. MR 223070 0 Pe ˜ na, E., Sla te, E. and Gonz ´ alez, J. (2007 ). Semipara- metric inference for a general class of mo dels for recurrent even ts. J. Statist. Plann. Inf er enc e . T o app ear. Pe ˜ na, E. A., S tra wderman, R. L. and Hollander, M. (2000). A weak conv ergence result relev ant in recurrent and renew al mo dels. In R e c ent A dvanc es in R eli ability The ory ( Bor de aux , 2000 ) ( N . Limnios and M. Nikulin, eds.) 49 3– 514. Birkh¨ auser, Boston. MR178350 1 Pe ˜ na, E. A., S tra wderman, R. L. and Hollander, M. (2001). Nonparametric estimation with recurrent event data. J. A mer. Statist . Asso c. 96 1299–1315. MR194657 8 Prentice, R., W illiams, B. and Peterson, A. (1981). On the regression analysis of m ultiv ariate failure time data. Biometrika 68 373–379. MR062639 6 Rebolledo, R. (1980). Cen tral limit theorems for lo- cal martingales. Z. Wahrsch. V erw. Gebiete 51 269–286. MR056632 1 Sellke, T . (1988). W eak con vergence of the Aalen estimator for a cen sored renewa l pro cess. I n Statistic al De cision The- ory and R elate d T opics IV ( S . Gupta and J. Berger, eds.) 2 183–194 . Springer, New Y ork. MR092713 2 Singpur w alla, N. D. (1995 ). Surviv al in dy n amic en viron- ments. Statist. Sci. 10 86– 103. St adje, W. and Zu ckerma n , D. (1991). Optimal mainte- nance strategies for repairable systems with general degree of repair. J. Appl. Pr ob ab. 28 384–396. MR110457 4 Stocker, R. (2004). A general class of parametric mo dels for recurren t ev ent data. Ph.D. d issertation, Univ. South Carolina. Stocker, R. and Pe ˜ na, E. (2007). A general class of para- metric mo d els for recurrent ev ent data. T e chnometrics . T o app ear. Therneau, T. and Grambsch, P. (2000). Mo deling Sur- vival Data : Extending the Cox M o del . Springer, New Y ork. MR177497 7 W ang, M.-C. and Chang, S.-H. (1999). Nonparametric es- timation of a recurrent surviv al function. J. Amer . Stat ist. Asso c. 94 146–153. MR168922 0 Wei, L., Lin, D. and We issfeld, L. (1989). Regression anal- ysis of multiv aria te incomplete fail ure time data by mod- eling marginal distributions. J. A mer. Statist. Asso c. 84 1065–1 073. MR11344 94

Original Paper

Loading high-quality paper...

Comments & Academic Discussion

Loading comments...

Leave a Comment